Update: On December 27, 2020, President Donald Trump signed the Consolidated Appropriations Act, 2021 (H.R. 133) into law. Explore our our original COVID-19 Relief Package summary.

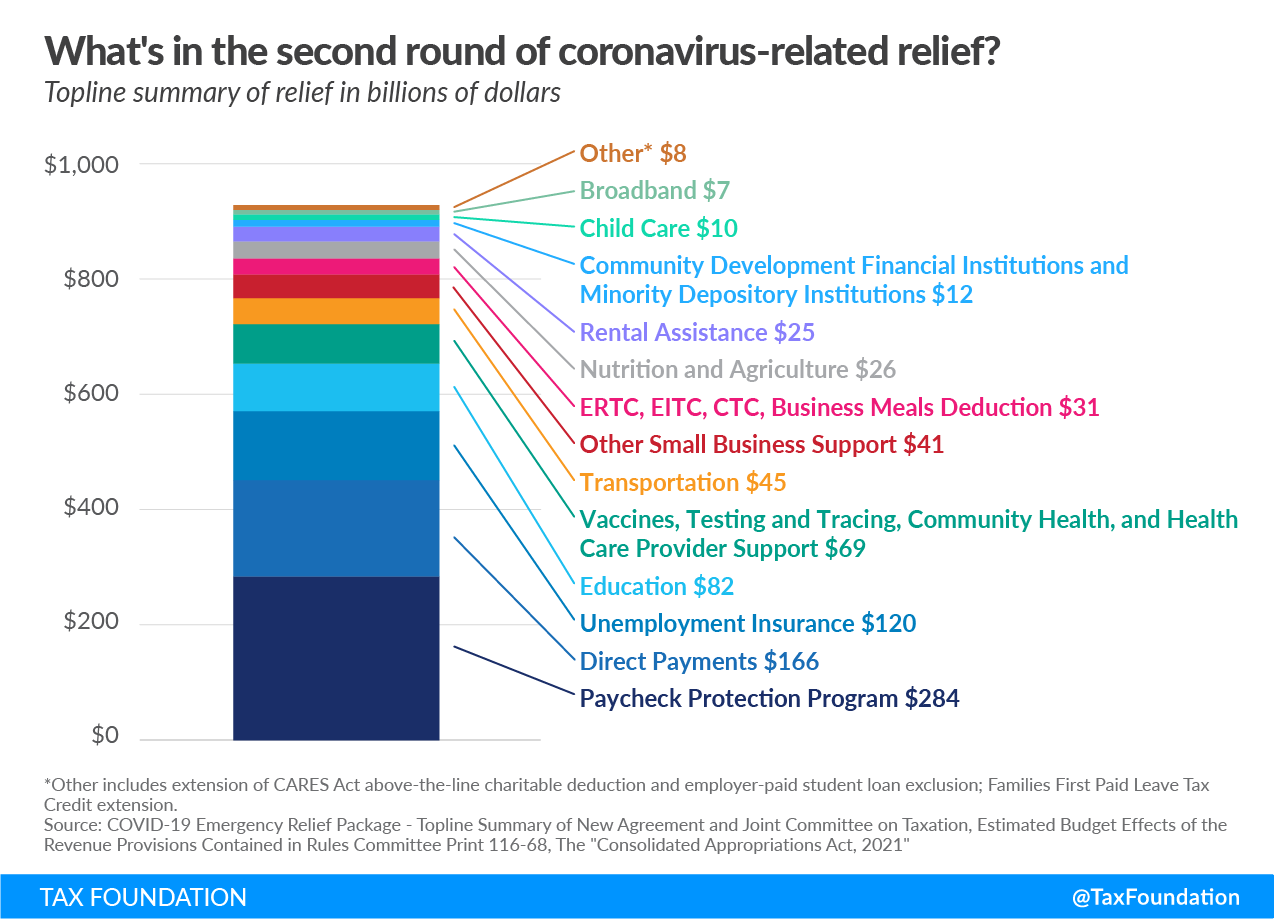

Leadership in the U.S. House and Senate came to an agreement in December over the details of a $900 billion COVID-19 relief bill, (Consolidated Appropriations Act, 2021) to be attached to a broader $1.4 trillion omnibus which will fund the federal government for the 2021 fiscal year. The COVID-19 relief bill extends and modifies several provisions first enacted in the CARES Act, Congress’s $2.2 trillion pandemic relief law that was passed in March. With this package, lawmakers will have responded to the coronavirus and related economic hardship with a record-setting $3.4 trillion of fiscal support.

Disclaimer: The information in this FAQ may not apply to your specific taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. situation. Please direct any tax preparation and filing questions to a professional tax preparer or the Internal Revenue Service (IRS). The Tax Foundation cannot answer specific questions about your tax situation or assist in the tax filing process.

The Basics

- What is in the new COVID-19 relief package?

- What exactly is the second round of recovery rebates?

- How much of a rebate will I receive this time?

- How do I get my rebate?

Rebates for Dependents

- Is there any minimum income amount to qualify for the rebate and claim dependents?

- Which dependents qualify for a rebate?

- What if I had a baby in 2019 or 2020 and haven’t filed a return?

- What if I’m divorced? Does each parent receive a $500 check for each of their dependents?

Rebates and Tax Returns

- If I had high income in 2019 but lost my job, do I still qualify?

- What if my income rises in 2020 and I received a higher rebate using my 2019 return?

- If my income drops in 2020, can I get an additional rebate if I got a lower rebate based on 2019 income?

- If I make more income in 2020, do I have to pay any amount back?

Social Security Benefits

- Will those receiving Social Security benefits still receive a rebate check?

- Do I still receive a check if I am on Social Security disability benefits?

