Because taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. systems in countries differ, tax treaties can help minimize distortions and obstacles affecting cross-border investment. The United States should focus on expanding its treaty network to minimize friction for US companies earning profits abroad and maintaining attractiveness for foreign companies investing in the US.

In the absence of a tax treaty, double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. can occur, limiting returns to shareholders or profits that companies can invest either in the US or abroad.

According to the 2024 version of our International Tax Competitiveness Index, the average size of a tax treaty network is 75 countries, and the US ranks 25th (out of 38 OECD countries) with 66 treaties.

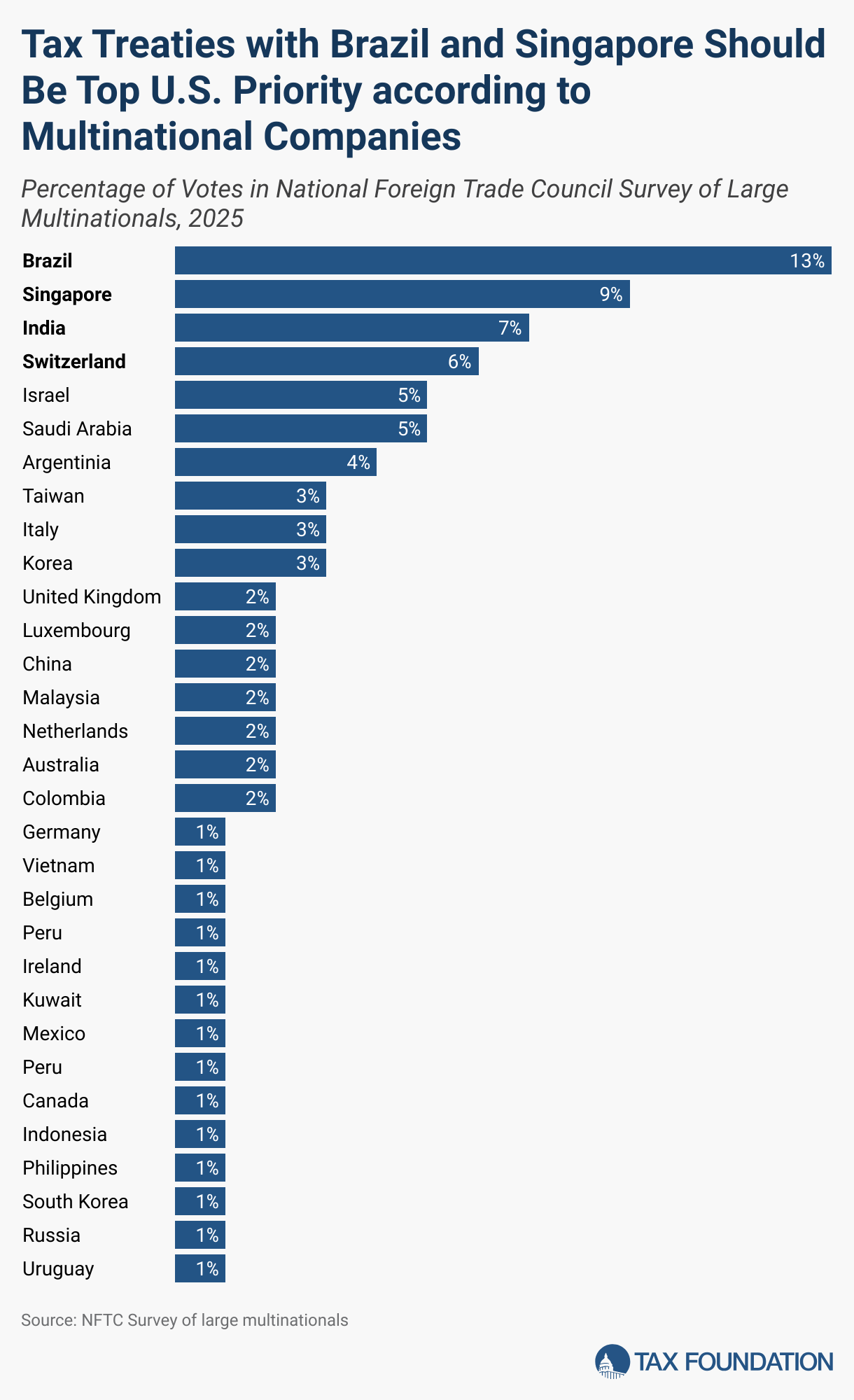

A recent National Foreign Trade Council survey of large multinational companies reveals that Brazil and Singapore are the top priorities for cross-border tax treaties. The US doesn’t have a tax treaty with either. At the same time, the 2025 survey shows that Switzerland and India have gained notable importance among treaty priorities. Unlike Brazil and Singapore, the US already maintains treaties with Switzerland and India, but these are increasingly seen as in need of modernization.

