Because taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. systems in countries differ, tax treaties can help minimize distortions and obstacles affecting cross-border investment. The United States should focus on expanding its treaty network to minimize friction for U.S. companies earning profits abroad and maintaining attractiveness for foreign companies investing in the U.S.

In the absence of a tax treaty, double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. can occur, limiting returns to shareholders or profits that companies can invest either in the U.S. or abroad.

According to the 2022 version of the International Tax Competitiveness Index, the average size of a tax treaty network is 74 countries, and the U.S. ranks 25th (out of 38 OECD countries) with 66 treaties.

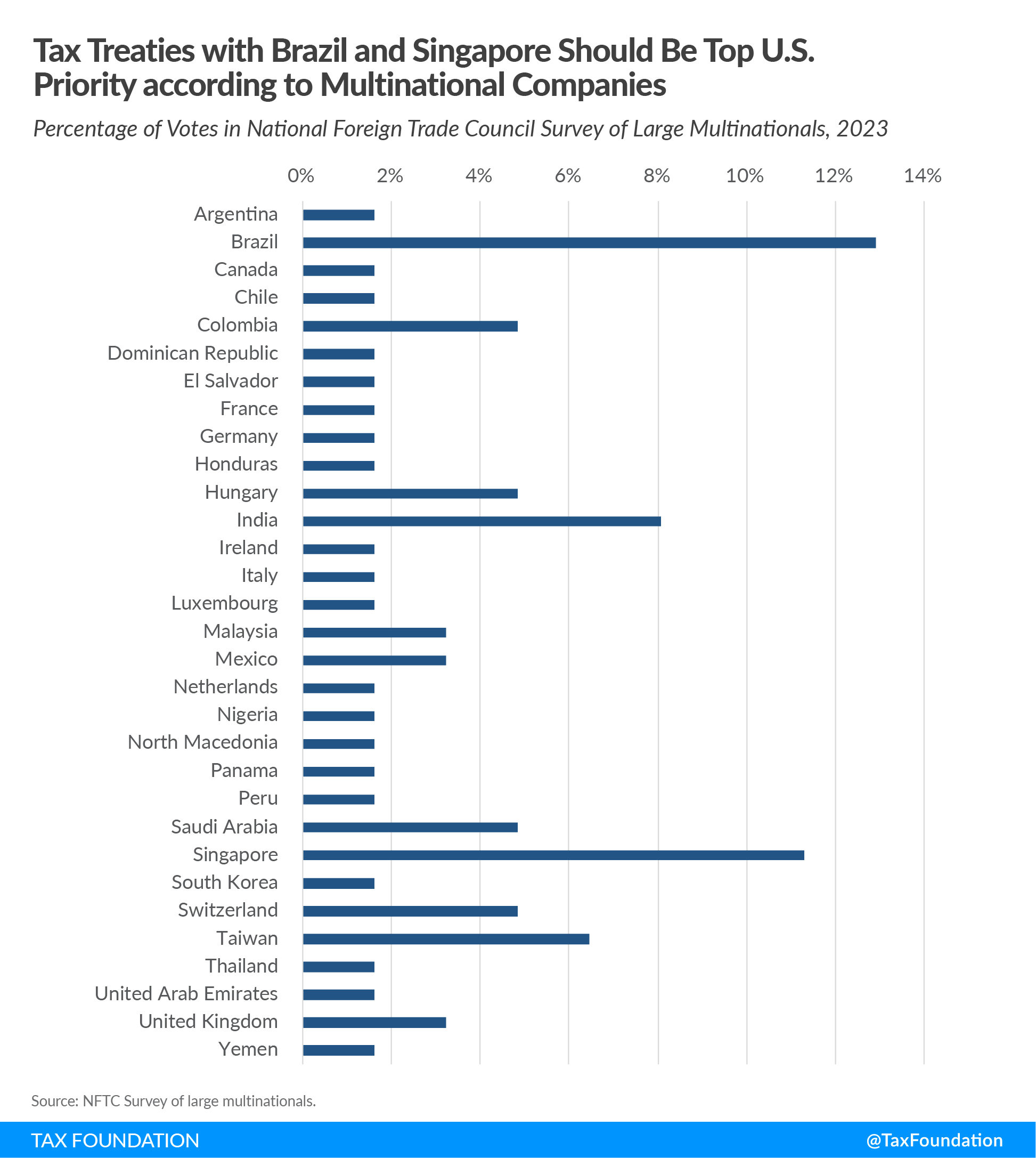

A recent National Foreign Trade Council survey of large multinational companies reveals that Brazil, Singapore, and India are the top priorities for cross-border tax treaties. While the U.S. does have a tax treaty with India, it does not have one with Brazil or Singapore.

