The breakdown of supply chains both domestically and worldwide currently dominates headlines. One strong explanation of supply chain failures is the dramatic increase in federal spending throughout the pandemic—raising aggregate demand—combined with the COVID 19-era shift of consumption from services to physical goods. That, coupled with preexisting issues that limit the ability of our ports and other parts of the country’s logistical backbone to increase capacity, explains most of the wait times and shortages happening today.

While tax policy is neither a direct cause of nor immediate solution to today’s supply chain woes, fixing how the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. code treats inventories and other capital investments could make supply chains more resilient going forward.

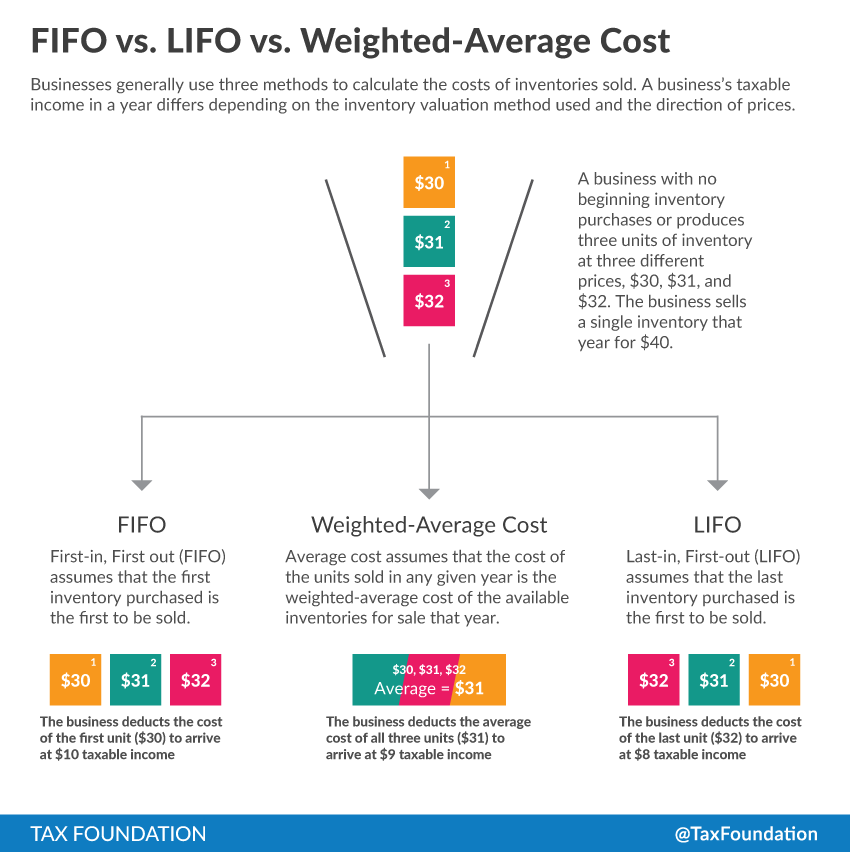

Under the current tax code, companies do not get to deduct the cost of inventories when they are purchased; instead, they wait until inventories are sold. The tax code provides three methods for determining the amount that can be deducted when a unit of inventory sells. First-in, First-out (FIFO) allows companies to deduct the amount paid for the oldest unit of that kind of inventory in stock. Last-in, First-out (LIFO) allows companies to deduct the amount paid for the most recently purchased piece of inventory. And the weighted-average cost method allows firms to deduct the average cost of all inventory units.

Ultimately, to treat inventory costs neutrally, firms should be allowed to deduct costs when inventory is purchased instead of waiting until it sells. No methods currently allow that, but LIFO gets closer than the others. Because prices tend to rise over time, having companies deduct the amount paid for the oldest units in their inventory usually means they are deducting much less than the price of a replacement inventory unit. Allowing firms to deduct the most recently-purchased unit, as LIFO does, comes closer to matching the cost of the replacement unit.

The impact of stopping short of a full, immediate deduction is a tax bias against inventory spending—in other words, this tax treatment raises the marginal cost of purchasing more inventory to keep in stock. As Kyle Pomerleau of the American Enterprise Institute noted in a paper last year, the marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. on business investment in inventory is 30 percent—higher than investments in intellectual property, equipment, structures, and land. And as my colleague Erica York wrote earlier this year, moving to a system that allows inventory to be deducted when purchased could fix a tax system that encourages just-in-time manufacturing.

There are some other tax issues that could improve the resiliency of supply chains. One major story of the supply chain crisis is how the Port of Los Angeles and the Port of Virginia have responded. The Port of Los Angeles has suffered from enormous delays, with 100 cargo ships stuck in a holding pattern in the harbor this October (as opposed to only 17 under typical circumstances). And a recent report named the Port of Los Angeles one of the least efficient in the world.

Meanwhile, the Port of Virginia’s operations have continued largely uninterrupted. One main explanation for the difference is the Port of Virginia is more heavily automated, which requires capital investment in newer machinery and equipment. Allowing companies to fully deduct capital investment puts capital costs on the same footing as salary expenses and makes capacity-enhancing investments more likely. Productivity-growing investments also help raise wages for workers.

While taxes are not at the root of supply chain disruptions, improvements to the tax code could make supply chains more resilient in the future.

Share this article