UPDATED [3:48 pm]

Yesterday, the U.S. Supreme Court denied petitions to review decisions of the Fourth Circuit, Seventh Circuit, and Tenth Circuit courts of appeals which declared bans on same-sex marriage unconstitutional. The Court’s action will have an impact on the “tax lives” of same-sex couples in the states immediately impacted (Indiana, Oklahoma, Utah, Virginia, and Wisconsin) as well as the other states in the circuits in question for which these decisions are now binding law (North Carolina, South Carolina, West Virginia, Kansas, and Wyoming; Colorado has already begun to comply with the new Tenth Circuit precedent by issuing marriage licenses to same-sex couples).

First, a little background: three federal appeals courts ruled that same-sex marriage bans in Indiana, Oklahoma, Utah, Virginia, and Wisconsin are unconstitutional. These cases were then appealed to the U.S. Supreme Court. The Supreme Court decided not to hear the appeals, letting the decisions of the three lower courts stand.

The New York Times has a concise explanation of what this means:

The decision to let the appeals court rulings stand, which came without explanation in a series of brief orders, will have an enormous practical effect…. Most immediately, the Supreme Court’s move increased the number of states allowing same sex marriage to 24…up from 19. Within weeks, legal ripples from the decision could expand same-sex marriage to 30 states.

We published a report early this year outlining what state- and federal-level taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. filing looks like for same-sex couples (a follow up to this 2013 article on the “State of Celebration” guidance issued by the IRS). We wrote,

Gay and lesbian couples holding a valid marriage certificate from a state that recognizes same-sex marriage will be able to file a joint federal return…. Just under half the states…[at the time the report was written] do not recognize same-sex marriage while requiring taxpayers to reference their federal return when filing state income tax.

We pointed out that “[r]evenue officials in these states must therefore provide guidance for taxpayers,” and all 22 states had done so as of yesterday.

States that allow same-sex marriage have no problem, because same-sex couples residing within their borders can file a married tax return at both the state and the federal level—there is no conflict between the two levels. But in most of the states that don’t allow same-sex marriage, couples would be required to file single returns at the state level while filing married returns at the federal level. The real issue arises when states require taxpayers to reference their federal returns when filing out their state return, creating a situation where they are both single and married filers, depending on the level of government.

This matters for two reasons. First, the extra confusion and compliance costs are something that heterosexual couples don’t have to deal with. Second, the issue of a “marriage penaltyA marriage penalty is when a household’s overall tax bill increases due to a couple marrying and filing taxes jointly. A marriage penalty typically occurs when two individuals with similar incomes marry; this is true for both high- and low-income couples.” or “marriage bonusA marriage bonus is when a household’s overall tax bill decreases due to a couple marrying and filing taxes jointly. Marriage bonuses typically occur when two individuals with disparate incomes marry. Marriage penalties are also possible.” can cause tax liabilities to change drastically depending on whether or not a couple files as two single people versus as a married couple (more on that here, along with a nifty chart).

The five states immediately impacted by yesterday’s Supreme Court action treated same-sex couples in the following ways for tax filing purposes:

- Wisconsin requires same-sex couples to allocate income to two single returns using a state-provided schedule. They must also file a federal return, so this means that Wisconsin same-sex married couples have to fill out four separate forms during income tax filing season.

- Indiana, Virginia, and Oklahoma require same-sex taxpayers to complete two pro forma federal single tax returns and use that information to fill out two single state tax returns. The two “dummy” federal returns are not filed but used only for calculating state tax liability. When we include the federal return, this amounts to five forms total.

- Utah allowed joint filing by same-sex couples prior to the Supreme Court’s action, so it has the simplest and most favorable tax-filing scenario of the five states. [Update: Virginia announced that same-sex couples filing jointly at the federal level would also be able to file jointly at the state level, just as couples in Utah can do. The Indiana Department of Revenue also said this would be the case in Indiana.]

The court decisions require these states to fully recognize same-sex marriage, which means they must treat these couples exactly the same as opposite-sex couples in all aspects of state operations, which includes the realm of taxation. In light of this new legal landscape, revenue officials in these states must issue prompt revenue guidance for the taxpayers of their respective states.

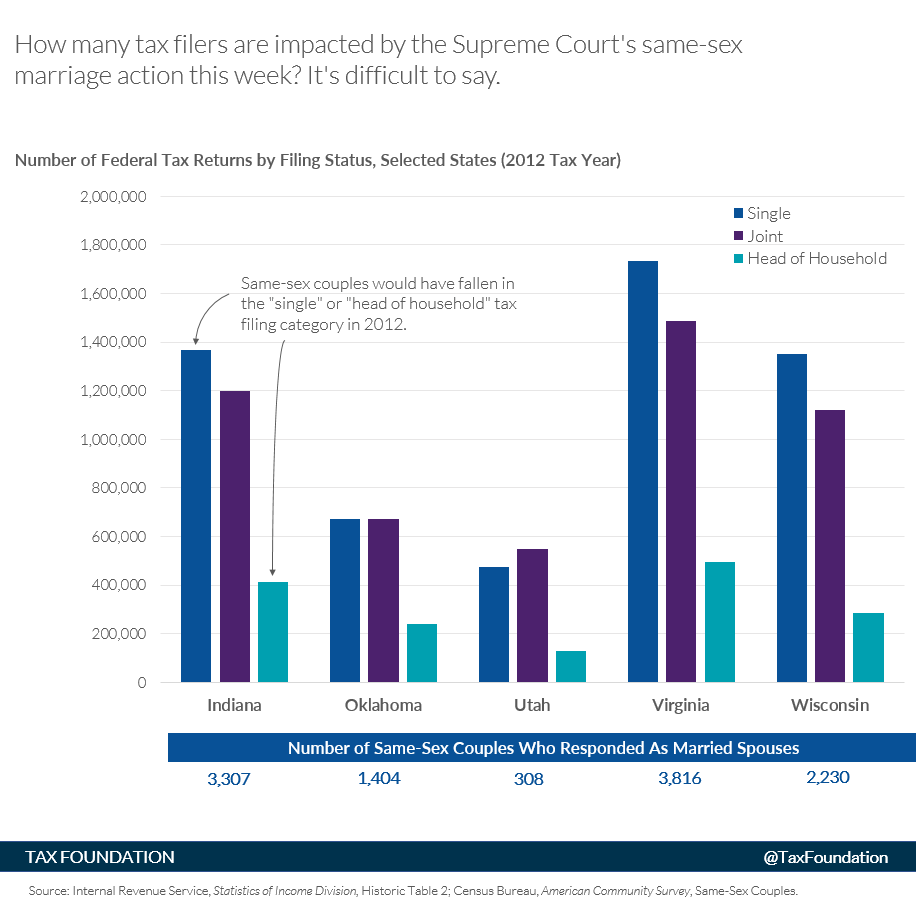

How many households does this impact? Well, it’s very hard to say because of serious data limitations. Though it’s not a perfect proxy, the number of filers at the federal level (and the federal filer status breakdown) is a reasonable approximation of the state tax picture—or it at least gives us a ballpark idea.

The table below shows the number of federal tax returns by filing status in the five states impacted by this week’s Supreme Court action (source data from the IRS here). That is, it shows how many single, joint, and head of household individual income tax returns were filed at the federal level in the 2012 tax year. It’s reasonable to assume that no same-sex couples would fall in the “joint” category (the purple bars below), since same-sex marriage was not recognized at the federal level at this time. That means they’d be captured in the single or head of household bars (blue and teal, respectively).

Click to enlarge.

Let’s pretend that this is a snapshot of filers at the state level in each of these five states, since we’re using federal tax return data as a proxy for state tax return data. The Census Bureau estimates the total number of same-sex households by state, and also the share of all same-sex households that respond as married “spouses.” That’s listed in blue underneath each state name.

For example, in 2012, Indiana had 3,307 same-sex couples that would have likely been married at the state level if it were legally permitted. Those couples were required to file as either two single individuals or as a head of household, because they were legally prohibited from filing jointly.

After the Supreme Court action this week, this means that a little sliver of the blue and teal bars in our chart above will likely move over to the “joint” category. It’s impossible to know the exact magnitude in each case, since we don’t know the filing category of the same-sex couples or if those couples will choose to file as “married filing separately.” The upward bound is somewhere close to the blue numbers on the bottom of the chart. But regardless of how many it impacts, the tax simplification for several thousand people is a step in the right direction.

As of press time, calls and emails to the revenue departments and the attorneys general of Indiana, Oklahoma, Virginia, and Wisconsin about when taxpayers can expect clear guidance have resulted in answers along the lines of both “we don’t know yet, but we’re working on it” and “we don’t know yet, and we’re waiting from guidance from higher up before acting”, or no response at all (Oklahoma and Indiana). As new information arises, we’ll keep you posted.

Update [3:24 pm]: The Virginia Department of Taxation has published a Tax Bulletin noting that “Same-sex marriages that are recognized for federal income tax purposes will now be recognized for Virginia income tax purposes.”

Update [3:48 pm]: According to the Indiana Department of Revenue, legally married same-sex couples can file joint Indiana state returns.

Follow Donnie and Liz on Twitter, @DonnieSaysStuff and @elizabeth_malm.

Share this article