As part of the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. proposals in President Biden’s American Families Plan (AFP), unrealized capital gains over $1 million would be taxed at death. However, this policy would likely raise less revenue than advocates expect after considering the proposal’s impact on taxpayer behavior, including capital gains realizations, and historical capital gains and estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs. revenue collections.

In addition to taxing unrealized gains at death, the AFP would raise the top marginal capital gains taxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment. rate for taxpayers earning over $1 million to 43.4 percent when including the 3.8 percent net investment income tax (NIIT), considerably higher than the current top capital gains tax rate of 23.8 percent. We estimate that taxing unrealized capital gains at death with a $1 million exemption and increasing the tax rate on capital gains (and qualified dividends) would raise about $213 billion over 10 years, lower than other estimates of around $400 billion over that time period.

The AFP proposed raising the top capital gains rate and taxing unrealized gains at death together, because raising the capital gains rate to 43.4 percent alone would lose federal revenue. Realizations would fall so much that it would more than offset the revenue produced by the higher tax rate. Without taxing unrealized gains at death, the revenue-maximizing capital gains tax rate is about 30 percent in the long run and about 20 percent in the short run.

Taxing unrealized capital gains at death theoretically increases the revenue-maximizing capital gains tax rate because taxpayers are less likely to hold onto assets until death to avoid the higher rate. Our estimate assumes that realizations are 20 percent less responsive to a change in the capital gains tax rate when unrealized gains are taxed at death, resulting in a long-run revenue-maximizing rate of about 38 percent.

However, there is in fact a great deal of uncertainty about how much realizations would change when taxing unrealized gains at death. First, the policy has never been tried in the United States. Second, partly because of the novelty of the policy, taxpayers may expect it to not be durable, and will hold onto assets with unrealized gains expecting that the policy will be reversed. Third, there may be opportunities for tax planning to reduce or avoid taxation of gains at death, including some techniques that have been developed in response to the estate tax (e.g., gifting), some newer methods (e.g., opportunity zones), and some not yet created.

Fourth, an increase in capital gains taxes tends to put downward pressure on the value of assets like equities, leading to smaller unrealized gains taxable at death than prior to the tax increase. Finally, the AFP would provide protections for businesses and farms without the liquidity to pay tax on unrealized gains all at once. For example, the STEP Act proposed by Sen. Chris Van Hollen (D-MD) and colleagues, which proposes a similar tax on unrealized gains at death, would provide a 15-year window for payment of the tax on unrealized gains. Building in exemptions or extended timelines for tax payment would reduce the revenue collected over the 10-year budget window, in part by creating new opportunities for tax planning.