- What if I receive Supplemental Security Income but not Social Security benefits? Do I qualify for a rebate?

Paycheck Protection Program (PPP) and Payroll TaxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. Credit Changes

- Are expenses paid for with PPP loan proceeds deductible?

- How did the payroll tax credit that employers can apply to employee wages (the ERTC) change?

- If a firm is taking a loan through the Paycheck Protection Program, can it also take the ERTC?

- What is the difference between the payroll tax credit created for coronavirus-related paid sick and family leave and the ERTC?

Unemployment Insurance Changes

- Have the CARES Act unemployment benefits been extended?

- How long do these benefits last?

- How did the law change one-week waiting periods before filing for unemployment insurance?

- Who qualifies for the expanded Pandemic Unemployment Insurance?

- How does the $300 weekly boost work?

- Can someone laid off before the new law was passed qualify for the new benefits?

Other Changes

Note: You can explore all of our analysis on the latest coronavirus relief legislation at the federal, state, and international levels with our dedicated COVID-19 Tax Resource Center.

Basics of the COVID-19 Relief Package

What is in the new COVID-19 relief package (Consolidated Appropriations Act, 2021)?

The new covid-19 relief package contains approximately $900 billion of programs for individuals and businesses. It includes renewal of many programs created in the CARES Act, including the Paycheck Protection Program, the Employee Retention Tax CreditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly. , direct payments to individuals, unemployment insurance expansion, and more. Back to top

What exactly is the second round of recovery rebates?

The recovery rebates (Economic Impact Payments) are refundable tax credits. This means that the rebate decreases a taxpayer’s tax liability dollar-for-dollar, and the credit can be refunded to a taxpayer if they have no tax liability to offset.

Congress has authorized two recovery rebates in 2020: a payment as part of the CARES Act in March, and a second payment as part of Congress’s Consolidated Appropriations Act of 2021 in December.

The rebates are tax credits that will be applied to 2020 tax returns but are advanced to taxpayers now based on their 2019 adjusted gross incomeFor individuals, gross income is the total pre-tax earnings from wages, tips, investments, interest, and other forms of income and is also referred to as “gross pay.” For businesses, gross income is total revenue minus cost of goods sold and is also known as “gross profit” or “gross margin.” (AGI). The credit will be applied to 2020 tax returns using 2020’s AGI in the spring, and taxpayers will receive the difference of the credit if it is in their favor. Unlike the CARES Act recovery rebates, the IRS will only use 2019 AGI and not 2018 AGI when calculating the payment amount.

For example, if a single taxpayer with no children made $200,000 in 2019, they would not receive an advance rebate based on their 2019 income. However, if they make $35,000 in 2020, they will receive a $600 refundable tax creditA refundable tax credit can be used to generate a federal tax refund larger than the amount of tax paid throughout the year. In other words, a refundable tax credit creates the possibility of a negative federal tax liability. An example of a refundable tax credit is the Earned Income Tax Credit (EITC). on their 2020 tax return. But in reverse, if a taxpayer had a $35,000 AGI in 2019 but has $200,000 AGI in 2020, they would receive a $600 rebate now and would not have to pay it back on their 2020 tax return. Back to top

