The EU’s Questionable VAT Policy

8 min readBy:Key Points

- The value-added tax (VAT) compliance gap—the additional VAT revenue that could be collected if all taxpayers, consumers, and businesses fully complied with VAT rules—continues to increase, reaching €128 billion in 2023.

- Seventy-five percent of the VAT compliance gap comes from just six countries: France, Germany, Italy, Poland, Romania, and Spain.

- The VAT actionable policy gap—the additional VAT revenue that could realistically be collected by eliminating reduced rates and certain exemptions—amounted to €773.5 billion in 2024, six times the compliance gap.

According to the latest “VAT gap” report published by the European Commission, value-added tax (VAT) compliance decreased in 2023. The VAT compliance gap—the additional VAT revenue that could be collected if all taxpayers, consumers, and businesses fully complied with VAT rules—increased from 7.9 percent in 2022 (€101 billion) to 9.5 percent in 2023 (€128 billion).

In 2023, the largest compliance gaps were observed in Romania (30 percent), Malta (24.2 percent), Poland (16 percent), Lithuania (15.1 percent), and Italy (15 percent). The smallest compliance gaps were registered in Austria (1 percent), Finland (3 percent), Cyprus (3.3 percent), and Portugal (3.6 percent). However, in absolute terms, 75 percent of the VAT gap comes from just six countries: France, Germany, Italy, Poland, Romania, and Spain.

This year’s report also includes selected European Union (EU) candidate and potential candidate countries. In 2023, VAT compliance gaps ranged from 24.6 percent in Albania to 8.1 percent in Kosovo and 5.4 percent in Georgia.

EU VAT Compliance Gaps Increased in 2023

| Country | 2023 VAT Compliance Gap (%) | Change in Percentage Points Between 2022 and 2023 |

|---|---|---|

| Belgium | 12.30% | 0.6 pp |

| Bulgaria | 8.60% | 2.3 pp |

| Czechia | 8.00% | -0.2 pp |

| Denmark | 8.90% | 0.9 pp |

| Germany | 9.70% | 3.1 pp |

| Estonia | 10.30% | 5.1 pp |

| Ireland | 8.30% | 6 pp |

| Greece | 11.40% | -1.1 pp |

| Spain | 7.60% | 3.5 pp |

| France | 5.60% | 0.5 pp |

| Croatia | 7.70% | -3.7 pp |

| Italy | 15.00% | 0.6 pp |

| Cyprus | 3.30% | -3 pp |

| Latvia | 5.40% | 3.5 pp |

| Lithuania | 15.10% | 2.9 pp |

| Hungary | 7.40% | 5 pp |

| Malta | 24.20% | 0.6 pp |

| Netherlands | 7.00% | -2.5 pp |

| Austria | 1.00% | -2 pp |

| Poland | 16.00% | 4.8 pp |

| Portugal | 3.60% | -0.5 pp |

| Romania | 30.00% | 3.4 pp |

| Slovenia | 4.90% | -3.5 pp |

| Slovakia | 10.50% | -1 pp |

| Finland | 3.00% | 0.9 pp |

| Sweden | 5.30% | 1.8 pp |

| EU Average | 9.50% | 1.6 pp |

| Albania | 24.60% | 4.1 pp |

| Georgia | 5.40% | 0 pp |

| Kosovo | 8.10% | -3.4 pp |

The VAT compliance gap increased in 17 EU countries and decreased in 9 countries. To understand this average increase in the compliance gap, a more thorough analysis of the VAT compliance gap is needed.

What Causes the VAT Compliance Gap?

The VAT compliance gap is caused not only by VAT avoidance or gaps in enforcement but also by unpaid VAT due to bankruptcies, insolvencies, or legal taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. optimization.

Using Eurostat data on bankruptcies, we find a positive but low correlation of 0.19 between the increase in the number of bankruptcies and the decrease in compliance. In other words, when bankruptcies rise, compliance tends to dip, as VAT owed becomes uncollectable. Nevertheless, in the Netherlands, where VAT compliance increased, a stark increase in bankruptcies was also observed. Therefore, the VAT compliance gap might be revised upward in the 2026 release of the “VAT gap” report. According to the Commission’s report, the overall decrease in compliance was due to VAT revenue growing at a slower pace than the estimated total liability.

In the 2025 “VAT gap” report, the VAT compliance gap for the years 2021 and 2022 was also revised upward, by an average of 0.6 and 0.9 percentage points, respectively. However, the 2021 data was also revised upward in last year’s report (2024) by another 1 percentage point. As the report notes, this was “due to the extraordinary measures introduced (and revoked) in those years” and to the “inconsistent treatment of deferrals, and the lower quality of national statistics.” As we highlighted in past years’ posts, in many countries, 2020 VAT payments were pushed into the 2021 fiscal year. This postponement artificially increased VAT tax collection in 2021, while having no impact on the VAT tax liability, explaining the artificial increase in VAT compliance in 2021. While the VAT compliance gap for the year 2021 was revised upward by 1.6 percentage points on average, for countries like Croatia, Czechia, Germany, Italy, Latvia, and the Netherlands, the VAT compliance gap was revised upward by more than 4 percentage points.

The VAT compliance gap will likely continue to increase slightly in the coming years. The report estimates for 2024 show that the VAT compliance gap in absolute terms is expected to increase in 12 (8, in relative terms) of the 22 countries for which estimates were available. Additionally, 2024 bankruptcy data already published by Eurostat portrays a somber perspective on businesses operating in the EU, as bankruptcies continued to increase in 20 EU countries between 2023 and 2024. The biggest increases in bankruptcies were observed in the Netherlands (30.3 percent), Sweden (30 percent), Spain (25.5 percent), and Germany (22.9 percent).

The European Commission is prioritizing efforts to reduce the VAT compliance gap by intensifying actions against fraud and avoidance. However, recent research indicates that current VAT fraud estimates are methodologically flawed and consistently overstated. Therefore, before introducing new VAT policies, a more robust assessment of the potential impact of these measures is needed.

What Is the VAT Actionable Policy Gap?

While the European Commission focuses on improving VAT compliance, policy is a major contributor to VAT revenue losses. The VAT actionable policy gap—the additional VAT revenue that could realistically be collected by eliminating reduced rates and certain exemptions—is 27.1 percent (in 2024, the latest available data). In absolute terms, the VAT actionable policy gap amounted to €773.5 billion in 2024 and €743.2 billion in 2023, six times the compliance gap.

The VAT policy gap is made up of two components: the rate gap and the exemption gap. The former represents lost VAT revenue due to reduced VAT rates, while the latter represents lost VAT revenue due to certain goods and services being exempt from the VAT. Policymakers often justify exemptions and reduced rates with arguments that they promote the consumption of certain goods and services to address equity, environmental, and other policy goals. But exemptions and reduced rates are bad policy because they distort consumption, inefficiently deliver fiscal benefits, add complexity for businesses, and reduce revenue, forcing governments to rely on less economically efficient revenue sources.

However, there are some services—namely, imputed rents, the provision of publicly provided goods, and financial services—that are VAT-exempt because it would be difficult to levy VAT on them. Subtracting the amount of lost VAT revenue caused by these services from the general policy gap leaves us with the actionable policy gap (i.e., the actionable exemption gap plus the rate gap), which is the amount of additional VAT revenue lawmakers could realistically raise by eliminating reduced rates and certain exemptions.

