One of the ways lawmakers intend to pay for $3.5 trillion of new spending in the budget reconciliation package is by creating “health care savings.” The leading proposal to achieve this is H.R. 3, the Elijah Cummings Lower Drug Costs Now Act, which would change the way that prescription drug prices are negotiated under Medicare Part D drugs by implementing the threat of steep tax penalties. While the policy would result in savings for patients and the federal government, it would come with the significant tradeoff of reduced medical innovation.

Under current law, drug prices for Medicare Part D are determined through negotiations between manufacturers, pharmacies, and prescription drug plans (PDPs). The federal government’s role is limited by a “non-interference provision.” H.R. 3 would change that by requiring the Health and Human Services (HHS) Secretary to negotiate prices for certain drugs.

The drug prices in question would not be permitted to exceed 120 percent of the average international market (AIM) price in a reference group of six countries (Australia, Canada, France, Germany, Japan, and the United Kingdom). Drugs without an AIM price would be subject to different rules limiting their price. The negotiated prices would be used for Medicare Part D, and they would also be available to insurers in commercial markets.

But, as the Congressional Budget Office (CBO) found in a past analysis, for such negotiations to result in meaningful price concessions, the Secretary would need to have leverage—in other words, a “stick.”

Without a stick, “CBO concluded that providing broad negotiating authority by itself would likely have a negligible effect on federal spending.” Further, the CBO explained that “The authority to establish a formulary, set prices administratively, or take other regulatory actions [emphasis added] against firms failing to offer price reductions could give the Secretary the ability to obtain significant discounts in negotiations with drug manufacturers.” That is where the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. comes in.

Under H.R. 3, if drug manufacturers do not agree to participate in negotiations, or do not agree to the negotiated price, they would be subject to an escalating excise tax on the sale of the drug in question. The tax would kick in at 65 percent and would rise by 10 percentage points each 90 days the manufacturers are in “noncompliance,” reaching a maximum tax rate of 95 percent.

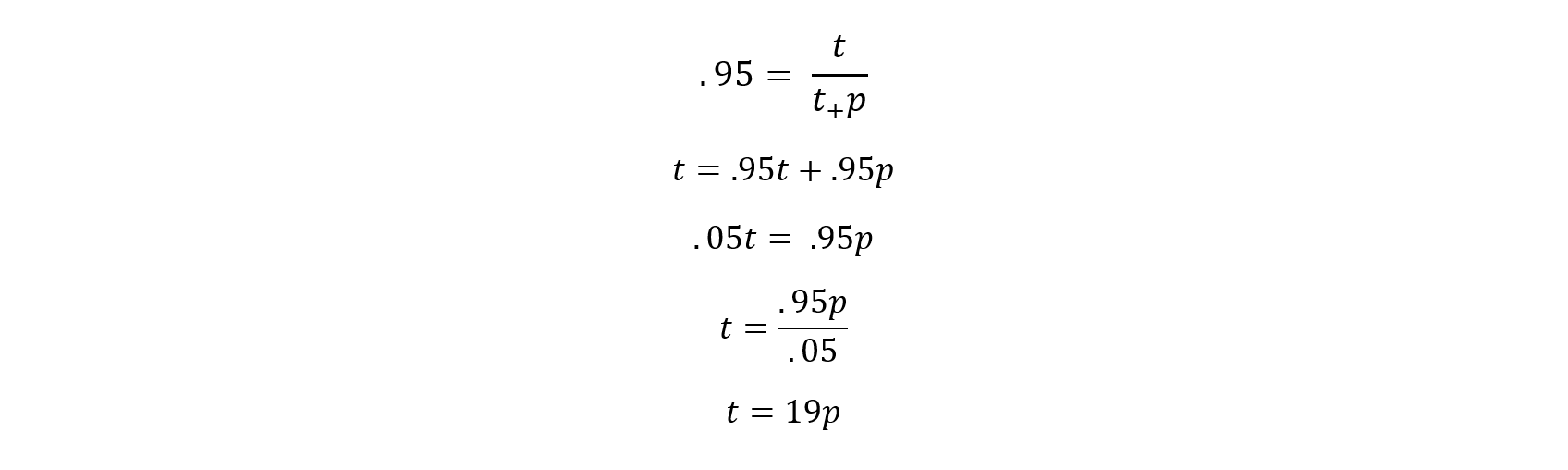

While most reporting refers to the tax as a 95 percent tax applied to gross sales, the text of H.R. 3 opens the door to an even higher extreme. Rather than describing the applicable rate applying to sales, the text states:

There is hereby imposed on the sale by the manufacturer, producer, or importer of any selected drug during a day described in subsection (b) a tax in an amount such that the applicable percentage is equal to the ratio of—

“(1) such tax, divided by

“(2) the sum of such tax and the price for which so sold.

If that is interpreted to mean the following, then the excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. rate under H.R. 3 could reach a maximum of 1,900 percent, where t means such tax and p means the price for which a drug sold.

Whether the rate applied to sales is 95 percent or 1,900 percent, the amount of tax paid would not be deductible when companies calculate their taxable income for income tax purposes. Disallowing deductibility means companies would have to pay income tax on resources used to pay the excise tax, which means the total tax rate would exceed 100 percent. In other words, even under a 95 percent rate, the combination of taxes would lead companies to lose money if the drug in question was sold in the United States.

The CBO and Joint Committee on Taxation (JCT) estimated in June 2020 that the policy would save the federal government $581 billion from 2021 through 2030—forcing companies to lower their prices does save some money for Medicare and lead to increased use of prescription drugs. The JCT expects that all manufacturers would either participate in the negotiation process (or pull a particular drug out of the U.S. market entirely) rather than pay the excise tax on sales—so the excise tax itself does not raise revenue.

But forcing companies to lower drug prices comes with negative tradeoffs. According to another CBO analysis of a previous version of H.R. 3: “The lower prices under the bill would immediately lower current and expected future revenues for drug manufacturers, change manufacturers’ incentives, and have broad effects on the drug market.”

Due to declining revenues, pharmaceutical manufactures may reduce their spending on research and development (R&D). CBO estimates that a reduction of pharmaceutical revenues ranging from $0.5 trillion to $1 trillion would mean 8 to 15 fewer new drugs coming to market over 10 years.

Against a baseline of approximately 300 new drugs anticipated over 10 years, that means CBO expects H.R. 3 could cause a 5 percent reduction in new drug innovation. While Americans would benefit from lower prices, they would be harmed by a reduction in medical innovation.

The bill could also have knock-on effects, such as reducing the attractiveness of making risky investments in the drug industry. As Doug Holtz-Eakin rightly explains, in that case, the CBO’s estimate of reduced innovation from a drop in revenues could be viewed as a “lower bound for the loss of innovation.”

H.R. 3 would be bad for medical innovation, which calls into question whether it would have a positive effect on America’s health overall. As the CBO explains, “The overall effect on the health of families in the United States that would stem from increased use of prescription drugs but decreased availability of new drugs is unclear.” Forcing companies to lower drug prices under the threat of a confiscatory tax is not an advisable way to pay for new government spending, nor to improve health outcomes.

Share this article