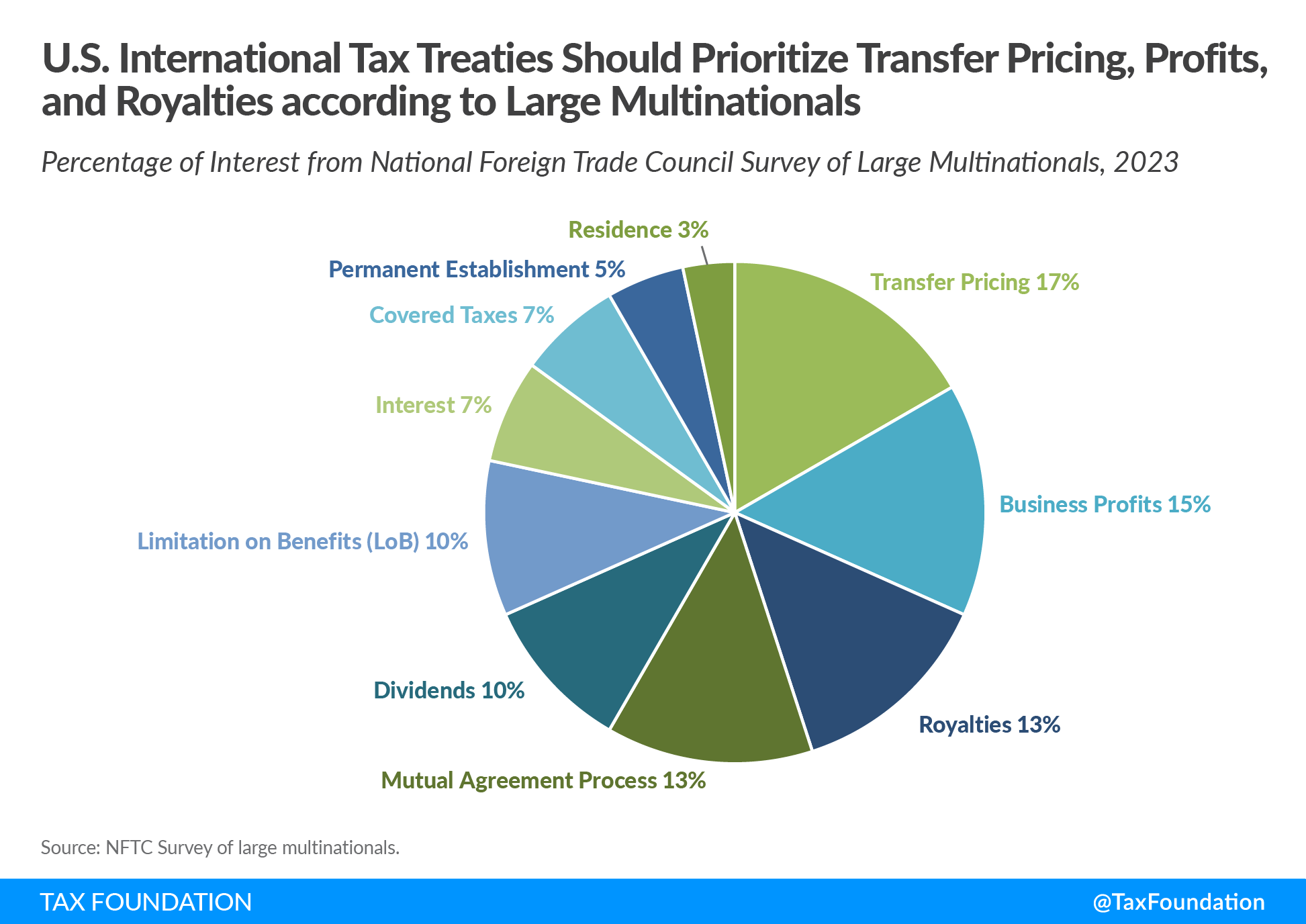

Respondents also consider transfer pricing and business profits to be the top negotiation priorities for these countries.

Eliminating double taxation and other distortions can facilitate business activity and contribute to more efficient tax regimes. One example is the recent transfer pricing developments in Brazil, which is in the process of aligning its rules with OECD standards.

In December 2022, the Brazilian Government published measures introducing new transfer pricing rules, the result of a joint OECD-Brazil project launched in 2018 to align Brazil’s transfer pricing rules to the global transfer pricing standard set out in the OECD Transfer Pricing Framework. They were approved by the Brazilian House of Representatives on March 30, 2023, and will be considered by the Brazilian Federal Senate at the beginning of June 2023. The inclusion of the arm’s length principle (i.e., related companies should transact with each other as if they were unrelated) in Brazilian transfer pricing rules is a stepping stone for Brazil to become a member of the OECD.

Even without a tax treaty between the U.S. and Brazil, a common approach to calculating profits in cross-border transactions will reduce businesses’ challenges when determining the tax impact of profitable projects in Brazil. But pursuing tax treaty negotiations with Brazil would further facilitate business operations in both countries.

The absence of a tax treaty can increase complexity and distortions, such as double taxation. In this regard, the U.S. is on the right track with Chile, but much work remains to be done to ensure coherent and pro-growth tax regimes across the globe.

The U.S. is in the process of ratifying a tax treaty with Chile that could greatly benefit both economies. Its provisions would eliminate double taxation and facilitate the day-to-day activities and transactions of businesses in Chile and in the United States, which have been affected by the lack of a bilateral treaty. U.S. foreign direct investment (FDI) into Chile, for instance, has fallen from $25.6 billion in 2018 to $22.6 billion in 2021. Additionally, the continued absence of a tax treaty between the two countries increases taxes on U.S. companies with Chilean operations by as much as 44 percent. On June 1, 2023, the U.S. Senate Foreign Relations Committee approved the treaty, recognizing the treaty’s role in strengthening U.S. competitiveness and growing FDI in Chile. Ratification by two-thirds of the Senate is necessary to ensure that the U.S. doesn’t miss out on opportunities for economic growth and prosperity.

The National Foreign Trade Council’s survey shows that the private sector recognizes the economic value of treaties as an instrument to increase tax certainty and decrease distortions. With potential forthcoming changes in Brazil and the tax treaty with Chile on the agenda, policymakers should seize the opportunity to maximize growth and simplify cross-border investment for economic actors. Removing barriers to cross-border investment is crucial, especially as the long-term stability of tax rules is being undermined by many international changes, including the implementation of the global minimum tax.

Share this article