TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. reform has paid off for the Tar Heel State. North Carolina features one of the nation’s most competitive tax environments for businesses across the industry spectrum, and the state currently boasts the nation’s third-best effective tax rates for newly established firms and fifth-best rates for mature firms, according to a new analysis conducted by the Tax Foundation and KPMG LLP.[1] North Carolina’s corporate income tax rate is now the nation’s lowest at 2.5 percent, but that is just one small part of the story of the state’s competitive transformation.

Sweeping tax reforms inaugurated in 2013 and continuing for several years helped North Carolina go from having the highest corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate in the Southeast to the lowest in the country. In the process, the state abandoned a corporate tax base heavily carved out for select industries (while implicitly penalizing the rest) to one notable for its neutrality. Before the reforms and decades after the emergence of North Carolina’s Research Triangle, the state’s tax code still reflected an agrarian economy, one based on farming and textiles. Those industries were favored in the tax code, but some other industries bore the brunt of the state’s then high tax rates and uncompetitive tax structure.

Targeted incentives were pared back, tax bases broadened, and rates reduced—with reductions in the corporate income, individual income, and franchise tax rate. The sales tax base was broadened to a wider range of consumer services, with a focus on those associated with already taxable tangible property, like installation or repair. Tax incentives that only benefited a select few industries gave way to a tax structure that was more competitive across the board, and it shows with North Carolina’s highly competitive rankings in the Tax Foundation and KPMG study Location Matters: The State Tax Costs of Doing Business. These improvements are important because North Carolina is situated in a highly competitive region.

