Dr. Huaqun Li is Senior Economist, Director of Modeling Projects at the Tax Foundation. She focuses on developing and maintaining the Foundation’s Taxes and Growth Model, which models the budgetary and economic effects of changes to federal tax policy.

Huaqun also uses the Taxes and Growth Model to model individual and corporate tax policy proposals and reform plans and helps with publishing the results. Before joining the Tax Foundation, she was a research economist at Regional Economics Models, Inc. at Amherst, MA, where she worked on model building, empirical analysis, and new product development on economic and demographic forecast models.

Dr. Huaqun Li received her PhD in Public Policy Analysis from George Mason University. Her primary research areas include regional economic development, regional inequality, entrepreneurship and new firms, as well as regional development in China.

Huaqun lives in Fairfax, Virginia. In her free time, she enjoys cooking, hiking, and doing yoga.

Learn more about the House Build Back Better Act, including the latest details and analysis of the Biden tax increases and reconciliation bill tax proposals.

Over the next ten years, the structure of the Child Tax Credit (CTC) is scheduled to change, complicating efforts to extend enhanced CTC benefits or reform the CTC for the long-term. Rather than take an all-or-nothing approach or kick the can down the road by relying on temporary expansions, lawmakers could consider alternative options that better target low-income households, retain work incentives, reduce the impact on federal revenue, and provide taxpayers with a stable, consistent tax code.

While Congress continues to debate how to pay for President Biden’s spending proposals in the fiscal year 2022 budget, it is useful to consider the economic impact of a range of financing options in addition to the President’s proposed tax increases.

While it is good that policymakers are taking the impact of the economy on tax revenue seriously, it is important to remember that the dynamic effect of increased spending would only offset a small portion of the total spending. In other words, new spending—like tax cuts—rarely pays for itself.

The redistribution of income from the Biden administration’s tax proposals would involve many winners and losers, not only across different types of taxpayers but also geographically across the country. Launch our new interactive map to see average tax changes by state and congressional district over the budget window from 2022 to 2031.

Explore President Biden budget proposals, including tax and spending in American Jobs Plan and American Families Plan. See Biden tax and spending proposals.

The Biden administration’s American Jobs Plan proposal to fund infrastructure spending relies on a bet that the benefits outweigh the costs of a higher corporate tax burden. Using the Tax Foundation model, we find that this trade-off is a bad one for the U.S. economy, resulting in reduced GDP, less capital investment, fewer jobs, and lower wages.

The Biden administration’s proposed American Families Plan includes several major tax changes. Explore the tax proposals in the American Families Plan.

As the Biden administration and Congress consider making the expanded child tax credit permanent, a nearly $1.6 trillion expansion of tax code-administered benefits, they should consider financing it in a way that doesn’t create significant headwinds to economic recovery.

The House Ways and Means Committee measures would further extend the relief measures created by the CARES Act and the Consolidated Appropriations Act of 2021, and would go further by significantly expanding existing tax credits and making changes to the international tax system.

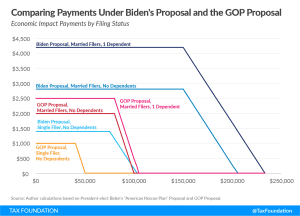

President Biden is calling for a third round of economic impact payments to households as part of his $1.9 trillion American Rescue Plan. Under the plan, the payments would be $1,400 per person, topping off the recent round of $600 payments for a combined $2,000 per person. Senate Republicans have proposed payment amounts of $1,000 per individual and $500 per dependent, lower income thresholds, and faster phaseout rates.

President Biden’s plan builds on previous relief packages and would include larger payments to individuals, expanded relief for households and small businesses, funding for vaccine distribution, and aid to state and local governments.

What has President Joe Biden proposed in terms of tax policy changes? Our experts provide the details and analyze the potential economic, revenue, and distributional impacts.

On Thursday, U.S. Senators Marco Rubio (R-FL), Bill Cassidy (R-LA), Steve Daines (R-MT), and Mitt Romney (R-UT) released the Coronavirus Assistance for American Families Act (CAAF), which would provide payments of $1,000 to adults and children with Social Security numbers, subject to income limits used in the original round of rebates. Among other modifications, it would be more generous to households and families with children when compared to the original rebates distributed under the CARES Act.

Our analysis shows that the economic benefits of federal investment in productivity-enhancing infrastructure may be undercut by the negative effects of the financing of those investments, such as when the corporate income tax is increased.

Permanent full expensing for all types of investment is an effective policy change lawmakers can use to encourage additional investment and economic growth.

As Congress and the White House consider ways to shore up the economy in the face of a public health crisis, President Trump has suggested suspending the entire payroll tax for the duration of the year. That would cost about $950 billion, according to our analysis.

The CARES Act, now signed into law, is intended to be a third round of federal government support in the wake of the coronavirus public health crisis and associated economic fallout, following the $8.3 billion in public health support passed two weeks ago and the Families First Coronavirus Response Act.

The proposed Take Responsibility for Workers and Families Act can be contrasted with the Senate Republican CARES Act, although they share some similarities by providing individual taxpayers with a rebate and modifying business tax provisions to provide liquidity for struggling firms.