The Flavored Tobacco Product Prohibition Amendment Act of 2021 (B24-0020) under consideration by the D.C. City Council would, as the name suggests, ban all flavored tobacco product sales in the District. That means banning the majority of cigarettes being sold, since more than 50 percent of the market is menthol flavored, which could have a significant impact on tobacco excise tax collections. The bill is scheduled for a hearing before the full Council this week.

The bill’s accompanying fiscal impact statement from the District’s Office of the Chief Financial Officer estimates that the revenue impact of the ban will be a roughly $3 million loss in the first year (Fiscal Year 2022) and an additional cumulative decline of $8.6 million over the subsequent three years. Last year, the District collected about $25 million from cigarette taxes. The fiscal statement concludes that revenue from cigarette taxes will decline 13.5 percent, but this estimate seems low considering available data from Massachusetts, which was the first state to ban all flavored tobacco products.

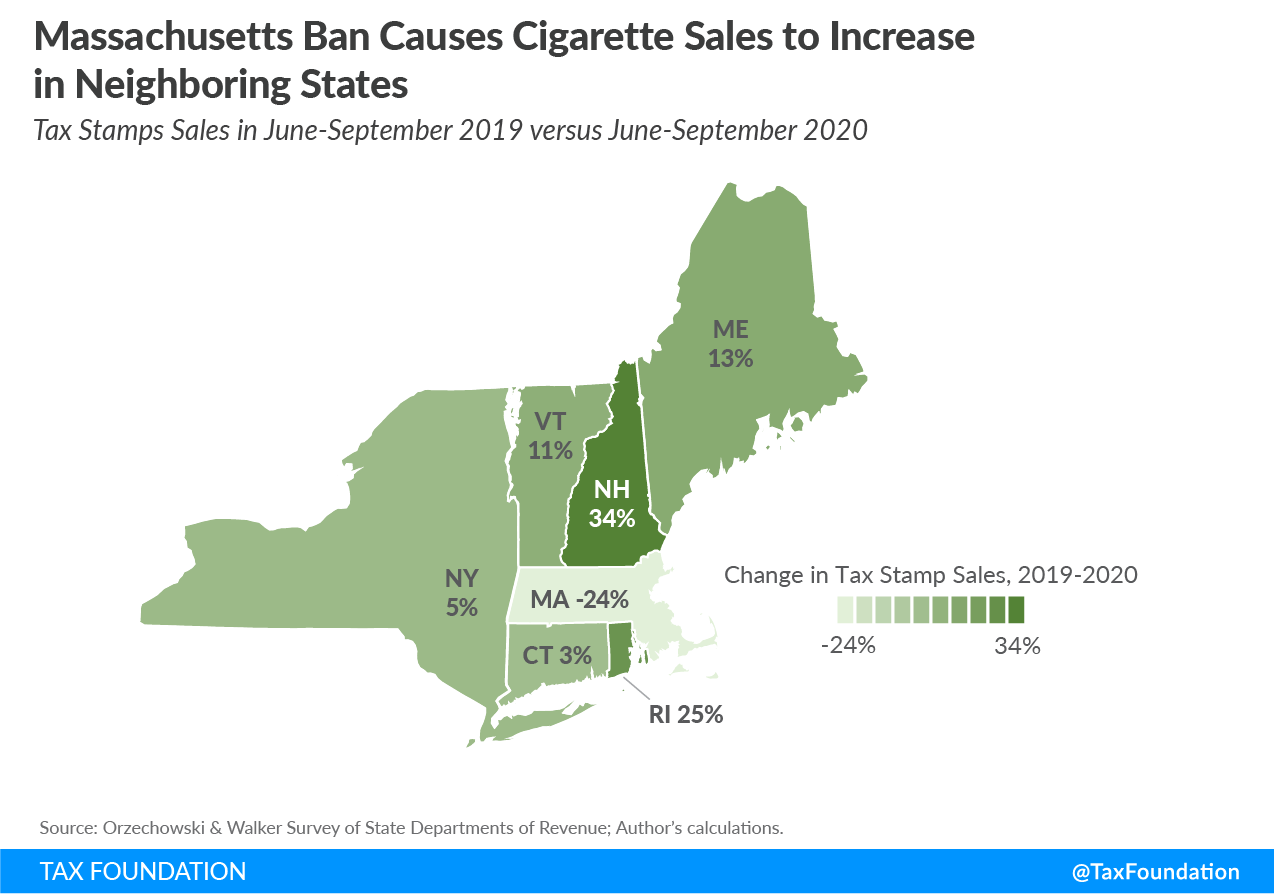

In Massachusetts, the tobacco flavor ban took effect in June 2020, and this fiscal year (July 2020-April 2021 data available), revenue from cigarette taxes is down $120 million—in line with our estimate—compared to the same period of the preceding fiscal year. That reflects a decline of roughly 26 percent, or almost twice the impact estimated by the District’s Office of the Chief Financial Officer.

There are several reasons why D.C. should, at the very least, expect revenue declines at the same level as Massachusetts. First, distance to jurisdictions without a ban is very short, as both Maryland and Virginia continue to allow sales of flavored tobacco. In Massachusetts, where distances are also short, the vast majority of sales moved to neighboring states, and a similar result is likely in D.C. The following map shows sales figures in the four months following the Massachusetts ban.

Second, the menthol market share in the District (60 percent) is twice as large as it is in Massachusetts (30 percent). Banning the majority of the cigarette market is likely to impact taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. collections to a much more significant degree than 13.5 percent.

If the District experiences a decline similar to Massachusetts, revenue will decline by approximately $6.5 million in the first full year after a ban is imposed. If we account for the much larger percentage of menthol smokers, the decline could be over $12 million. This figure does not include impact on tax collections from other tobacco products.

Even at the low estimate, the Office of the Chief Financial Officer concludes that “[f]unds are not sufficient in the proposed fiscal year 2022 through fiscal year 2025 budget and financial plan to implement the bill.” In other words, the District Council needs to find the lost revenue elsewhere in the upcoming budget.

State tax coffers are not all that is impacted by this ban, however. Bans impact the small business owners operating vape shops, convenience stores, and gas stations, without necessarily reducing smoking overall. Policymakers should not lose sight of the law of unintended consequences as they set tax rates and regulatory regimes for nicotine products.

Early signs indicate that flavors bans will not decrease tobacco consumption. It is not in the interest of the District of Columbia to pursue a public health measure that merely sends tax revenue to its neighboring jurisdictions without improving public health.

Share this article