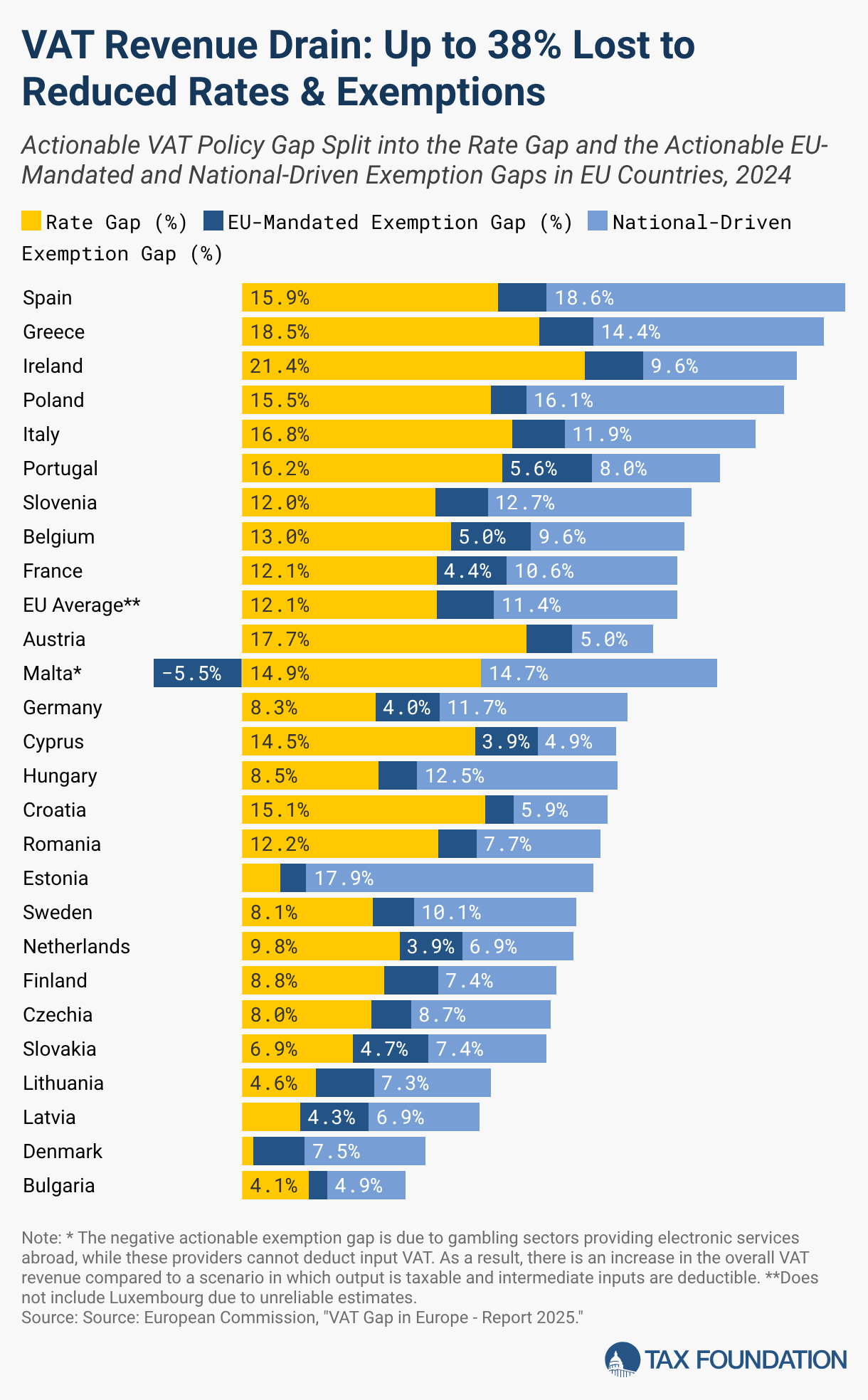

In 2024, the average actionable policy gap for the EU was 27.1 percent—of which 12 percent was due to reduced rates (rate gap) and 15 percent to the actionable portion of the exemption gap.

The rate gap is smaller in countries that rely on reduced rates less, such as Denmark (0.7 percent), Estonia (2.4 percent), Latvia (3.6 percent), Bulgaria (4.1 percent), and Lithuania (4.6 percent). However, the rate gaps in Ireland (21.4 percent), Greece (18.5 percent), Austria (17.7 percent), Italy (16.8 percent), Portugal (16.2 percent), Spain (15.9 percent), Poland (15.5 percent), and Croatia (15.1 percent) show significant forgone revenue because of reduced rates. The highest actionable exemption gaps are observed in Spain (21.7 percent), Estonia (19.5 percent), Poland (18.3 percent), Greece (17.8 percent), Slovenia (16 percent), Germany (15.7 percent), Italy (15.2 percent), and France (15 percent).

