Since the 2008 financial crisis, financial transaction taxes (FTTs) have been debated as a potential instrument to address financial market instabilities and as a source for taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. revenue.

FTTs are levied on the trade in financial instruments such as stocks, bonds, or derivatives. Under an FTT, a percentage of the asset’s sales value is paid in taxes when it is traded. For example, if an investor sells an asset worth €1,000, they would be charged €1 on the transaction under a 0.1 percent FTT. Usually, FTTs apply only to select financial instruments and often have varying tax rates depending on the asset type.

2026 Data

2021

2020

Expand or Collapse Table

European Countries with a Financial Transaction Tax (FTT), as of June 2026

| Country | Tax Rate | Comment |

|---|---|---|

| Austria | - | |

| Belgium | 0.12% - 1.32% | Tax on stock exchange transactions (TOB): 0.12% on bonds and most ETFs, 0.35% on shares, 1.32% on Belgium-registered accumulating funds; per-transaction cap of €1,600 applies. |

| Bulgaria | - | |

| Croatia | - | |

| Cyprus | - | |

| Czech Republic | - | |

| Denmark | - | |

| Estonia | - | |

| Finland | 1.50% | Transfer tax on unlisted Finnish securities. Listed-company securities are generally exempt; rate effectively bites on unlisted shares and real-estate company shares. |

| France | 0.01% - 0.40% | FTT on equity of 0.4% for listed French companies with market cap > €1 bn; 0.01% high-frequency-trading levy on cancelled/modified orders. |

| Georgia | - | |

| Germany | - | |

| Greece | 0.10% | 0.1% sales tax on transfers of shares listed on Greek regulated markets/MTFs. |

| Hungary | 0.45% - 0.9% | Broader financial transactions tax on payment, securities and currency-exchange transactions: 0.45% standard, 0.9% on cash withdrawals, per-transaction cap of HUF 20,000 (ca. €57). |

| Iceland | - | |

| Ireland | 1% | Stamp duty on most transfers of Irish shares (above €1,000); 7.5% / 15% on certain real-estate-rich share transfers. Exemption for listed Irish SMEs with market cap < €1 bn. |

| Italy | 0.04% - 0.40% | Cash equities FTT applies to shares issued by Italian companies and securities tracking those shares; rates apply at 0.2% on regulated-market trades and 0.4% on over-the-counter trades. Tax base is the net daily balance of transactions on the same financial instruments by the same person on the settlement date. Derivatives FTT applies to derivatives tied to Italian shares on a separate schedule, reduced to 1/5 on regulated markets. Taxable base is the notional amount of the derivative. High-frequency trading FTT applies to transactions on any shares and share-based derivatives (wherever the shares are issued) in the Italian financial markets; trades amended or cancelled within half a second are subject to a 0.04% rate, to the extent they exceed 60% of overall trades. |

| Latvia | - | |

| Lithuania | - | |

| Luxembourg | - | |

| Malta | 2% | Stamp duty is charged on marketable securities in Maltese companies at a rate of 2%. A rate of 5% applies only in the case of transfers of shares in property companies, as a replacement of stamp duty on real estate. Exemptions include shares listed on the Malta Stock Exchange, non-resident-to-non-resident transfers, intra-group transfers, and companies determined by the Commissioner to have a majority of business interests outside Malta. |

| Netherlands | - | |

| Norway | - | |

| Poland | 0.5% - 2% | Tax on civil law transactions (PCC): 1% on transfer of shares not subject to VAT. PCC rates range 0.5% - 2% depending on transaction type. |

| Portugal | - | |

| Romania | - | |

| Slovakia | 0.4% - 0.8% | Financial transactions tax: 0.4% on gross debits from business bank accounts (max €40 per transaction), 0.8% on cash withdrawals. Payments for securities purchases made through a Slovak business account are caught at 0.4% on gross value. |

| Slovenia | - | |

| Spain | 0.20% | FTT on transfers of shares of listed Spanish companies with market cap > €1 bn. |

| Sweden | - | |

| Switzerland | 0.15% - 0.30% | Securities transfer tax (Umsatzabgabe): 0.15% on Swiss securities, 0.30% on foreign securities, where a Swiss securities dealer is involved. |

| Türkiye | 0% - 0.2% | Banking and Insurance Transactions Tax (BSMV) applies at 0.2% on the value of FX transactions (0% for specified FX transactions). |

| Ukraine | - | |

| United Kingdom | 0.5% - 1.5% | Stamp Duty Reserve Tax (SDRT) at 0.5% on transfers of shares in UK companies; 1.5% on transfers to depositary-receipt and clearance systems and on bearer-share transfers. Three-year relief for securities of newly listed UK companies. |

