As more details about the forthcoming taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. reform bill emerge, one compromise appears increasingly likely: repealing the deduction for state and local income and sales taxes, but retaining the deduction for property taxes. In the past, we’ve explored the implications of the repeal of the state and local tax (SALT) deduction in full, but what would a property tax deduction look like on its own? Here are five implications of retaining the property tax deduction.

First, it would be much smaller than the current SALT deduction: the property tax deductionA tax deduction allows taxpayers to subtract certain deductible expenses and other items to reduce how much of their income is taxed, which reduces how much tax they owe. For individuals, some deductions are available to all taxpayers, while others are reserved only for taxpayers who itemize. For businesses, most business expenses are fully and immediately deductible in the year they occur, but others, particularly for capital investment and research and development (R&D), must be deducted over time. accounted for just over one-third (33.9 percent) of all state and local taxes deducted in 2015, the most recent year for which data are available.

Second, it strongly benefits the middle class. Whereas the SALT deduction as a whole favors high-income earners disproportionately (since the federal income tax is highly progressive), the property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. component provides a larger deduction, as a share of adjusted gross incomeFor individuals, gross income is the total pre-tax earnings from wages, tips, investments, interest, and other forms of income and is also referred to as “gross pay.” For businesses, gross income is total revenue minus cost of goods sold and is also known as “gross profit” or “gross margin.” , to middle-income earners. This makes sense, as (1) property taxes lack progressive rate structures and (2) while those with higher incomes also have larger property holdings, the value of property doesn’t scale with income. A household earning ten times the median income is unlikely to own property worth ten times the median amount.

| Adjusted Gross Income | Full SALT Deduction | Property Tax Deduction | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Source: IRS Statistics of Income (2015); Tax Foundation calculations | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $0 – $24,999 | 2.1% | 1.6% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $25,000 – $49,999 | 2.1% | 1.3% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $50,000 – $99,999 | 4.0% | 2.0% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $100,000 – $499,999 | 6.7% | 2.6% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| $500,000 + | 7.1% | 1.1% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

As a percentage of AGI, households with incomes between $25,000 and $50,000 claim only 29 percent of what households with incomes above $500,000 claim on the SALT deduction as a whole (2.1 vs. 7.1 percent of AGI), but their property tax deduction actually represents a 20 percent larger share of AGI (1.3 vs. 1.1 percent of AGI). The deduction as a share of income is most generous to middle-income families, unlike the full SALT deduction.

Third, it does not penalize low-tax states the same way that the full SALT deduction does. Under the current system, itemizers can deduct property taxes as well as either income or sales taxes. Itemizers in the nine states which forgo a wage income tax would currently take the sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. deduction, which is generally estimated on IRS worksheets rather than relying on actual receipts. This approach tends to be less generous, and of course income tax burdens are usually higher than sales tax burdens, so residents of states which forgo an income tax are generally net losers under the current regime.

The effect is most pronounced in a state like New Hampshire, which taxes neither sales nor wage income, or Alaska, which only has local option sales taxes. Still, even states which impose all of the major taxes are often net losers, as the state and local tax deduction redistributes money from lower-income filers, particularly those in low-tax states, to higher-income individuals in high-tax jurisdictions.

The property tax component on its own, though, looks rather different. Property taxes are a major source of local revenue in all states. Suddenly, a state like Texas has a deduction as a percentage of AGI that is above the median. Under the full SALT deduction, Texas’s deduction is less than half the median. A quarter of all filers (25.1 percent) take the property tax deduction, slightly less than the 29.6 percent of filers who take any portion of the SALT deduction.

