Tax Policy and Economic Downturns in Europe

6 min readBy:Over the past 15 years, Europe has experienced three major economic downturns. What began with the global financial crisis in 2008-09 ultimately evolved into the European public debt crisis (2010-12) and after some years of relative stability, the coronavirus outbreak hit Europe as well (2020-21). Policymakers reacted to these downturns with various measures to soften their impact. But how did these policies—which were often temporary—affect revenues, deficits, and countries’ economies?

Revenue and Deficit Trends in the Eurozone

The global financial crisis caused significant turmoil in the European financial sector, culminating in the European public debt crisis, as well as a double-dip recessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years. that the Eurozone economies did not recover from until 2015. Between 2008 and 2010, tax revenues fell by 6 percent in real terms and only started rising again in 2011. TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. revenues reached the pre-crisis level in 2015 and rose further until 2019. During the pandemic, tax revenues fell by 7 percent in 2020, before climbing above the pre-crisis level immediately in 2021, while the pandemic was far from over and still dominated economic policy debates throughout the year.

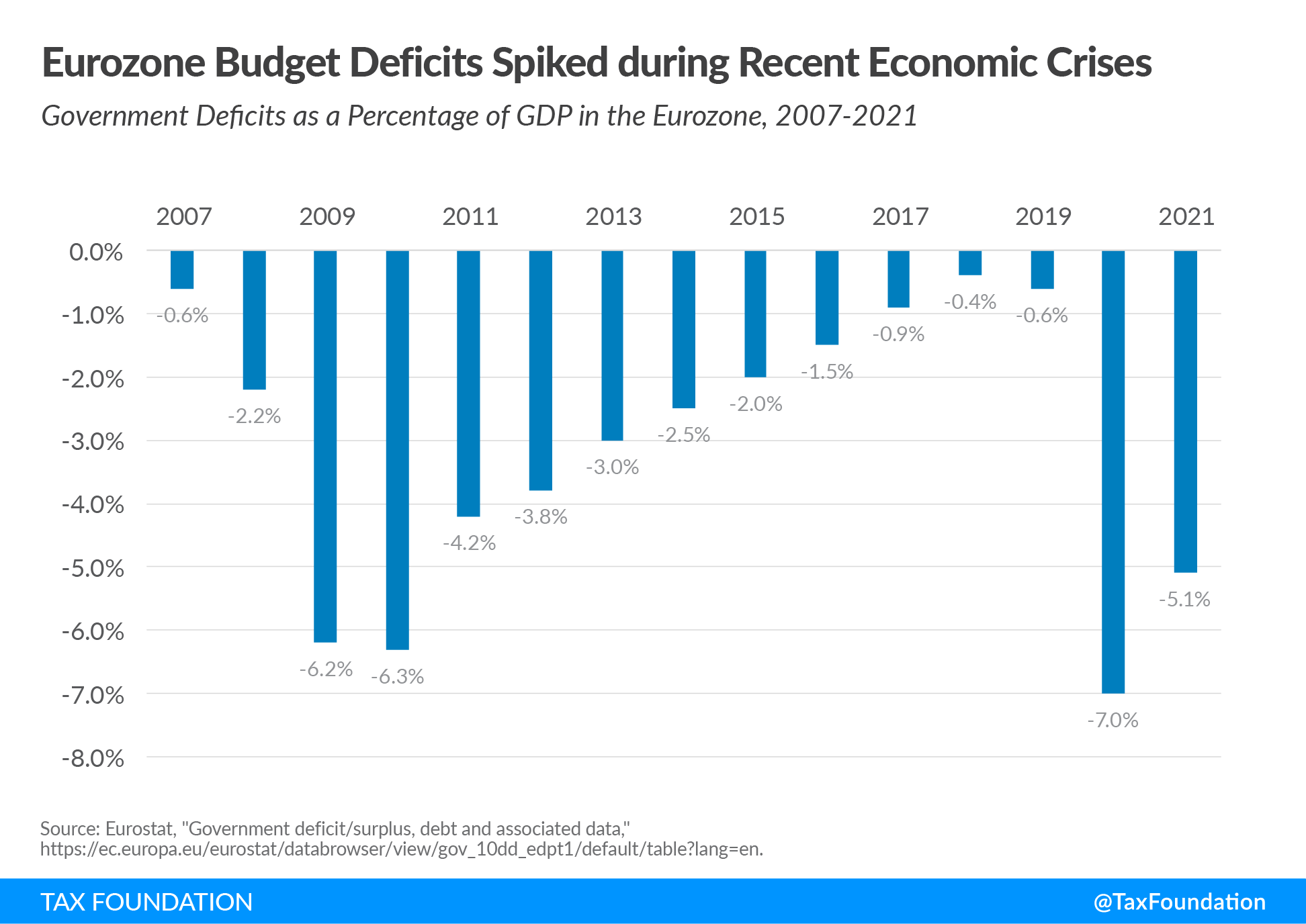

As expected, budget deficits spike in the most severe years of crisis (2009, 2010, 2020, 2021) and recover when waters are calmer. The long recovery back to a balanced budget after 2010 can be attributed to fiscal policy measures aimed at the survival of the single currency and continued support measures to help economies in southern Europe recover from the public debt crisis. The closest the Member States of the Eurozone came to a balanced budget over the last decade was in 2018 with an aggregate deficit of 0.4 percent.

A budget deficit of 5.1 percent in 2021 demonstrates that the fiscal impact of the COVID-19 pandemic was far from over at this point. This makes the high tax revenues in 2021 appear even more remarkable as one would expect higher spending and lower taxes in times of crises, but not higher spending and an all-time high of tax revenues. When governments support their economies in times of crisis, we would either expect a decrease in tax revenues due to tax cuts or a larger budget deficit due to increased spending. Observing higher spending and higher tax revenues simultaneously hints at ineffective relief policies—governments raising more money from their citizens despite lower economic activity—or governments’ distributional concerns outweighing their desire to combat the downturn.