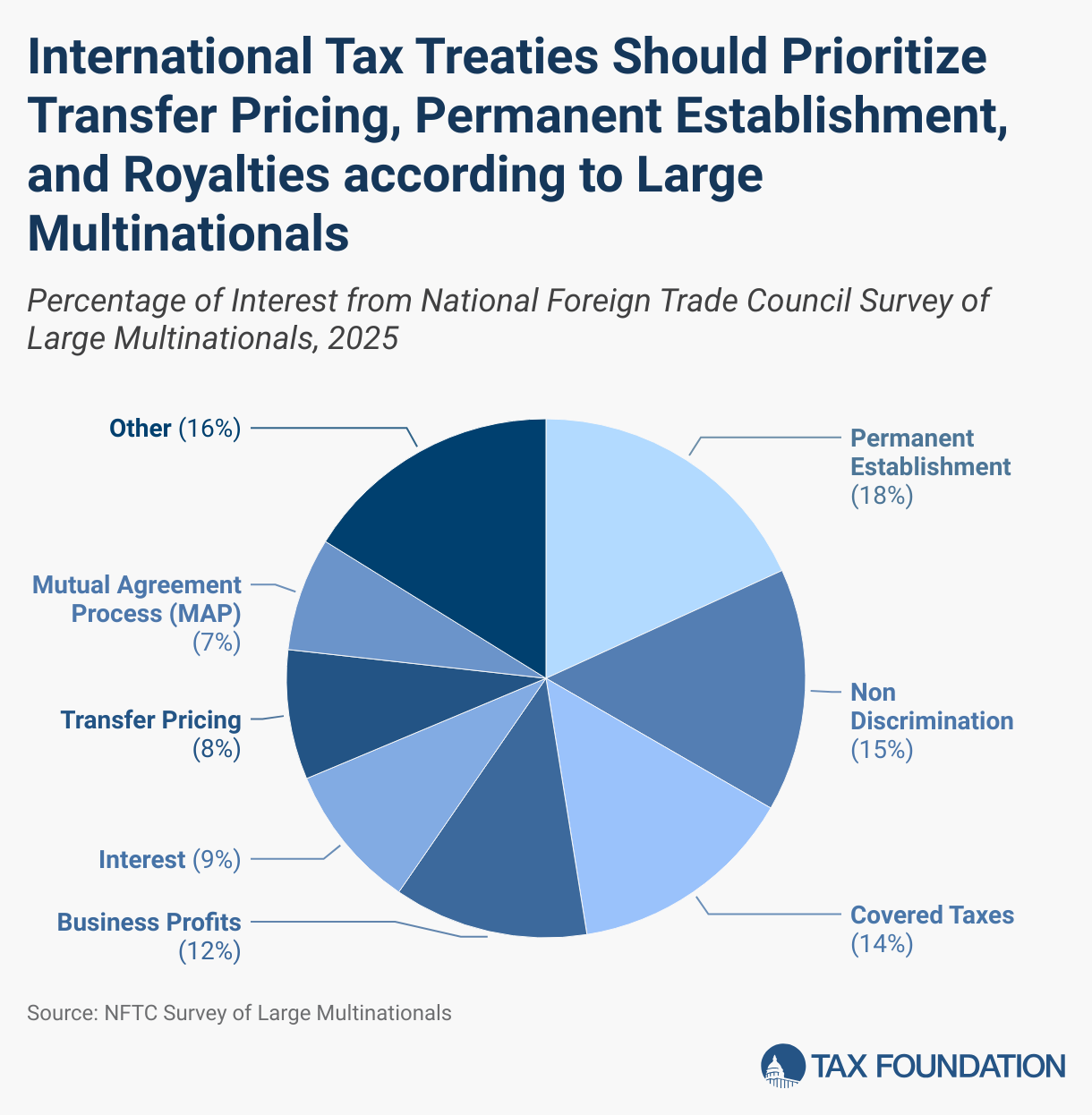

Respondents also identified reducing withholdingWithholding is the income an employer takes out of an employee’s paycheck and remits to the federal, state, and/or local government. It is calculated based on the amount of income earned, the taxpayer’s filing status, the number of allowances claimed, and any additional amount the employee requests. tax rates on royalties, improving transfer pricing provisions, and strengthening mutual agreement procedures as top negotiation objectives.

Eliminating double taxation and other distortions can facilitate business activity and contribute to more efficient tax regimes. While the United States has concluded double taxation agreements (DTAs) with countries such as Switzerland and India, no such agreements exist with Brazil or Singapore. This absence of DTAs can lead to tax uncertainty and the risk of double taxation, which may discourage cross-border investment and complicate tax compliance for multinational enterprises.

An important development in this context was Brazil’s recent reform of its transfer pricing rules, aligning them with OECD standards and thus moving closer to international best practices. Enacted in June 2023 and effective as of January 1, 2024, the reform introduced the arm’s length principle into Brazilian law. Even without a tax treaty between the US and Brazil, a common approach to calculating profits in cross-border transactions will reduce businesses’ challenges when determining the tax impact of profitable projects in Brazil. Nevertheless, a treaty would offer additional clarity and legal certainty to facilitate business operations in both countries. The absence of a tax treaty can increase complexity and distortions, such as double taxation.

In 2023, the US-Chile comprehensive income tax treaty successfully went into effect. This treaty reduces tax-related barriers to cross-border investments and ensures a more coherent and pro-growth international tax environment. It eliminates double taxation and facilitates the daily operations of companies in both countries. Importantly, it remains the only new US tax treaty to have gone into effect in recent years, and no others have been concluded since.

The National Foreign Trade Council’s survey shows that the private sector recognizes the economic value of treaties as an instrument to increase tax certainty and decrease distortions.

