Vapor products, also known as electronic cigarettes, have become commonly displayed at gas stations, convenience stores, and stand-alone vapor stores since entering in the market in 2007. While there is currently no federal excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. on vapor products, some states and localities have proposed and enacted taxes on vapor products. Localities in Alaska, Illinois, and Maryland levy their own excise taxes while the state does not.

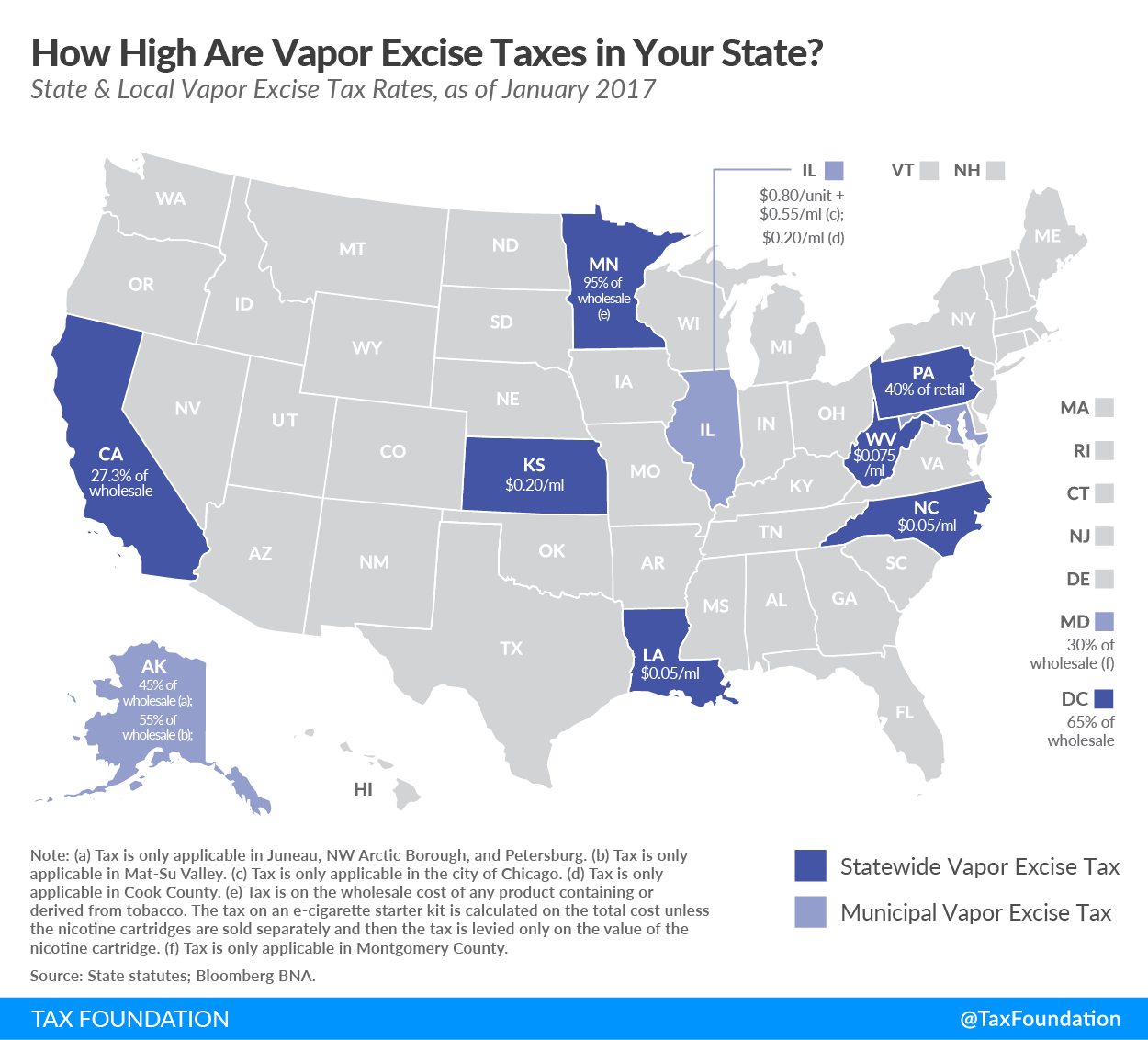

This week’s map shows where state and local vapor taxes stand today.

Taxation methods vary across states and localities. Some taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. a percentage of the wholesale value while others tax per unit or milliliter of e-liquid. The variety of taxing methods and wide range of rates indicates that there is little consensus on the best way to tax vapor products.

Of the states that tax the wholesale value, Minnesota is the highest by far (95 percent) followed by the District of Columbia (65 percent). The lowest wholesale rate is found in California (27.3 percent). Chicago levies the highest per unit tax ($0.80) plus a per milliliter rate ($0.20). Louisiana and North Carolina have the lowest per milliliter rate ($0.05).

There is a broader debate about the relative risk of vapor products compared to traditional cigarettes. Recent research shows that vaping is 95 percent less harmful compared to smoking cigarettes. However, states and localities are not necessarily considering the difference in health risk when taxing vapor. Opponents of aggressive vapor taxation argue that a high price could deter current cigarette smokers from using vapor as a tool for quitting. Proponents assert that the health risks of vapor usage are unknown and therefore taxes should be levied to offset any potential negative externalities.

Beyond these arguments, states and localities should be cautious of the negative externalities of a vapor tax itself. Cigarette smuggling and budget dependence on cigarette tax revenue are problems that could sabotage any potential benefits of a vapor tax.

Share this article