VAT Rates in Europe, 2019

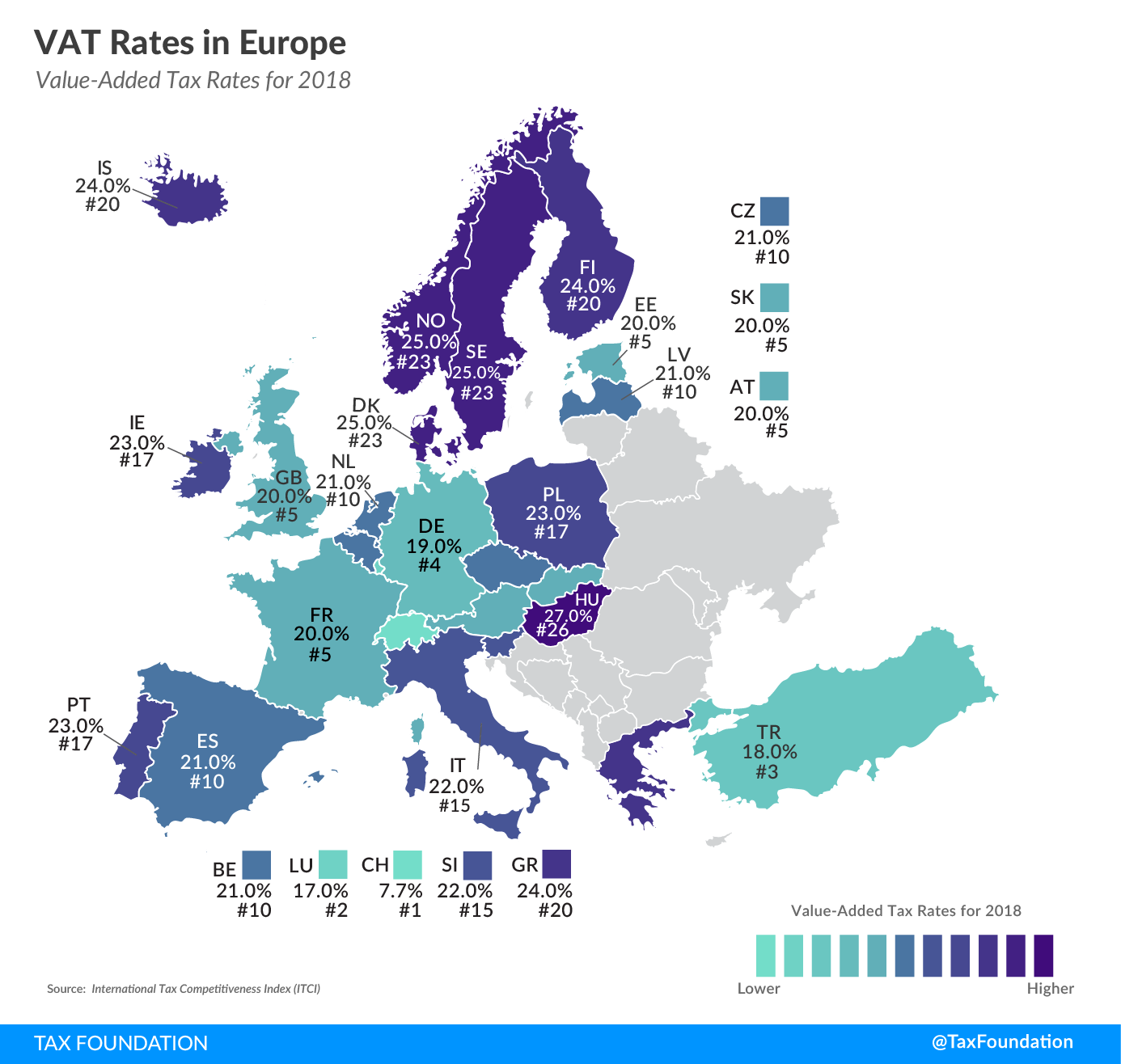

4 min readBy:More than 140 countries worldwide – including all European countries – levy a Value-Added Tax (VAT) on purchases for consumption. As today’s tax map shows, although harmonized to some extent by the European Union (EU), Europe’s VAT rates vary moderately across countries.

