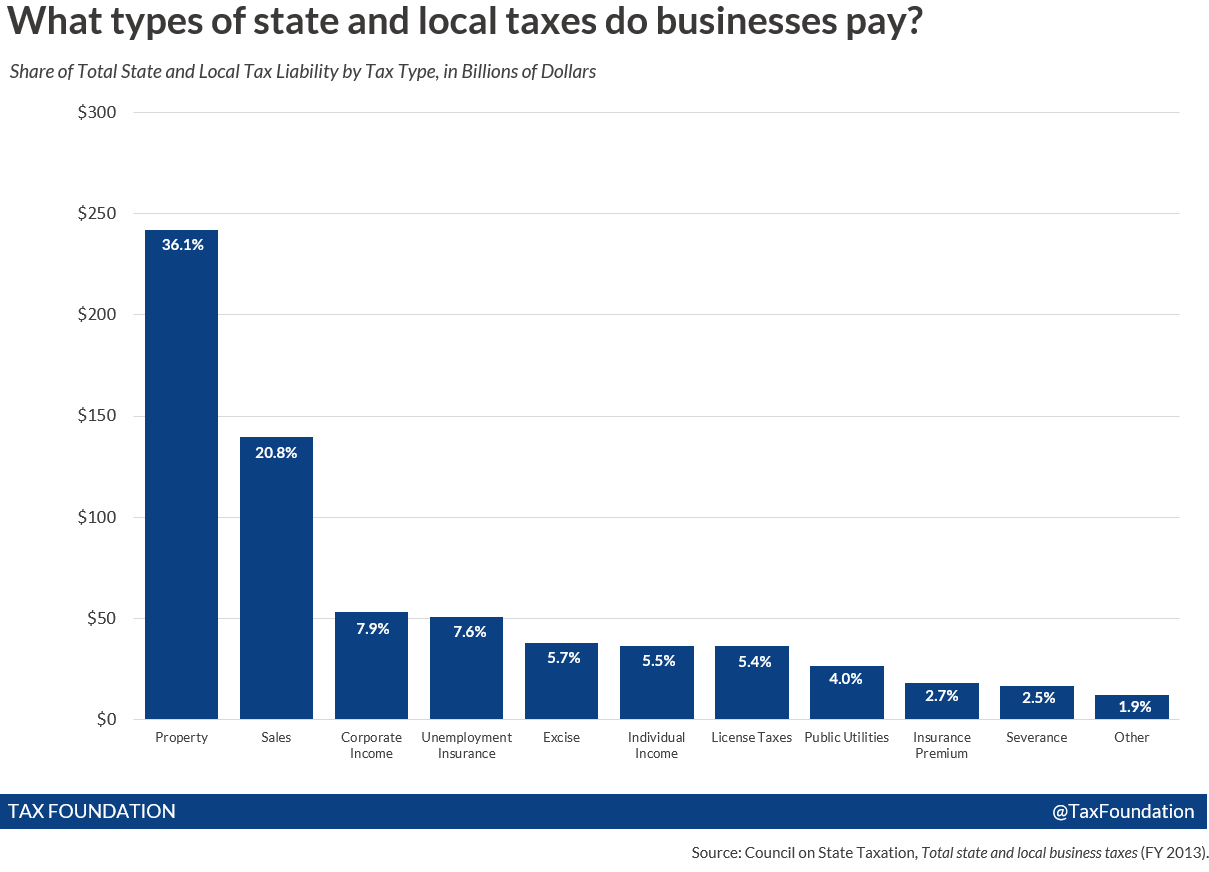

Each year, the Council on State Taxation (COST) estimates the share of total state and local taxes that are paid by businesses. The lastest edition of the report found that firms paid 44.9 percent of total U.S. state and local taxes last year—amounting to nearly $671 billion.

Here’s the breakdown by taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. type (click to enlarge and share):

Of the $670.8 billion in total business taxes, most went to property taxes on business property ($242.1 billion), followed by sales taxes on business inputs ($139.8 billion). In a perfect world, businesses wouldn't pay sales taxes. My colleague, Scott Drenkard, summed this up eloquently a few years ago:

Business inputs (products that businesses buy so that they can make other things) should be exempt from sales taxes. This is not because businesses deserve special treatment, but because taxing business inputs results in “tax pyramiding,” the problem where one tax applied many times on a supply chain results in a high effective tax rate at the end of the supply chain. Taxation of business inputs results in the unequal (or non-neutral) treatment of industries or companies that have many capital inputs…

It's also important to note that corporate income taxes, though they are the most familiar business tax, are only a small share of the total tax bill firms pay each year. But don't confuse this fact for an argument to increase corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rates–corporate income taxes are an inefficient tool for collecting state tax revenue due to their low growth and high volatility.

For more information on the types of business taxes outlined in the report, the changes from 2012 to 2013, and a state-by-state breakdown, check out COST's full report here.

Follow Liz on Twitter @elizabeth_malm.

Share this article