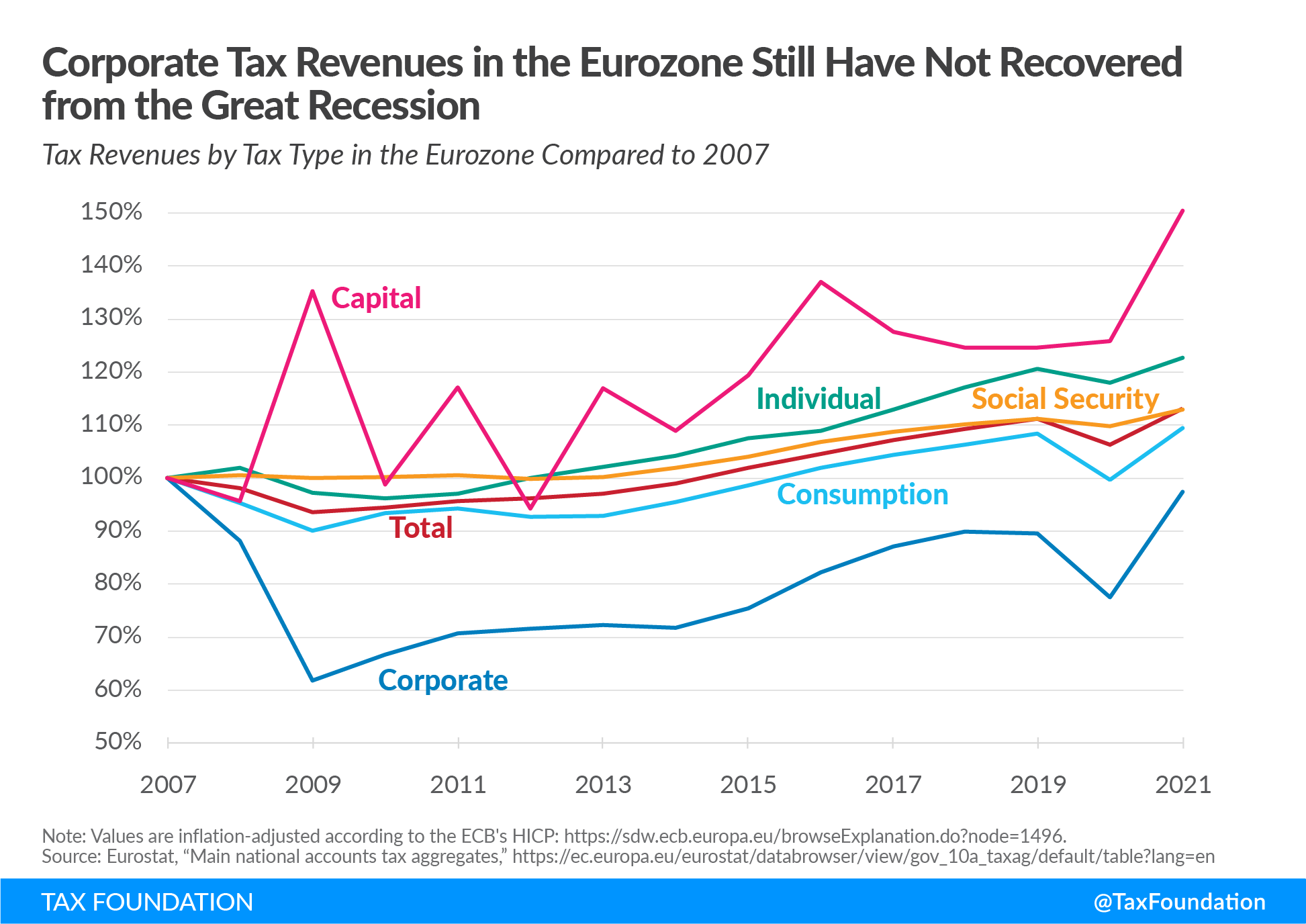

Figure 2 shows that during all three downturns, the different types of taxes vary in their reliability as sources of government revenue, with corporate taxes and capital taxes being the most volatile, followed by consumption taxes. The revenue of consumption taxes closely resembles the trend of total tax revenues. Revenue from both social contributions and income taxes were relatively unaffected by each of the crises and only saw increases outside of crisis periods.

Policy Responses to the Crises

The effects of each economic downturn on tax revenues and budget deficits are only partly explained by automatic stabilizers—the additional outlays or revenues incurred due to changes in macroeconomic conditions (e.g., higher budget deficits due to increased unemployment, less income tax revenue raised, and more unemployment benefits paid out) without any action by the government. Beyond automatic stabilizers, governments devoted significant resources to discretionary fiscal policy, often implemented as temporary measures.

In the global financial crisis, central banks reacted with expansionary monetary policy to secure the financial sector and governments bailed out banks. Expansionary monetary policy entailed a sharp decrease in central bank lending rates and liquidity support to banks. In addition, there were tax relief and subsidies for part-time unemployment. The majority of these measures were temporary, like the German car-scrapping premium. Most of these measures were aimed at stabilizing households’ consumption. Similar cuts in value-added taxes and social contributions also affected businesses, but this only constituted approximately one-fifth of the total effect on reduced revenue.

The reaction to the European public debt crisis was different. As public debt accrued, driven by efforts to alleviate the global financial crisis, policymakers mainly reacted to it by introducing measures for more fiscal prudence. In the affected southern European countries, social insurance payments such as pensions were cut, and income taxes increased. To ensure the credibility of these actions, they were made permanent. Another important feature was the tightening of the Stability and Growth Pact (SGP) to pave the way for prudent government finances and prevent future debt crises. The EU-wide budget deficits came from continued support schemes after the financial crisis, the missing recovery especially in southern Europe, and the fiscal support for the struggling countries.