Data compiled by Alex Mengden

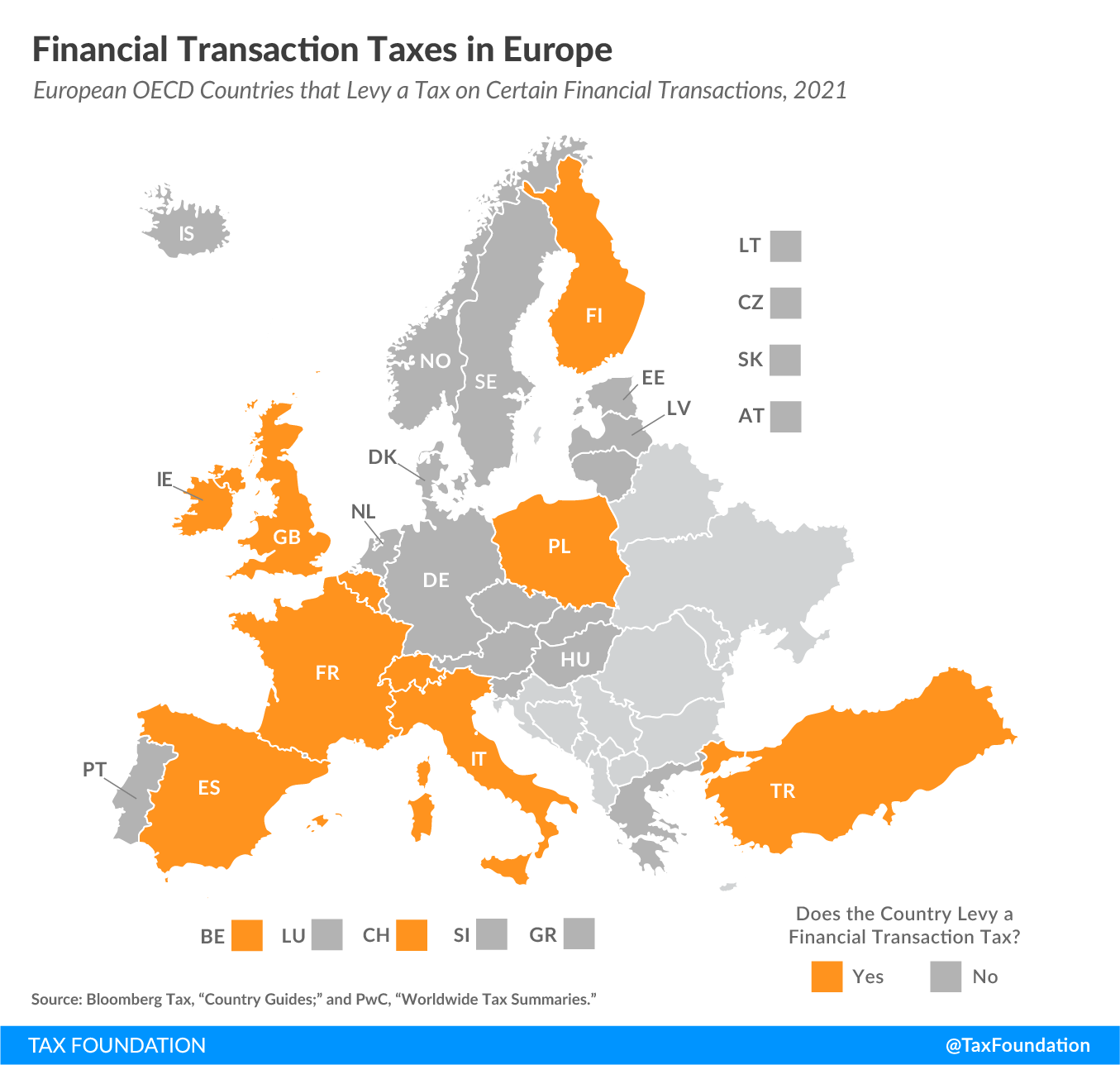

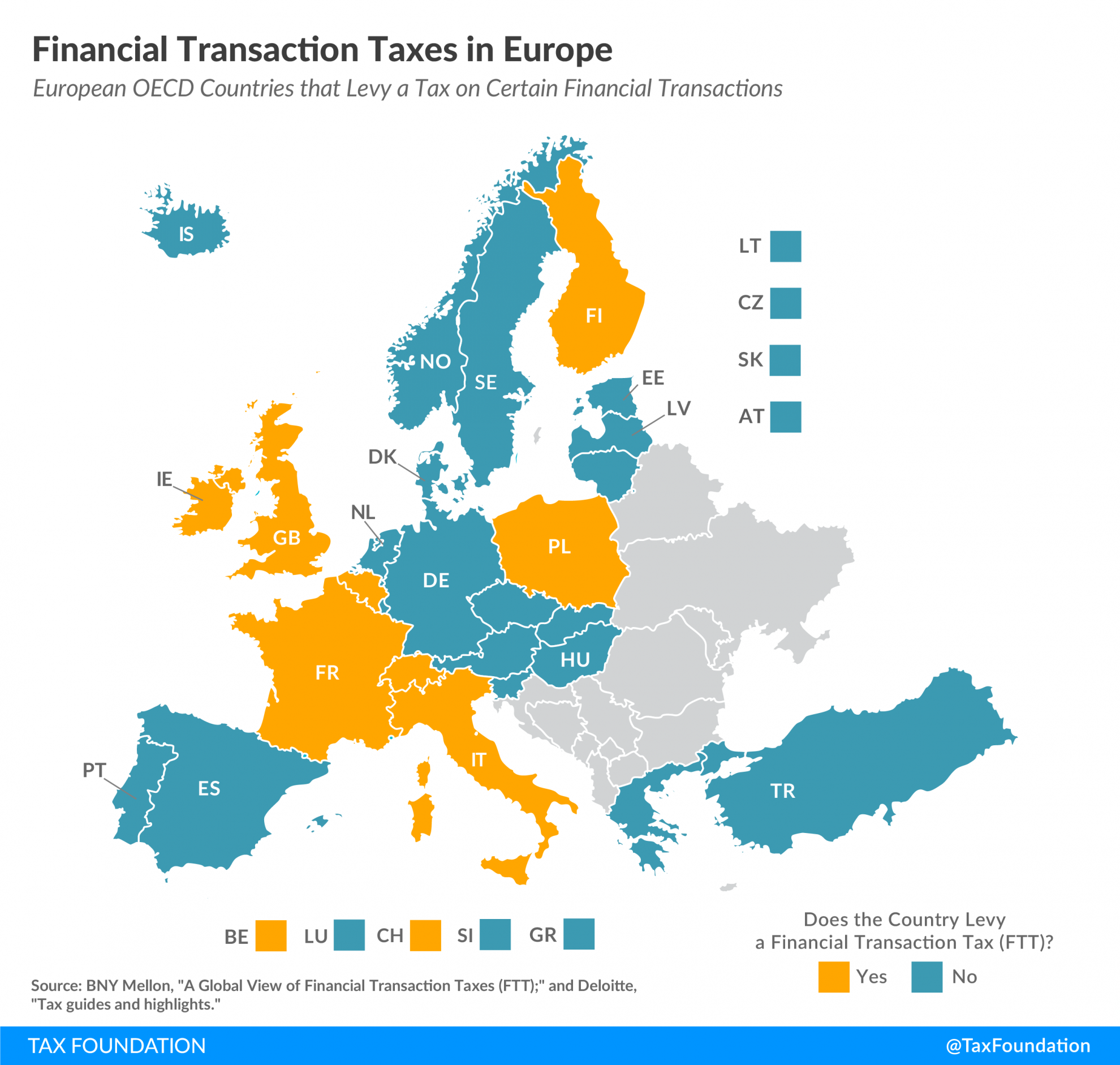

Fourteen countries in Europe—Belgium, Finland, France, Greece, Hungary, Ireland, Italy, Malta, Poland, the Slovak Republic, Spain, Switzerland, Turkey, and the United Kingdom—currently levy a type of financial transaction tax.

The FTTs vary significantly in the applicable rates as well as the scope of transactions covered across different European countries. For example, Switzerland levies a 0.15-0.30 percent stamp duty on the transfer of equities and bonds involving a Swiss securities dealer, while France implemented an FTT that taxes equity trades at 0.4 percent and high-frequency-trading at 0.01 percent.

FTTs directly increase the cost of raising equity capital to finance business investment. Due to the strong negative response of transaction volumes and share prices to higher transaction costs, they frequently fail to achieve their revenue goals.

Since 2011, the European Commission tabled proposals for an EU-wide FTT that would levy a 0.1 percent tax on the transfer of shares and bonds and a 0.01 percent tax on derivative contracts. However, negotiations came to a halt due to resistance from several EU member states, and in its work programme for 2026, the Commission indicated that it intends to withdraw the FTT proposal.

Recent Changes

Several European countries have made changes to their FTTs in the past years. France has raised its FTT rate from 0.3 to 0.4 percent in April 2025, and Italy doubled its cash-equity rates from January 2026. The Slovak Republic introduced a new transactions tax of 0.4 percent on gross debits from business bank accounts (max €40 per transaction) and 0.8 percent on cash withdrawals in 2025, from which sole traders are exempted since 2026.

In contrast, Finland reduced its FFT rates from a maximum of 2.0 percent to a uniform 1.5 percent in 2024. Ireland introduced an exemption for Irish-listed SMEs from its FTT in 2025. The United Kingdom started to apply a three-year relief to securities of newly listed companies in the London Stock Exchange from November 2025. Cyprus repealed its stamp duty from January 2026.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAbout the Author

Alex Mengden is an Economist at the Tax Foundation, where he focuses on international tax issues and tax policy in Europe. He holds a BA in philosophy and economics from the University of Bayreuth and an MSc in economics from the Ludwig Maximilian University of Munich.