| Rank | ||

|---|---|---|

| State | New | Mature |

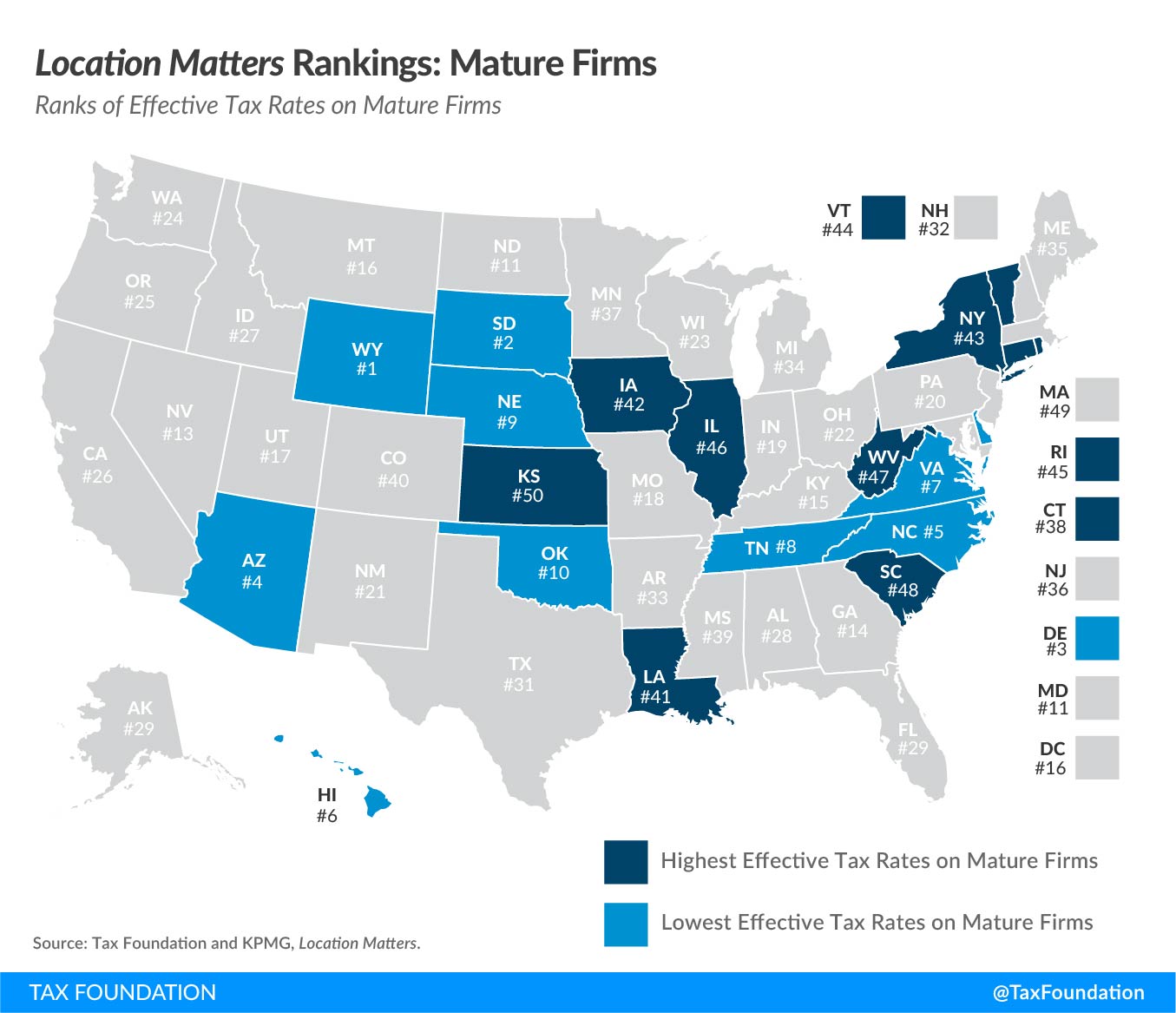

| North Carolina | 3 | 5 |

| Georgia | 4 | 14 |

| South Carolina | 42 | 48 |

| Tennessee | 15 | 8 |

| Virginia | 24 | 7 |

|

Source: Tax Foundation, Location Matters. |

||

Before the inauguration of tax reform, North Carolina’s competitiveness was lagging. State GDP was only up 1.8 percent in real terms in the seven years leading up to 2013, compared to a national average of 5.6 percent GDP growth. In the seven years following—which includes the downturn from the coronavirus pandemic—state GDP rose 9.5 percent, exceeding the 9 percent national average for the period. And over the past decade, North Carolina has seen the third-most net migration, following only Florida and Texas. Tax reform is by no means the only reason for North Carolina’s increased competitiveness or its attractiveness for those looking to relocate, but it eliminated what had been a significant impediment to the sort of growth being experienced throughout the rest of the Southeast.

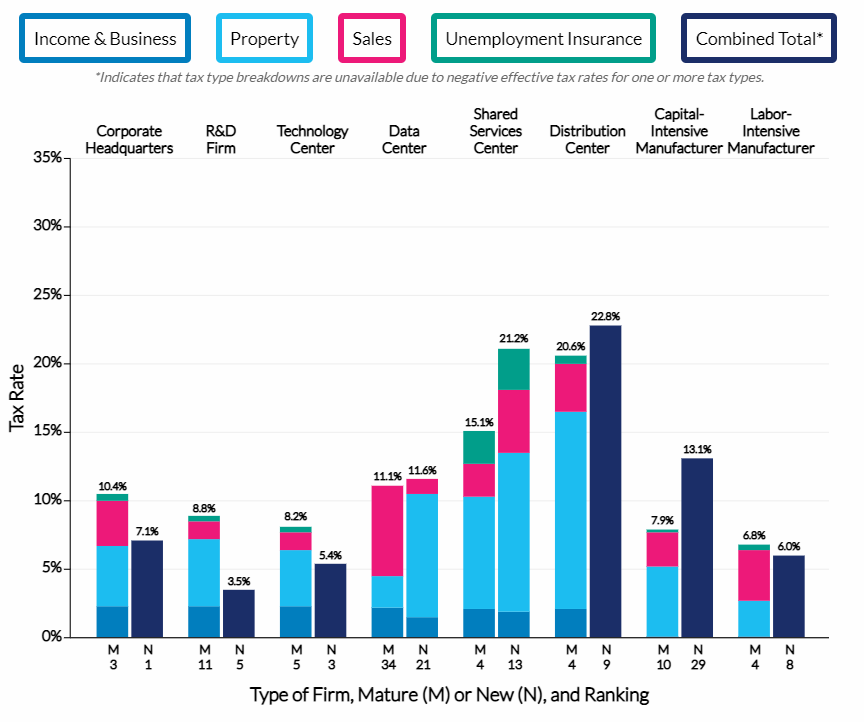

The Location Matters study compares corporate tax costs in all 50 states across eight model firms: a corporate headquarters, a research and development facility, a technology center, a data center, a shared services center, a distribution center, a capital-intensive manufacturer, and a labor-intensive manufacturer. Each firm is modeled twice, first as a new operation eligible for tax incentives and then as a mature operation not eligible for such incentives. Whereas the non-neutrality of many states’ tax codes yields starkly disparate tax treatment across firm types and maturity, North Carolina is notable for the consistency of its taxation of these firms.

For mature firms, all but one (the data center) rank between 3rd and 11th lowest effective tax rates nationwide. Five of the eight firms rank 5th or better: the corporate headquarters (3rd), shared service center, distribution center, and labor-intensive manufacturer (all 4th), and, appropriate for a state which boasts the Research Triangle, the technology center (5th). New firms also do well, with five of the eight ranking in the top 10. And rate differentials between new and mature firms tend to be modest and driven more by the changing characteristics of firms across their different stages of existence—new firms devote more resources to capital investment, for instance—than to the tax code.

| Income & Business Taxes | Property Taxes | Sales Taxes | UI Taxes | Total Effective Tax Rate | Rank | |

|---|---|---|---|---|---|---|

| Corporate Headquarters | ||||||

| Mature | 2.3% | 4.4% | 3.3% | 0.5% | 10.4% | 3 |

| New | -3.4% | 5.5% | 4.4% | 0.5% | 7.1% | 1 |

| Research & Development | ||||||

| Mature | 2.3% | 4.9% | 1.3% | 0.4% | 8.8% | 11 |

| New | -7.1% | 8.2% | 1.9% | 0.5% | 3.5% | 5 |

| Technology Center | ||||||

| Mature | 2.3% | 4.1% | 1.3% | 0.4% | 8.2% | 5 |

| New | -7.0% | 7.3% | 4.5% | 0.6% | 5.4% | 3 |

| Data Center | ||||||

| Mature | 2.2% | 2.3% | 6.6% | 0.0% | 11.1% | 34 |

| New | 1.5% | 9.0% | 1.1% | 0.0% | 11.6% | 21 |

| Shared Services Center | ||||||

| Mature | 2.1% | 8.2% | 2.4% | 2.4% | 15.1% | 4 |

| New | 1.9% | 11.6% | 4.6% | 3.0% | 21.2% | 13 |

| Distribution Center | ||||||

| Mature | 2.1% | 14.4% | 3.5% | 0.6% | 20.6% | 4 |

| New | -2.7% | 18.7% | 6.1% | 0.7% | 22.8% | 9 |

| Capital-Intensive Manufacturer | ||||||

| Mature | 0.1% | 5.1% | 2.5% | 0.2% | 7.9% | 10 |

| New | -1.6% | 11.5% | 3.0% | 0.2% | 13.1% | 29 |

| Labor-Intensive Manufacturer | ||||||

| Mature | 0.1% | 2.6% | 3.7% | 0.4% | 6.8% | 4 |

| New | -4.9% | 5.5% | 4.8% | 0.5% | 6.0% | 8 |

|

Source: Tax Foundation, Location Matters. |

||||||

Most firms in the study benefit from North Carolina’s low commercial property taxes. Unlike neighboring South Carolina and Tennessee, North Carolina does not have split roll taxation, meaning that commercial property is not subject to a higher assessment ratio than other classes of property. And unlike two other border states, Georgia and Virginia, North Carolina does not include business inventory in its property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. base.

North Carolina does, however, impose an annual franchise tax (also known as a capital stock tax). The tax is computed on the highest of three bases: apportioned net worth, net investment in property, or 55 percent of the appraised value as computed for property tax purposes. This tax, levied in addition to the corporate income tax and not on net income, can be quite burdensome to businesses that are just starting out or otherwise post losses. The tax is uncapped (some states limit total liability) and generates almost as much revenue as the corporate income tax, raising $749.6 million in Fiscal Year 2019, compared to the $830.5 million generated by the corporate income tax. In FY 2020, which included several months of the pandemic, overall revenues were down under both taxes, but the gap had narrowed still further, with the corporate income tax generating $657.8 million to the franchise tax’s $646 million.

Capital stock taxes are increasingly uncommon, as states recognize them as a barrier to investment and an impediment to the survival of struggling businesses, but they remain a mainstay of taxation in the southern U.S. At present, 16 states impose capital stock taxes, though four—Connecticut, Illinois, Mississippi, and New York—are in the process of phasing them out. Despite the regional prevalence of these taxes, North Carolina’s franchise tax is an outlier both nationally and in terms of its own otherwise highly competitive tax code.

Of all the firm types in the Location Matters study, data centers (both new and mature) and new capital-intensive manufacturers experience the highest rates in North Carolina relative to other states. The property tax base’s inclusion of machinery and equipment—not uncommon, but poor tax policy—and the franchise both contribute to these tax burdens. Burdens on data centers, moreover, are not out of line with the state’s general system of taxation; it is simply that, unlike many other states, North Carolina does not provide those firms with aggressive incentives that wipe out much of their tax liability.

Prior to tax reform, North Carolina possessed many of the pieces it needed for broad business competitiveness, but tax reform helped complete the puzzle. North Carolina now ranks first overall on Forbes’ “Best States for Business” list.[2] The state also ranks third on CNBC’s “America’s Top States for Business” list, following Virginia and Texas, and first on its “Economy” subcomponent, which includes taxes.[3] The state ranked 41st for its economy in the CNBC index a decade ago,[4] and while not all the improvement is the result of tax reforms, they have played an outsized role in this transformation.

North Carolina is not just for manufacturers anymore—though manufacturers still do quite well there. Increasingly, the state has positioned itself as an attractive location for all industries thanks to the state’s modest costs of doing business, its low regulatory burdens, and, due to recent reforms, its highly competitive tax code.

Taxes make more sense with us in your inbox.

Subscribe to our newsletter for tax insights that cut through the noise—and make sense of it.

Sign Up[1] Jared Walczak et al., Location Matters 2021: The State Tax Costs of Doing Business, Tax Foundation, May 5, 2021, https://www.taxfoundation.org/state-tax-costs-of-doing-business-2021/.

[2] Forbes, “Best States for Business,” 2019, https://www.forbes.com/best-states-for-business/list/.

[3] CNBC, “America’s Top States for Business in 2019,” updated Jan. 27, 2020, https://www.cnbc.com/2019/07/10/americas-top-states-for-business-2019.html.

[4] CNBC, “Top States 2011: Overall Rankings,” June 2011, https://www.cnbc.com/top-states-2011-overall-rankings/.

Share this article