| State | AGI Per Filer | % Claiming | As % of AGI | State Share | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Source: IRS Statistics of Income (2015); Tax Foundation calculations | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Alabama | $54,457 | 20.9% | 0.6% | 0.3% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Alaska | $69,181 | 19.9% | 1.3% | 0.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Arizona | $59,031 | 24.9% | 1.1% | 1.0% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Arkansas | $54,162 | 18.4% | 0.7% | 0.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| California | $77,814 | 27.1% | 2.0% | 15.1% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Colorado | $72,175 | 28.9% | 1.1% | 1.1% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Connecticut | $95,100 | 37.4% | 3.0% | 2.7% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Delaware | $63,604 | 28.3% | 1.2% | 0.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Florida | $63,729 | 18.5% | 1.5% | 4.9% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Georgia | $59,979 | 26.9% | 1.4% | 2.0% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Hawaii | $60,771 | 22.5% | 0.8% | 0.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Idaho | $54,253 | 25.3% | 1.2% | 0.3% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Illinois | $71,672 | 27.9% | 2.6% | 6.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Indiana | $55,863 | 20.4% | 0.8% | 0.8% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Iowa | $60,544 | 26.5% | 1.6% | 0.7% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Kansas | $62,479 | 22.9% | 1.3% | 0.6% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Kentucky | $53,742 | 23.0% | 1.0% | 0.6% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Louisiana | $56,261 | 16.5% | 0.6% | 0.4% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Maine | $55,070 | 25.7% | 2.0% | 0.4% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Maryland | $74,992 | 36.4% | 2.1% | 2.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Massachusetts | $87,877 | 32.9% | 2.3% | 3.7% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Michigan | $58,851 | 24.2% | 1.7% | 2.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Minnesota | $70,832 | 31.8% | 1.6% | 1.7% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Mississippi | $47,412 | 17.6% | 0.8% | 0.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Missouri | $58,426 | 23.3% | 1.2% | 1.1% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Montana | $55,864 | 25.3% | 1.3% | 0.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Nebraska | $61,498 | 24.4% | 1.6% | 0.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Nevada | $61,066 | 20.1% | 1.0% | 0.4% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Hampshire | $71,673 | 29.4% | 3.0% | 0.8% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Jersey | $83,649 | 35.7% | 4.1% | 7.9% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New Mexico | $50,883 | 19.4% | 1.0% | 0.3% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| New York | $81,397 | 24.9% | 2.7% | 11.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| North Carolina | $58,812 | 25.6% | 1.3% | 1.8% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| North Dakota | $69,081 | 14.8% | 0.7% | 0.1% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ohio | $57,774 | 23.1% | 1.7% | 2.9% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Oklahoma | $58,918 | 20.0% | 0.9% | 0.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Oregon | $62,956 | 32.0% | 2.1% | 1.3% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Pennsylvania | $65,340 | 25.7% | 2.0% | 4.4% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Rhode Island | $63,040 | 30.1% | 2.6% | 0.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| South Carolina | $54,870 | 24.2% | 1.0% | 0.6% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| South Dakota | $61,482 | 14.5% | 0.9% | 0.1% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Tennessee | $56,763 | 17.0% | 0.8% | 0.8% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Texas | $66,970 | 19.1% | 1.8% | 7.9% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utah | $62,716 | 31.8% | 1.2% | 0.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Vermont | $58,290 | 25.5% | 2.6% | 0.3% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Virginia | $73,957 | 32.4% | 1.8% | 2.8% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Washington | $76,083 | 27.7% | 1.7% | 2.4% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| West Virginia | $50,786 | 14.8% | 0.5% | 0.1% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wisconsin | $61,406 | 28.5% | 2.2% | 2.0% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wyoming | $74,792 | 19.3% | 0.7% | 0.1% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| District of Columbia | $93,221 | 25.2% | 1.2% | 0.2% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| U.S. Total | $67,786 | 25.1% | 1.8% | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

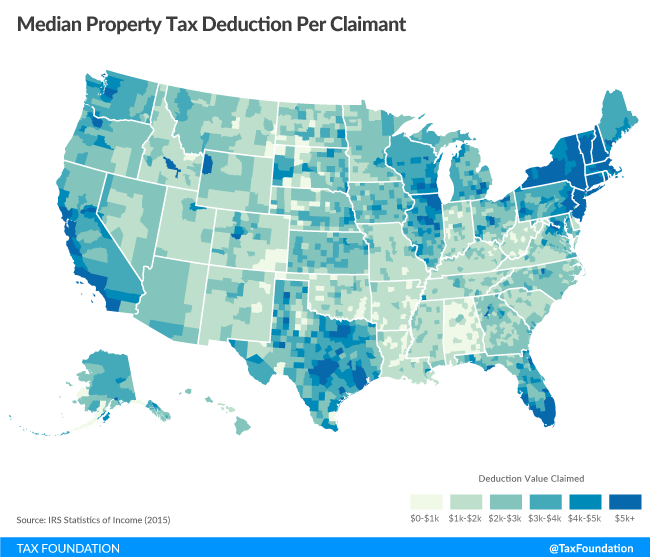

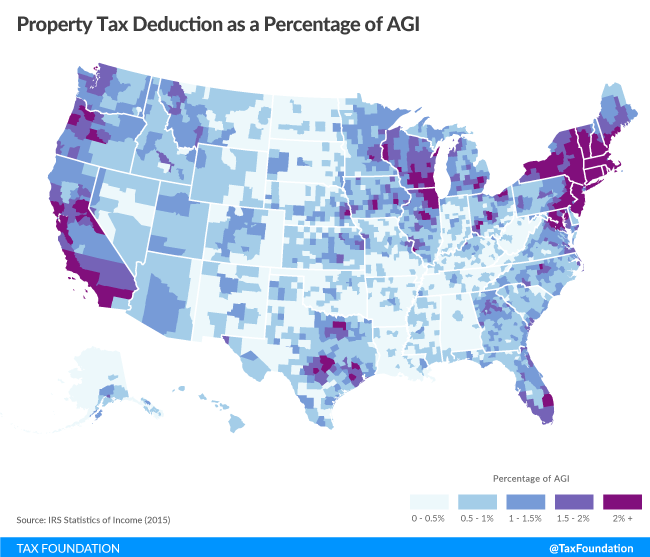

Fourth, some states and localities continue to benefit disproportionately from a scaled-down, property tax-only deduction, just as they do under the broader provision. The majority of the value of the property tax deduction, like the state and local tax deduction as a whole, flows to a small number of states. Just six states (California, New York, New Jersey, Texas, Illinois, and Florida) claim more than 50 percent of the property tax deduction.

In twenty-five counties, the property tax deduction is worth 4 percent of AGI or more, led by Putnam and Rockland Counties in New York, each at 5.5 percent. Of these top counties, sixteen are in New Jersey, seven are in New York, and two are in Illinois. At the other end of the spectrum are counties—generally low-income and low-population—where the deduction’s value is negligible or even non-existent. The median value of the deduction by county is 0.8 percent of AGI.

In Westchester County, New York, the property tax deduction alone is worth $5,548 per filer and $15,033 per deduction claimant. Among all counties, however, the mean value per filer taking the deduction is a far more modest $2,333. The interactive county map below allows you to toggle between the property tax deduction as a percentage of AGI and the amount per filer claiming the deduction. Static versions of these maps can be found here and here.

{kind=link}

{kind=link}

Interactive County-Level Map

Fifth, retaining the property tax deduction leaves a lot of revenue on the table, as it is worth about one-third of the $1.8 trillion (or $1.7 trillion on a dynamic basis) “pay-for” the repeal of the state and local tax deduction would provide over the ten-year revenue window. Although it lacks the highly regressive features of the broader SALT deduction, and distributes benefits more broadly across states, it still represents a subsidy to taxpayers in higher-income and higher-tax jurisdictions.

The property tax, even more than other forms of state and local taxation, generally pays for highly localized public expenditures—schools, roads, police and fire protection, utilities, parks, and other local amenities—for which subsidization by less affluent jurisdictions makes little sense. On the other hand, it is sometimes argued that a large proportion of local government expenditures represent investments in human and physical capital that would be deductible as capital expenditures under an ideal tax code. To the extent that this argument has merit, it is stronger with property taxes (a chiefly local revenue measure) than income or sales taxes.

If Congress is to adopt meaningful federal tax reform, it will require significant base-broadening “pay-fors” to pay down rate reductions and structural reform. The state and local tax deduction is an important piece of the puzzle. Saving the property tax deduction makes the math somewhat more difficult, but still leaves clear paths forward. Going further and preserving the entire SALT deduction, however, might send would-be reformers back to the drawing board.

Share this article