Additionally, this year’s report distinguishes between the national policy-driven VAT exemption gap and the EU policy-mandated VAT exemption gap, exemptions required by the VAT directive. On one hand, the highest EU policy-mandated exemption gaps were observed in Portugal (5.6 percent) and Belgium (5 percent), while the smallest gaps were observed in Bulgaria (1.2 percent), Estonia (1.6 percent), and Croatia (1.8 percent). These gaps were primarily driven by the exemptions applied to private health insurance, private education, and insurance-related activities.

On the other hand, the highest national policy-driven exemption gaps were observed in Spain (18.6 percent), Estonia (17.9 percent), and Poland (16.1 percent). The national policy-driven exemption gap was smaller in Bulgaria (4.9 percent), Cyprus (4.9 percent), Austria (5 percent), and Croatia (5.9 percent).

Overall, the highest actionable policy gaps were observed in Spain (37.6 percent), Greece (36.3 percent), Ireland (34.7 percent), Poland (33.7 percent), Italy (32 percent), Portugal (29.8 percent), Slovenia (27.9 percent), Belgium (27.6 percent), and France (27.1 percent). Spain’s actionable policy gap was due in part to the application of different indirect taxes in the Canary Islands, Ceuta, and Melilla. The actionable policy gap was smaller in Bulgaria (10.2 percent), Denmark (11.4 percent), Latvia (14.8 percent), and Lithuania (15.5 percent).

According to the data in the latest “VAT gap” report, between 2022 and 2024, the VAT actionable policy gap increased from 26.1 percent to 27.1 percent. The average actionable policy gap for the EU increased by 1 percentage point, of which 0.2 percentage points were due to the increase in the rate gap and 0.8 percentage points were due to the increase in the actionable exemption gap.

However, in the previous “VAT gap” report (2024), for the year 2022, the VAT actionable policy gap was 19 percent, 7 percentage points below the figure shown in this year’s report for the same indicator. This change is due to a large change in the actionable exemption gap data. The 2024 report estimated the EU’s actionable exemption gap for 2022 at 7 percent, while the 2025 report raises this figure to 14.15 percent. While the average estimate of the actionable exemption gap increased by 7.2 percentage points, country-level revisions ranged from 1.2 percentage points in Cyprus to 10.2 percentage points in Belgium. While the report notes that financial and insurance services are now treated as actionable exemptions, these two sectors only account for up to 2.7 percentage points of the 7.2 percentage point difference.

Nevertheless, both financial and insurance services are subject to different forms of taxation across EU Member States, beyond the VAT framework. In France, the insurance premium tax applicable to motor third‑party liability insurance reaches up to 33 percent.

The upward trend of the VAT actionable policy gap will likely change in 2025, as the temporary rate reductions to VAT on energy and food products, as a price support measure to cushion the impact of a sharp rise in energy prices and inflation, expired. However, some countries continued to introduce reduced rates on a variety of goods and services to increase equity or to stimulate certain sectors of the economy. If no new important rate reductions are introduced, the VAT base will broaden, decreasing the VAT rate gap and consequently the actionable policy gap in 2025.

As the compliance gap is expected to increase slightly in the following years, policymakers will need to closely monitor both compliance and rate gaps. In a survey regarding companies’ barriers to conducting business in the EU single market, VAT ranked first, at 17 percent. Therefore, policymakers should invest in reforming VAT systems to close both compliance and policy gaps in ways that improve the overall efficiency of their tax systems.

Subscribe to our free newsletter to get the latest tax data, news and analysis.Stay informed on the tax policies impacting you.

About the Author

Cristina Enache writes on the economics of tax policy and is the author of the Spanish Regional Tax Competitiveness Index. She was formerly the Director of Research at Civismo, an economic research organization based in Spain. She also served as head of research at Institución Futuro, a regional think tank based in Navarra in northern Spain. She is also currently Secretary-General at the World Taxpayers Associations and General Manager of the Spanish Taxpayers Union, which she joined in 2016.