All Related Articles

9232 Results

Reliance on Consumption Taxes in Europe

2 min read

Comparison of Cross-Border Effective Average Tax Rates in Europe and G7 Countries

As policymakers consider ways to facilitate investment, effective average tax rates provide a valuable perspective on where burdens on those activities are high and where they are low.

16 min read

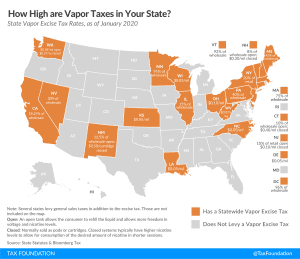

Excise Taxes on Vapor Products Are Trending

While lawmakers are working through the design of vapor tax proposals, they must thread the needle between protecting adult smokers’ ability to switch and barring minors’ access to nicotine products. A good first step is creating appropriate definitions for the new nicotine products to avoid unintended disproportionate taxation based on design differences or bundling.

7 min read

Analysis of Democratic Presidential Candidate Individual Income Tax Proposals

Joe Biden and Bernie Sanders have each proposed changes to the individual income tax, one of the largest sources of federal revenue. Our new analysis compares the economic, revenue, and distributional effects of the various proposals.

13 min read