Brazil and Singapore remain top priorities for U.S. treaty negotiations. For both countries, reducing withholding tax rates on royalties emerged as a critical concern—emphasizing the need to eliminate barriers to cross-border innovation and intellectual property-related transactions. The United States should prioritize expanding its treaty network, especially with partners like Singapore and Brazil, to facilitate global investment flows. Removing barriers to cross-border investment is crucial, especially as international changes like the implementation of the global minimum tax and tensions over cross-border taxation undermine the long-term stability of tax rules.

While Brazil and Singapore top the list of priorities, the increased attention to Switzerland and India highlights the need to modernize existing agreements. The US–Switzerland tax treaty has already seen meaningful steps toward reform. Following the inception of a 2009 protocol in 2019, which introduced mandatory arbitration and enhanced information exchange, both governments have moved to modernize the treaty further. In late 2022, a US Treasury official publicly confirmed that negotiations were underway to comprehensively revise the 1996 agreement. The negotiations aim to reduce withholding taxes on intercompany dividends, update the Limitation on Benefits (LOB) clause, and improve treaty access for pension funds and multinational businesses.

In contrast, the US–India tax treaty, in force since 1991, has not been revised and is widely regarded as outdated. It features relatively high withholding tax rates and lacks a binding arbitration mechanism under its Mutual Agreement Procedure (MAP). Although no formal negotiations have been announced, growing pressure from the business community and recognition of the treaty’s limitations have placed it under increased scrutiny. Key reform goals include reducing tax barriers, modernizing LOB provisions, and introducing binding arbitration to resolve disputes more efficiently.

Expanding and updating the US tax treaty network—both by forging new agreements and modernizing existing ones—is vital to maintaining the country’s competitiveness in a rapidly evolving global tax landscape.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe