In November 2000, Arizona voters approved Proposition 301, increasing the sales tax rate from 5 to 5.6 percent to help fund public education. Advocates in the state are seeking to both extend and expand the rate, but lawmakers should instead address the state’s dwindling tax base.

Governor Ducey (R) has indicated his willingness to support a ballot initiative to extend the rate, which expires in 2021. Arizona Superintendent Diane Douglas and business leaders want to go further and increase the sales tax rate.

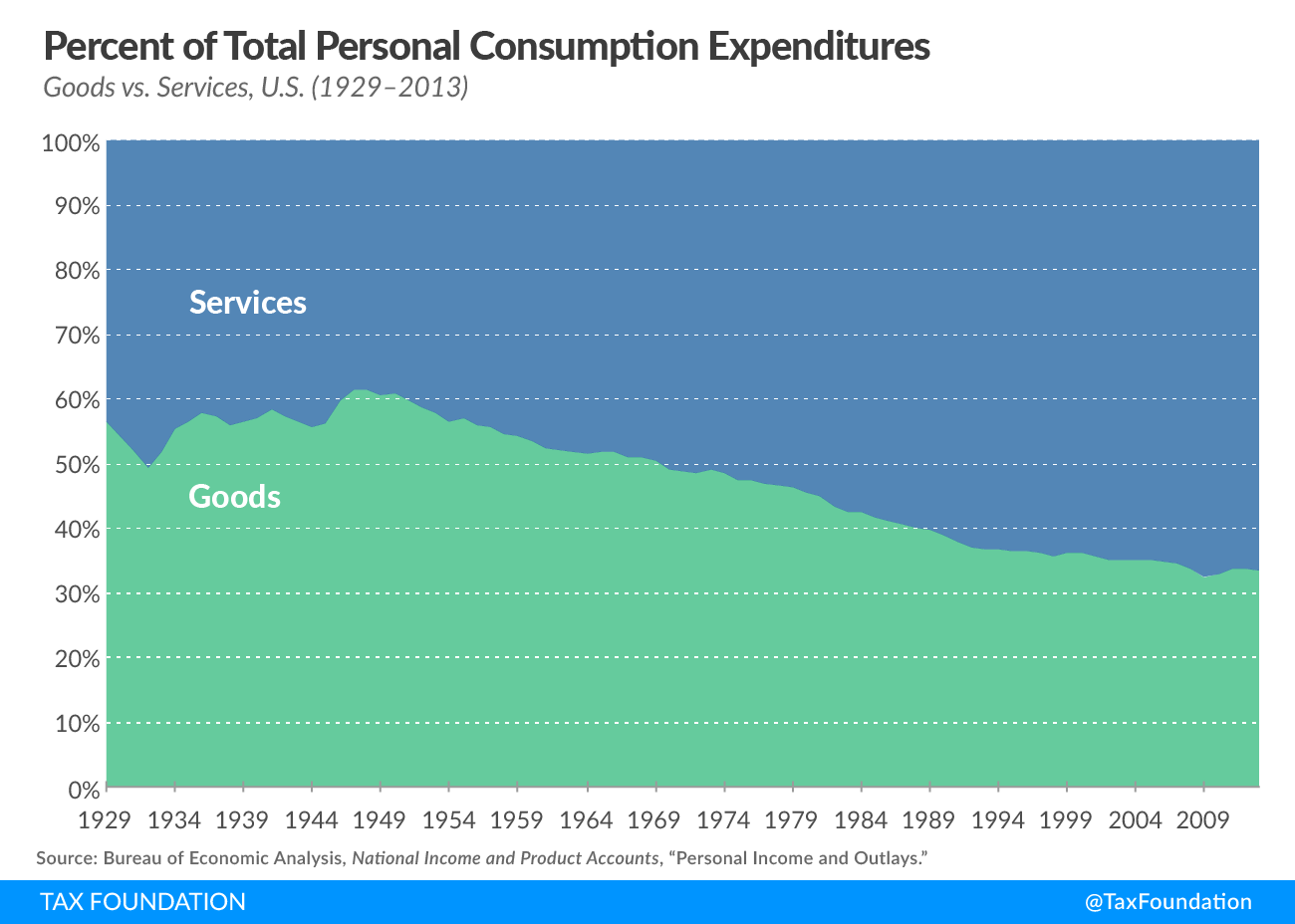

However, these calls for a higher sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. rate increase are indicative of a larger, structural problem in Arizona’s taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. code. As the chart below shows, services are accounting for a growing portion of economic activity, but are typically not subject to the sales tax which has led to a narrow sales tax. States have generally shied away from expanding their tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. to include services. As a result, the sales tax base has narrowed in many states. As the tax base narrows, the rate must increase to generate the same amount of revenue. Due to exemptions for particular goods and most services, the sales tax only applies to 41 percent of Arizona’s economy.

Another rate hike is only a short-term solution to Arizona’s revenue concerns. The long-term solution is to expand the tax base by including all final consumer goods and services. By broadening the sales tax base instead of raising the rate, Arizona can improve its tax code and stabilize its revenue stream to fund policy priorities.

Share this article