The VAT is a consumption tax assessed on the value added to goods and services. The final VAT levied on a good or service is the sum of the VAT paid at each production stage. While VAT-registered businesses can deduct all the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. already paid in the preceding production stages, the end consumer does not receive a credit for the VAT paid, making it a tax on final consumption.

The potential for easy administration, significant tax revenue, and few economic distortions make the VAT one of the most efficient forms of taxation. In contrast, some other forms of taxation, such as income and corporate taxes, impede economic activity and can distort decisions between consumption and investment.

According to EU law, EU Member States are required to levy a standard VAT rate of at least 15 percent and a reduced rate of at least 5 percent. Switzerland, as a non-EU country, levies the lowest VAT rate of only 7.7 percent, followed by Luxembourg (17 percent), Turkey (18 percent), and Germany (19 percent). The countries with the highest VAT rates are Hungary (27 percent), and Sweden, Norway, and Denmark (all at 25 percent). The average VAT rate of the European countries covered is 21.3 percent.

Most European countries set thresholds for their VATs. This means that a business’s revenue of taxable goods and services must be above a certain value before it is required to register and pay a VAT on its products. This registration threshold allows small businesses to save time and expenses in compliance. However, it also discriminates against larger businesses, creating economic distortions.

|

Source: OECD (http://www.oecd.org/tax/tax-policy/tax-database.htm#VATTables) Registration thresholds identified in this table are general concessions that relieve domestic suppliers from the requirement to register for and/or to collect VAT until such time as they exceed the revenue threshold. Relief from collection and/or registration may be available to specific industries or types of traders (for example nonresident suppliers) under more detailed rules, or a specific industry or type of trader may be subject to more stringent registration and collection requirements. The thresholds of non-euro countries have been converted into euros for comparability by using the European Central Bank’s (ECB) 2018 exchange rates. |

||

| Country | Standard VAT Rate | Registration Threshold (a) |

|---|---|---|

| Austria | 20.0% | € 30,000 |

| Belgium | 21.0% | € 25,000 |

| Czech Republic | 21.0% | € 38,991 |

| Denmark | 25.0% | € 6,709 |

| Estonia | 20.0% | € 40,000 |

| Finland | 24.0% | € 10,000 |

| France | 20.0% | € 82,200 |

| Germany | 19.0% | € 17,500 |

| Greece | 24.0% | € 10,000 |

| Hungary | 27.0% | € 25,087 |

| Iceland | 24.0% | € 7,819 |

| Ireland | 23.0% | € 75,000 |

| Italy | 22.0% | € 30,000 |

| Latvia | 21.0% | € 40,000 |

| Luxembourg | 17.0% | € 30,000 |

| Netherlands | 21.0% | € 1,345 |

| Norway | 25.0% | € 5,210 |

| Poland | 23.0% | € 46,932 |

| Portugal | 23.0% | € 10,000 |

| Slovak Republic | 20.0% | € 49,790 |

| Slovenia | 22.0% | € 50,000 |

| Spain | 21.0% | € 0 |

| Sweden | 25.0% | € 2,924 |

| Switzerland | 7.7% | € 86,580 |

| Turkey | 18.0% | € 0 |

| United Kingdom | 20.0% | € 96,077 |

In Spain and Turkey, all businesses, regardless of their revenue, are required to register and pay a VAT. On the other hand, French and Swiss businesses are only exempt from VAT registration if their revenues stay below considerably high thresholds of € 82,200 and € 86,580, respectively.

Apart from VAT rates and thresholds, the VAT base also significantly impacts the effectiveness and efficiency of a VAT. A future map will show how European countries rank on a measure of their VAT base.

International Tax Competitiveness Index

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAbout the Author

Elke Asen

Policy Analyst

Elke Asen was a Policy Analyst with the Tax Foundation’s Center for Global Tax Policy, focusing on international tax issues and tax policy in Europe. Prior to joining the Tax Foundation, Elke interned with the EU Delegation in Washington, D.C., the German Development Agency, and a social startup in Munich, Germany. She holds a BS in Economics from Ludwig Maximilian University of Munich.