Government support schemes during the COVID-19 pandemic were also largely temporary, including subsidies to promote continued employment (especially in times of lockdowns), various tax cuts, and tax reporting provisions to prevent firms from going bankrupt. For example, Germany cut its standard VAT rate from 19 percent to 16 percent, and the reduced rate from 7 percent to 5 percent for the second half of 2020. Other countries took similar measures. Greece, France, and Spain suspended certain tax payments temporarily and the Netherlands introduced wage subsidies for distressed businesses.

The EU further introduced the Pandemic Crisis Support safety net which consists mainly of loan guarantees, and various temporary instruments to protect jobs across Europe. Additionally, the EU loosened the rules for state aide to provide Member States with maximum flexibility in targeting their country-specific problems. Overall, the final policy response was a mix of tax cuts or deferrals and more pronounced spending increases. The large role played by tax deferrals and stalled payments, which were phased out in 2021, partly explains the resurgence of tax revenues in that year.

Overall Trends in Taxation

Throughout the past 15 years, overall taxation levels in the Eurozone have been rising. In 2007, the tax-to-GDP ratio stood at 39.1 percent and increased after a temporary decline during the global financial crisis to 41.2 percent in 2021. The ratio increased even through 2020 and 2021 which can mainly be explained by sharp but temporary declines in GDP during the COVID-19 pandemic. The fact that tax-to-GDP ratios often resurge to a higher level after economic crises is rooted in the need for governments to recover the costs they incurred during the crises for fiscal sustainability.

The tax mix on the other hand has not changed significantly, with the only notable difference lying in the decrease of corporate taxes from 8 percent of total tax revenues in 2007 to 6 percent in 2021. For the other categories, their share of total revenues has remained relatively constant.

The large majority of all crisis relief measures in the past were temporary. And while some temporary policies can help in a crisis, policymakers should focus their efforts on sustainable policies that support growth and the resilience of businesses (and government coffers) over the long term.

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign UpAbout the Author

Joost Haddinga is a Transatlantic Tax Fellow with the Tax Foundation’s Center for Global Tax Policy.