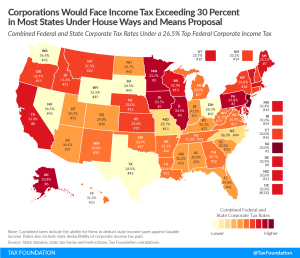

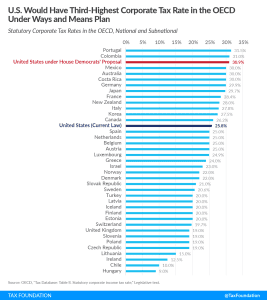

U.S. Would Have Third-Highest Corporate Tax Rate in OECD Under Ways and Means Plan

Under the Ways and Means text, the U.S. would have an average corporate tax rate of 30.9 percent, which would be the third-highest corporate tax rate in the OECD, behind only Colombia and Portugal.

1 min read