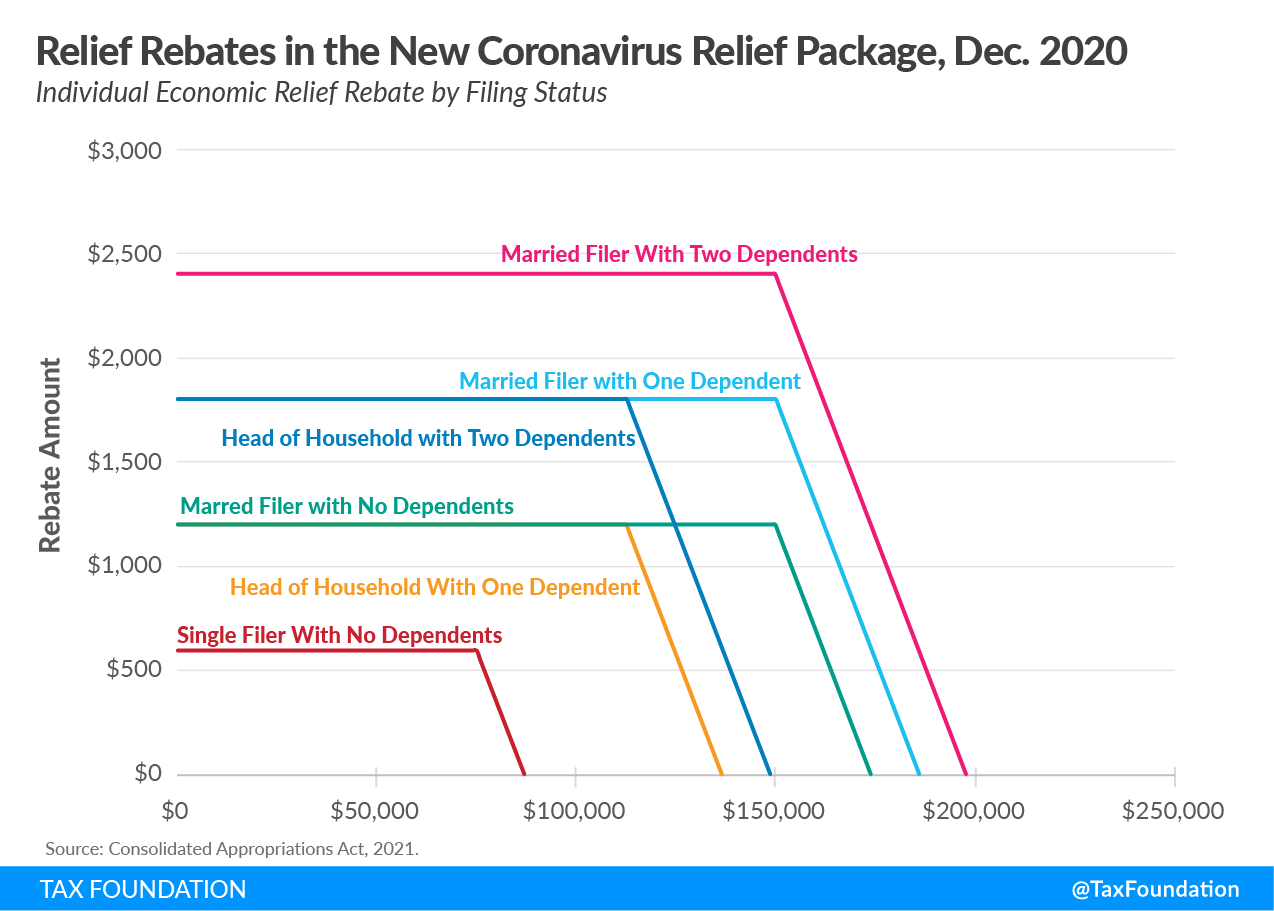

How much of a rebate will I receive this time?

Individuals with a Social Security Number (SSN) and who are not dependents may receive $600 (single filers and heads of household) or $1,200 (joint filers), with an additional rebate of $600 per qualifying child, if they have AGI under $75,000 (single), $150,000 (joint), or $112,500 (heads of household) using 2019 tax return information. The rebate phases out at $50 for every $1,000 of income earned above those thresholds. The payments phase out entirely at $87,000 for single filers with no qualifying dependents and $174,000 for those married filing jointly with no qualifying dependents.

In a change from the first round of rebates, families with members of mixed immigration status with a valid Social Security number for one spouse are eligible for the second round of rebates. Mixed status families with qualifying children can also receive a $600 additional rebate per child if the child has a Social Security number and one of the joint filers has a Social Security number.

To receive a payment, a person must have been alive on January 1, 2020. Back to top

How do I get my rebate?

For most Americans, no action is required. The IRS will use data from the most current tax returns or Social Security data to provide a rebate to Americans either via direct deposit (if such information is available) or through a paper check in the mail to the last address on file.

U.S. Treasury Secretary Steven Mnuchin said payments will begin as early as the week of December 28. The second round of payments will likely be distributed even faster than the first round given the IRS has information on file for everyone who received payments in the first round. Back to top

Rebates for Dependents

Is there any minimum income amount to qualify for the rebate and claim dependents?

No, even filers with $0 of income can file for the rebate. However, they must file a tax return to ensure the IRS can process the rebate. Additionally, they must have a Social Security Number and not be claimed as a dependent on another person’s return. Back to top

Which dependents qualify for a rebate?

The rebates use the Child Tax Credit (CTC) eligibility standards. All qualifying children who are under age 17 who have not provided for more than half of their own expenses and lived with the taxpayer for more than six months are eligible. This means that adult dependents, such as college students aged 17 and over, and elderly dependents do not qualify for the $600 rebate. Adult dependents do not qualify for their own rebate either. Back to top

What if I had a baby in 2019 or 2020 and haven’t filed a return?

If a taxpayer has not already filed a 2019 return with the name and Social Security Number (SSN) of the eligible dependent being claimed, the filer will not receive credit for those dependents born after they filed their 2018 return. However, the taxpayer may claim a $600 credit for each eligible child on their 2020 return. Back to top

What if I am divorced? Does each parent receive a $600 check for each of their dependents?

Only the parental taxpayer claiming the child as a dependent will receive the $600. Back to top

Rebates and Tax Returns

If I had high income in 2019 but lost my job, do I still qualify?

If a taxpayer’s high income in 2019 puts them above the threshold, they may be in the phaseout range and remain eligible for a partial refund. If their income is lower in 2020 when they file taxes, any remaining credit that they are eligible for will also be refunded or deducted from their tax liability when they file taxes for 2020. Back to top

What if my income rises in 2020 and I received a higher rebate using my 2019 return?

There is no penalty for receiving a rebate based on a lower income on 2019 or 2018 tax returns. If a filer’s eligible rebate rises when using 2020 tax returns, that will be remedied on their 2020 return. If the filer is given too much, the IRS will not penalize them. Back to top

If my income drops in 2020, can I get additional rebate if I got a lower rebate based on 2019 income?

Yes, if a taxpayer’s income drops in 2020, they will be eligible for any remaining rebate credit they were not able to claim using their 2019 or 2018 return. Back to top

If I make more income in 2020, do I have to pay any amount back?

No, if the amount of credit a taxpayer qualifies for in 2020 is less than it was based on their 2019 return, it does not have to be paid back and it is not considered taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. For both individuals and corporations, taxable income differs from—and is less than—gross income. . Back to top

Social Security Benefits

Will those receiving Social Security benefits still receive a rebate check?

Yes, all taxpayers are eligible for the rebate, including those receiving Social Security benefits, subject to the same eligibility rules as other taxpayers. Treasury Secretary Mnuchin announced that these beneficiaries will not have to submit a separate tax return to receive a rebate. The payment will be sent directly to their bank account associated with those benefits. Back to top

Do I still receive a check if I am on Social Security disability benefits?

Yes, Social Security beneficiaries should receive their rebate through the bank account associated with receiving benefits. Back to top

What if I receive Supplemental Security Income but not Social Security benefits? Do I qualify for a rebate?

Yes, taxpayers will qualify for the rebate as long as their Adjusted Gross Income is below the rebate thresholds depending on their filing status. If a taxpayer received Supplemental Security Income (SSI) but not Social Security benefits and did not file for taxes in 2019, the IRS will automatically send the rebate through the way taxpayers normally receive their SSI benefits, such as direct deposit, Direct Express debit card, or by paper check. Back to top

Paycheck Protection Program (PPP) and Payroll Tax Credit Changes

Are expenses paid for with Paycheck Protection Program (PPP) loan proceeds deductible?

The new COVID-19 relief package clarifies that businesses can deduct expenses paid with forgiven PPP loans. This clarification applies to old loans and to new loans with no limitations. By clarifying both that loan forgiveness is not taxable income and that expenses can be deducted, this provision results in a two-part subsidy to businesses comprised of expense deductions and tax-free loan forgiveness.

Typically, forgiven debt is considered taxable income. In the CARES Act, lawmakers specified that forgiven PPP loans would not count as taxable income. They also intended that expenses paid for with PPP loans would be deductible but did not specify so in law. Section 265 of the tax code generally prohibits firms from deducting expenses associated with income that is tax-free, so without specification, the Treasury Department ruled that expenses paid for with PPP loans were not deductible. The new clarification cements the original intent of tax-free forgiveness and deductibility into law. Back to top

How did the payroll tax credit that employers can apply to employee wages (the ERTC) change?

The new COVID-19 relief package expanded the Employee Retention Tax Credit (ERTC). Employers may claim a 70 percent tax credit (up from 50 percent) on up to $10,000 in wages paid to employees per quarter (up from $10,00 per year) through July 1, 2021, resulting in up to a maximum of a $14,000 credit per employee (up from $5,000).

To qualify, firms must be suspended due to government actions related to coronavirus or experience a 20 percent decline (down from 50 percent) in gross receipts during a calendar quarter when compared to the same quarter in the previous year. For firms with 500 employees or more (expanded from 100 employees or more), the credit can only be applied to employees not able to do their duties due to a business suspension or a lack of business. Back to top

If a firm is taking a loan through the Paycheck Protection Program, can it also take the ERTC?

The new COVID-19 relief package clarifies that firms may have access to both the Paycheck Protection Program and the ERTC but prevents a double benefit from both programs. Back to top

What is the difference between the payroll tax credit created for coronavirus-related paid sick and family leave and the ERTC?

The Families First Coronavirus Response Act created tax credits on employer-side Social Security payroll taxes to offset paid family and sick leave related to the coronavirus. These have been extended through March 2021. Back to top

These payroll tax credits are different from and unrelated to the ERTC. The ERTC is not dependent on employees taking qualified sick or family leave and was created as part of the CARES Act. Back to top

Unemployment Insurance Changes

Have the CARES Act unemployment benefits been extended?

Yes, the new COVID-19 relief package extends certain unemployment benefit programs for 11 weeks.

Pandemic Unemployment Assistance (PUA) that provides UI benefits to workers who traditionally are ineligible, such as gig economy workers and independent contractors, is extended. Federal Pandemic Unemployment Assistance (FPUA) has been extended to provide an additional $300 per week supplement to state UI compensation. Pandemic Emergency Unemployment Compensation (PEUC), which originally provided an additional 13 weeks of UI benefits, will also be extended for 11 weeks (for a combined maximum of 50 weeks) and will expire on March 14, 2021.

Individuals receiving benefits beyond the standard 26-week period as of March 14th will continue receiving them through April 5th if they have not reached their maximum number of benefit weeks.

Workers with at least $5,000 in self-employment income may be eligible for an additional $100 per week benefit as part of the Mixed Earner Unemployment Compensation to adjust for a lower UI base payment. Back to top

How long do these benefits last?

The new COVID-19 relief package expands federal unemployment benefits for 11 weeks. Federal expansions will expire on March 14, 2021.

Individuals receiving benefits beyond the standard 26-week period as of March 14th will continue receiving them through April 5th if they have not reached their maximum number of benefit weeks. Back to top

How did the law change one-week waiting periods before filing for unemployment insurance?

The new law incentivizes states to end one-week waiting periods by providing 100 percent federal financing of the first week for states without one-week waiting periods. It will be up to each individual state to remove existing one-week waiting periods. Back to top

Who qualifies for the expanded Pandemic Unemployment Insurance?

Workers must meet these three qualifications: 1) ineligible for any other state or federal unemployment benefits; 2) unemployed, partially unemployed, or cannot work due to the COVID-19 public health emergency; and 3) cannot telework or receive paid leave. This includes workers like those who are self-employed, independent contractors, gig economy workers, and those who do not have sufficient work history to qualify for regular benefits.

These workers are now eligible for a temporary federal program called Pandemic Unemployment Assistance that provides 11 weeks of unemployment benefits. Back to top

How does the $300 weekly boost work?

The new COVID-19 relief package that provides the $300 weekly boost is fully funded by the federal government through the Federal Pandemic Unemployment Assistance (FPUA) program to augment the regular unemployment benefit amount an unemployed worker receives. States are not authorized to reduce the amount or duration of their unemployment compensation during the time of the federal expansion. Back to top

Can someone laid off before the new law was passed qualify for the new benefits?

Yes. The $300 weekly boost will be provided as a supplement to those who are already receiving unemployment compensation at the state level.

Additionally, the renewed Pandemic Unemployment Assistance program provides benefits (including the $300 boost) for unemployment, partial unemployment, or inability to work that ends any week beginning after April 5, 2021. These benefits can be paid retroactively to those who qualify. Back to top

Other Changes

How Have the Child Tax Credit and Earned Income Tax Credit Been Changed?

The new COVID-19 relief package provides a “lookback adjustment” for both the Child Tax Credit and the Earned Income Tax Credit. Both tax credits phase in as taxpayers earn more income. Since many taxpayers may have lost income in 2020, that may have reduced the number of credits they are eligible for when they file taxes in the spring.

The lookback rule will help taxpayers prevent this loss of tax credit by allowing 2019 income to be used to determine an individual’s credit eligibility for the 2020 tax year. Back to top

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe