Tax Subsidies for R&D Expenditures in Europe

3 min readBy:Many countries incentivize business investment in research and development (R&D), intending to foster innovation. A common approach is to provide direct government funding for R&D activity. However, a significant number of jurisdictions also offers R&D tax incentives.

These generally take two forms, namely patent boxA patent box—also referred to as intellectual property (IP) regime—taxes business income earned from IP at a rate below the statutory corporate income tax rate, aiming to encourage local research and development. Many patent boxes around the world have undergone substantial reforms due to profit shifting concerns. es—taxing income derived from intellectual property at a rate below the statutory corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate—and taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. incentives for R&D expenditures. Today’s map will focus on the latter, showing to what degree European OECD countries grant expenditure-based R&D tax relief.

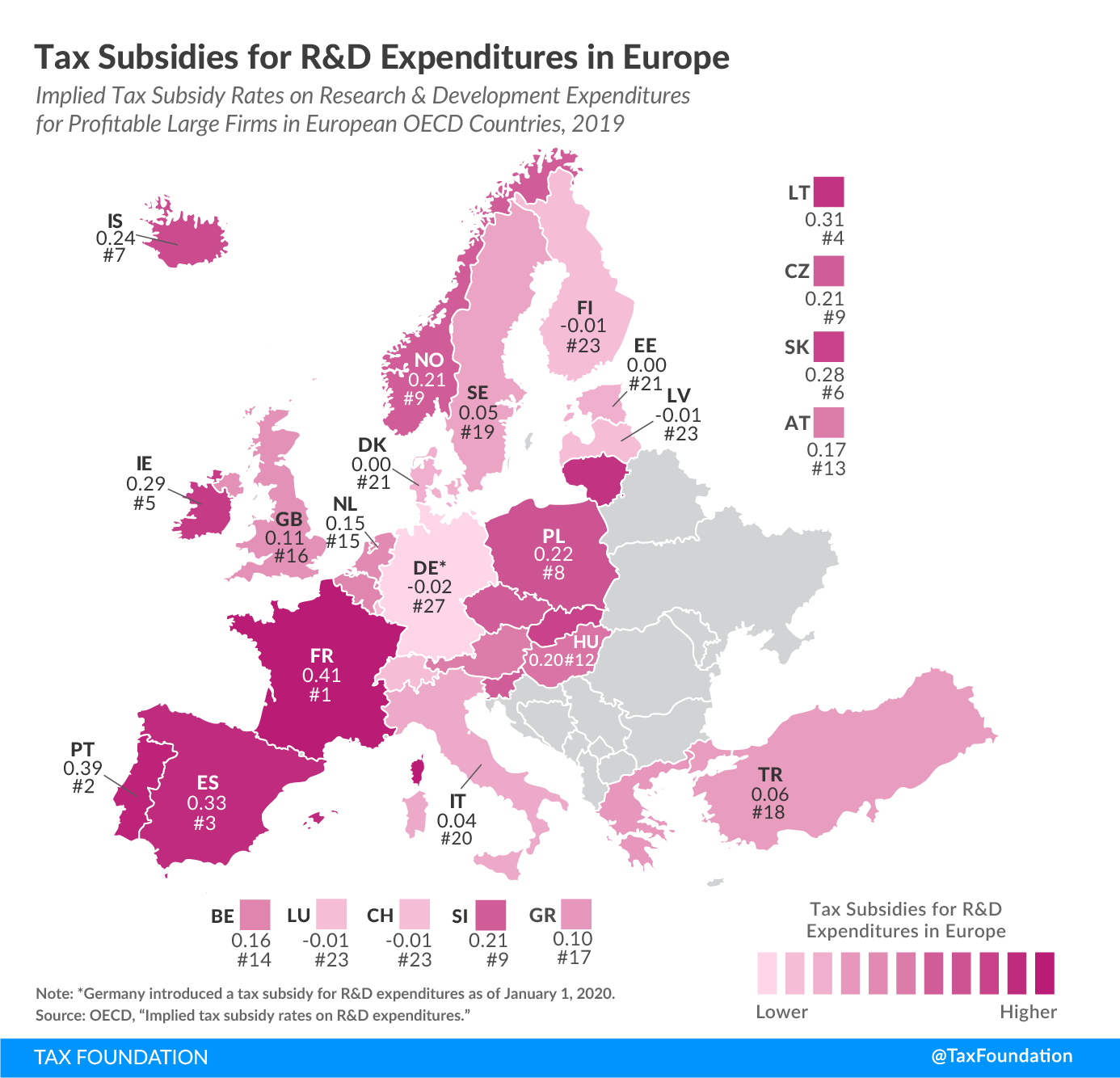

The implied tax subsidy rate, developed by the OECD, is one way to measure the extent of expenditure-based R&D tax relief across countries. Tax subsidy rates are measured as the difference between one unit of investment in R&D and the pretax income required to break even on that investment unit, assuming a representative firm. In other words, it measures the extent of the preferential treatment of R&D in a given tax system. The more generous the tax provisions for R&D, the higher the implied subsidy rates for R&D. An implied subsidy rate of zero means R&D does not receive preferential tax treatment.

The implied tax subsidy rates for large profitable firms vary significantly among countries that grant notable relief, ranging from 0.04 in Italy to 0.41 in France. Portugal and Spain provide the second and third most generous relief after France, with implied tax subsidy rates of 0.39 and 0.33, respectively.

Of the countries that grant notable relief, Italy (0.04), Sweden (0.05), and Turkey (0.06) are the least generous. The implied tax subsidy rates of Denmark, Estonia, Finland, Latvia, Luxembourg, and Switzerland do not show any significant expenditure-based R&D tax relief. Germany introduced an R&D tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly. in 2020 (not reflected in data).

The OECD also provides implied tax subsidy rates for loss-making firms and for small and medium-sized enterprises (SMEs). Most countries covered in today’s map provide the same expenditure-based R&D tax relief to large firms and SMEs. Only France (in the case of loss-making firms), the Netherlands, Norway, and the United Kingdom are relatively more generous to SMEs than to large firms.

Some countries’ R&D tax incentives include refunds and carryover provisions, changing the implied tax subsidy rates for loss-making firms relative to profitable firms. This has resulted in lower average implied tax subsidy rates for loss-making firms relative to profitable firms, both for SMEs and large firms.

|

Note: Germany introduced an R&D tax credit in 2020. Source: OECD, “Implied tax subsidy rates on R&D expenditures,” Dec. 16, 2019, https://stats.oecd.org/Index.aspx?DataSetCode=RDSUB. |

||||

| Profitable Firms | Loss-Making Firms | |||

|---|---|---|---|---|

| Country | SME | Large Firm | SME | Large Firm |

| Austria (AT) | 0.17 | 0.17 | 0.17 | 0.17 |

| Belgium (BE) | 0.16 | 0.16 | 0.15 | 0.14 |

| Czech Republic (CZ) | 0.21 | 0.21 | 0.15 | 0.15 |

| Denmark (DK) | 0 | 0 | -0.01 | -0.01 |

| Estonia (EE) | 0 | 0 | 0 | 0 |

| Finland (FI) | -0.01 | -0.01 | 0 | 0 |

| France (FR) | 0.41 | 0.41 | 0.41 | 0.34 |

| Germany (DE)* | -0.02 | -0.02 | -0.02 | -0.02 |

| Greece (GR) | 0.10 | 0.10 | 0.08 | 0.08 |

| Hungary (HU) | 0.20 | 0.20 | 0.18 | 0.19 |

| Iceland (IS) | 0.24 | 0.24 | 0.24 | 0.24 |

| Ireland (IE) | 0.29 | 0.29 | 0.23 | 0.23 |

| Italy (IT) | 0.04 | 0.04 | 0.04 | 0.04 |

| Latvia (LV) | 0 | -0.01 | -0.01 | -0.01 |

| Lithuania (LT) | 0.31 | 0.31 | 0.25 | 0.25 |

| Luxembourg (LU) | -0.01 | -0.01 | -0.01 | -0.01 |

| Netherlands (NL) | 0.31 | 0.15 | 0.30 | 0.15 |

| Norway (NO) | 0.23 | 0.21 | 0.23 | 0.21 |

| Poland (PL) | 0.22 | 0.22 | 0.18 | 0.18 |

| Portugal (PT) | 0.39 | 0.39 | 0.31 | 0.31 |

| Slovak Republic (SK) | 0.28 | 0.28 | 0.22 | 0.22 |

| Slovenia (SI) | 0.21 | 0.21 | 0.17 | 0.17 |

| Spain (ES) | 0.33 | 0.33 | 0.26 | 0.26 |

| Sweden (SE) | 0.05 | 0.05 | 0.05 | 0.05 |

| Switzerland (CH) | -0.01 | -0.01 | -0.01 | -0.01 |

| Turkey (TR) | 0.06 | 0.06 | 0.05 | 0.05 |

| United Kingdom (GB) | 0.27 | 0.11 | 0.27 | 0.11 |

| Average | 0.16 | 0.15 | 0.14 | 0.13 |

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe