Tracking the Impact of the Trump Tariffs & Trade War

The Trump tariffs have not meaningfully altered the trade balance and amount to an average tax increase per US household of $700 in 2026.

55 min readThe Tax Foundation is the world’s leading independent tax policy 501(c)(3) nonprofit. For over 85 years, our mission has remained the same: to improve lives through tax policies that lead to greater economic growth and opportunity.

Our Center for Federal Tax Policy, Center for State Tax Policy, and Center for Global Tax Policy each produce timely and high-quality research and analysis that influences the debate toward economically principled tax policies. Our experts are continuously analyzing the day’s most relevant tax policy topics and are relied upon routinely for presentations, testimony, and media appearances on tax issues spanning every level of government.

Likewise, providing journalists, taxpayers, and policymakers with basic data on taxes and spending has been a cornerstone of the Tax Foundation’s educational mission since its founding. As we wrote in our first edition of Facts & Figures in 1941, “Facts give a broader perspective; facts dissipate predilections and prejudices…[and are] an important step to meet the challenge presented by the broad problems of public finance.”

The Trump tariffs have not meaningfully altered the trade balance and amount to an average tax increase per US household of $700 in 2026.

55 min read

How will recent federal tax changes affect you?

4 min read

The State Tax Competitiveness Index enables policymakers, taxpayers, and business leaders to gauge how their states’ tax systems compare. While there are many ways to show how much state governments collect in taxes, the Index evaluates how well states structure their tax systems and provides a road map for improvement.

122 min read

Lawmakers can constrain the growth of property taxes without creating new problems. But the details matter.

Our experts explain how this major tax legislation may affect you and how policymakers can better improve the tax code.

24 min read

For Congress, work on the One Big Beautiful Bill Act is done. But in state capitols, the work has not yet begun. Many of the tax changes in the federal reconciliation act flow through to state tax codes—automatically in some states, and subject to an update in states’ Internal Revenue Code conformity date in others.

39 min read

As a rule, an individual’s income can be taxed both by the state in which the taxpayer resides and by the state in which the taxpayer’s income is earned.

52 min read

Notably, the OBBBA makes permanent the individual tax changes first put in place by the TCJA, which avoids a tax hike on an estimated 62 percent of tax filers in 2026.

4 min read

Facts & Figures serves as a one-stop state tax data resource that compares all 50 states on over 40 measures of tax rates, collections, burdens, and more.

2 min read

While there are many factors that affect a country’s economic performance, taxes play an important role. A well-structured tax code is easy for taxpayers to comply with and can promote economic development while raising sufficient revenue for a government’s priorities.

93 min read

New IRS data shows the US federal income tax system continues to be progressive as high-income taxpayers pay the highest average income tax rates. Average tax rates for all income groups remain lower after the Tax Cuts and Jobs Act (TCJA).

6 min read

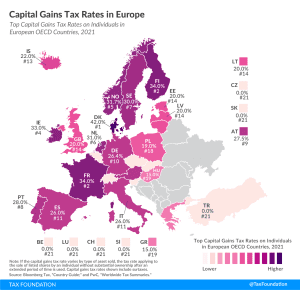

The variety of approaches to taxation among European countries creates a need to evaluate these systems relative to each other. For that purpose, we have developed the European Tax Policy Scorecard—a relative comparison of European countries’ tax systems.

55 min read

Taxes on goods and services were on average the greatest source of tax revenue for Latin American and Caribbean countries

5 min read

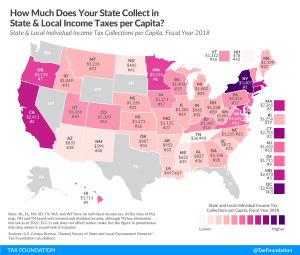

The individual income tax is one of the most significant sources of revenue for state and local governments, generating approximately 24 percent of state and local tax collections in FY 2018.

2 min read

The Biden administration has argued for raising the corporate tax rate to offset the drop in federal corporate revenues following the Tax Cuts and Jobs Act (TCJA) of 2017, claiming it did not lead to more corporate investment as advertised. Although corporate revenues did drop following this tax reform, the ensuing increase in corporate investment far exceeds these revenue losses.

1 min read

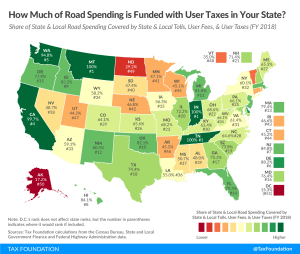

Traditionally, revenue dedicated to infrastructure spending has been raised through taxes on motor fuel, license fees, and tolls, but revenue from motor fuel has proven less effective over the last few decades.

6 min read

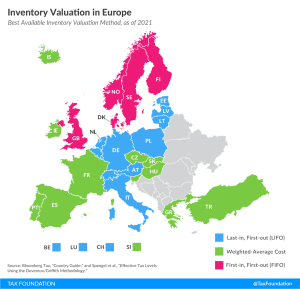

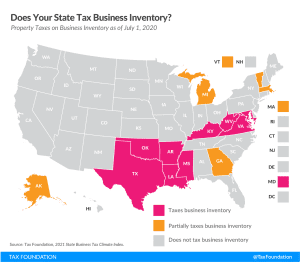

The method by which a country allows businesses to account for inventories can significantly impact a business’s taxable income. When prices are rising, as is usually the case due to factors like inflation, LIFO is the preferred method because it allows inventory costs to be closer to true costs at the time of sale.

2 min read

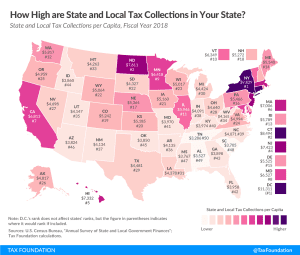

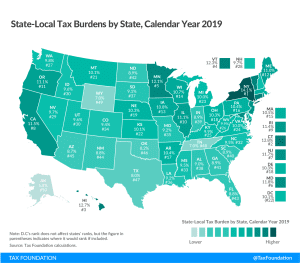

Although Tax Day has been pushed back this year, mid-April is still a good occasion to take a look at tax collections in the United States. Because differing state populations can make overall comparisons difficult, today’s state tax map shows state and local tax collections per capita in each of the 50 states and the District of Columbia.

3 min read

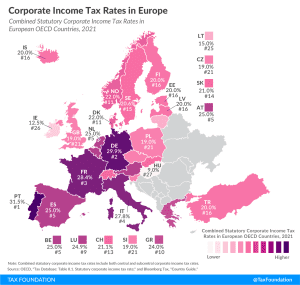

On average, European OECD countries currently levy a corporate income tax rate of 21.7 percent. This is below the worldwide average which, measured across 177 jurisdictions, was 23.9 percent in 2020.

2 min read

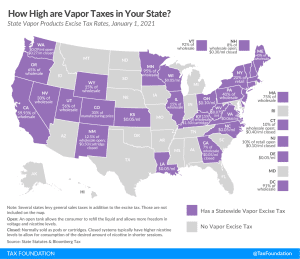

Several states are considering introducing or increasing taxes on vapor products to make up declining tax revenue from traditional tobacco products or to fill budget holes in the wake of the coronavirus pandemic. However, lawmakers should approach the issue carefully because flawed excise tax design on vapor products could drive consumers back to more harmful combustible products like cigarettes.

3 min read

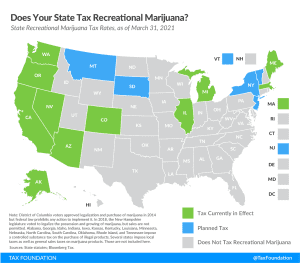

The legalization and taxation of recreational marijuana remains one of the hottest trends in state taxation.

6 min read

The ongoing pandemic has once again highlighted the importance of investment. To address the economic fallout of the pandemic, several OECD countries have temporarily accelerated depreciation schedules for various assets.

31 min read

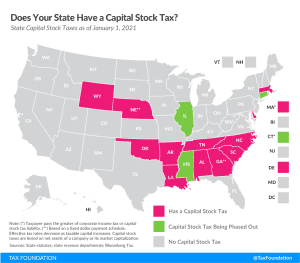

Capital stock taxes are imposed on a business’s net worth (or accumulated wealth). As such, the tax tends to penalize investment and requires businesses to pay regardless of whether they make a profit in a given year, or ever.

4 min read

New Yorkers faced the highest burden, with 14.1 percent of income in the state going to state and local taxes. Connecticut (12.8 percent) and Hawaii (12.7 percent) followed.

19 min read

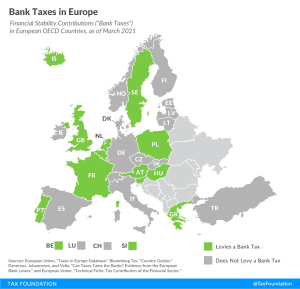

Today’s map shows which European OECD countries implemented financial stability contributions (FSCs), commonly referred to as “bank taxes.”

2 min read

Inventory taxes are levied regardless of whether a business makes a profit, adding to the burden of businesses already struggling to stay afloat.

3 min read

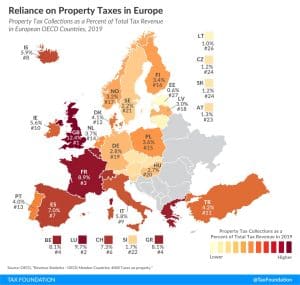

Property taxes are levied on the assets of an individual or business. There are different types of property taxes, with recurrent taxes on immovable property (such as property taxes on land and buildings) the only ones levied by all countries covered. Other types of property taxes include estate, inheritance, and gift taxes, net wealth taxes, and taxes on financial and capital transactions.

1 min read

Moving away from state gross receipts taxes would represent a pro-growth change to make the tax code friendlier to businesses and consumers alike, which is especially necessary in the wake of the coronavirus pandemic.

3 min read

Our updated 2021 edition of Facts & Figures serves as a one-stop state tax data resource that compares all 50 states on over 40 measures of tax rates, collections, burdens, and more.

1 min read

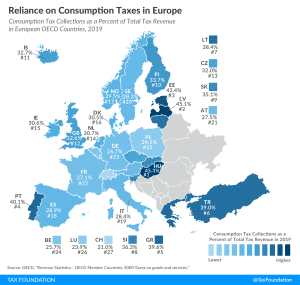

Hungary relies the most on consumption tax revenue, at 45.3 percent of total tax revenue, followed by Latvia and Estonia at 45.1 percent and 42.4 percent, respectively.

2 min read