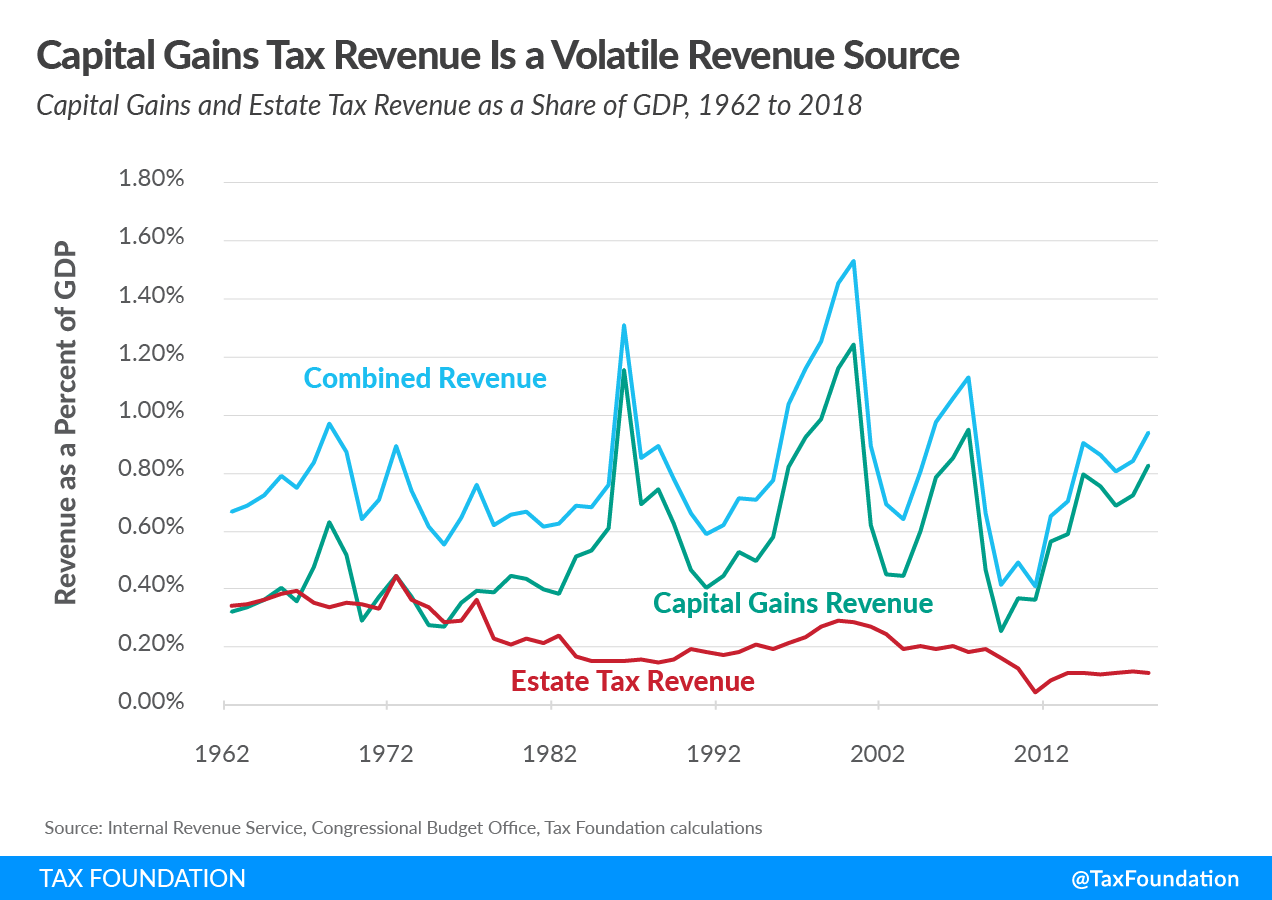

Another way to evaluate the proposal’s revenue potential is to look at historical revenue collected from the estate tax and capital gains taxes. Examining estate tax revenue can be useful because the proposed taxation of unrealized gains at death is very similar to the estate tax, but with a lower exemption (the estate tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. is $11.7 million for single filers) and applicable only to assets with unrealized gains.

Estate tax revenue has fallen from about 0.3 percent of GDP in the 1960s to about 0.1 percent in 2018, partly due to an increasing exemption. The estate tax exemption was at or less than $1 million in real terms prior to 2003.

Capital gains taxes have been a volatile source of revenue, as it is sensitive to economic conditions and changes in realizations in expectation of and reacting to changes in tax rates. Between 1987 and 1997, when the top tax rate for capital gains was 28 or 29 percent, capital gains revenue averaged about 0.6 percent of GDP, lower than the 0.8 percent collected today.

Raising the top statutory rate on capital gains often has not led to more revenue as a share of the economy. Between 1970 and 1978, when top statutory capital gains rates exceeded 30 percent—topping out at 39.875 percent from 1976 to 1978—revenue averaged about 0.35 percent of GDP.

Combined revenue for capital gains and the estate tax has averaged about 0.8 percent of GDP since 1990, bottoming out at about 0.4 percent in 2011 and rising to about 0.9 percent in 2018. We estimate that the AFP would raise capital gains revenue by about 0.1 percent of GDP by 2031, which may bring combined collections with the estate tax to about 1 percent of GDP. If the tax change were to raise $400 billion as some advocates argue, this would raise total collections by nearly 0.2 percent of GDP.

The U.S. has not typically seen sustained collections of capital gains and estates taxes above 1 percent of GDP; the longest stretch of time when collections exceeded that level was between 1996 to 2000 during the dot-com boom. It is unlikely this tax change would break that trend, especially given the uncertainty about the long-term prospects of the policy locking gains in place.

As Congress considers proposals to increase the tax burden on capital gains, we should be skeptical of arguments that taxing unrealized gains at death and raising the top tax rate will be a large revenue raiser.

Launch Resource Center: President Biden’s Tax Proposals

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe