Inflation operates much like a tax, a particularly egregious one that disproportionately falls on the poor and leads to a variety of economic problems, including, as we’re seeing, higher interest rates, slow economic growth, and reduced incomes.

With inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin still running high, it is worth exploring who bears the cost of the surge in prices over the past year and a half. While academic evidence shows that bondholders and consumers bear much of the burden of inflation over the long run, a new Congressional Budget Office (CBO) report reveals that lower- and middle-income households are disproportionately shouldering the burden of this current inflation wave.

Inflation is a general increase in prices, commonly measured by the Consumer Price Index (CPI)—currently up 8.3 percent over the last year—or the Produce Price Index (PPI)—up 8.7 percent—among other measures. These general price increases are sometimes referred to as an “inflation tax,” and not without reason.

Inflation is a burden on all those who use U.S. dollars, but the burden varies considerably across users. For instance, it falls particularly heavy on lenders, who subsequently are repaid in less valuable dollars. In contrast, borrowers benefit from inflation, with the single largest beneficiary being the federal government, as Treasury debt is repaid with less valuable dollars. Publicly held Treasury debt is currently about $24 trillion, roughly the size of U.S. GDP.

There is a long history of the federal government using inflation, or money creation, to finance spending instead of taxes, particularly in times of war. For example, the sharp increase in federal spending during World War II produced large fiscal deficits that were financed by Treasury debt. The debt was purchased by the Federal Reserve through printing money, or “seignorage,” and added to the Fed’s balance sheet under an agreement to suppress interest rates, and thus borrowing costs, for the federal government. The agreement remained in place until 1951, when the Federal Reserve regained a degree of independence from the Treasury. Over this period, from the outbreak of the war in 1939 to 1951, the CPI rose a cumulative 87 percent.

Recent studies (ungated versions here and here) by economists Thomas Sargent and George Hall document the financing of major wars in U.S. history, including what they term the “War on COVID-19,” which shares certain key features with other major wars. Namely, the federal government responded to the pandemic with a surge in spending primarily financed by issuing Treasury bonds, much of which were then purchased by the Federal Reserve, increasing the supply of money in the economy.

Sargent and Hall find the surge in spending in response to COVID-19, amounting to about $5 trillion through 2021, was financed almost entirely (more than 97 percent) by debt and money creation, rather than higher taxes. In contrast, higher taxes financed a considerably larger share of spending for World Wars I and II (21 percent and 30 percent, respectively), and yet the substantial increases in debt and money creation from those wars led to large losses for bondholders and consumers, as the price level grew more than 50 percent over several years.

It remains to be seen how the War on COVID-19 will translate into higher inflation in the years to come. Thus far the CPI has grown 15.3 percent since December 2019, but the historical analysis by Sargent and Hall, as well as the theoretical analysis by economist John Cochrane, indicates there is much more to come.

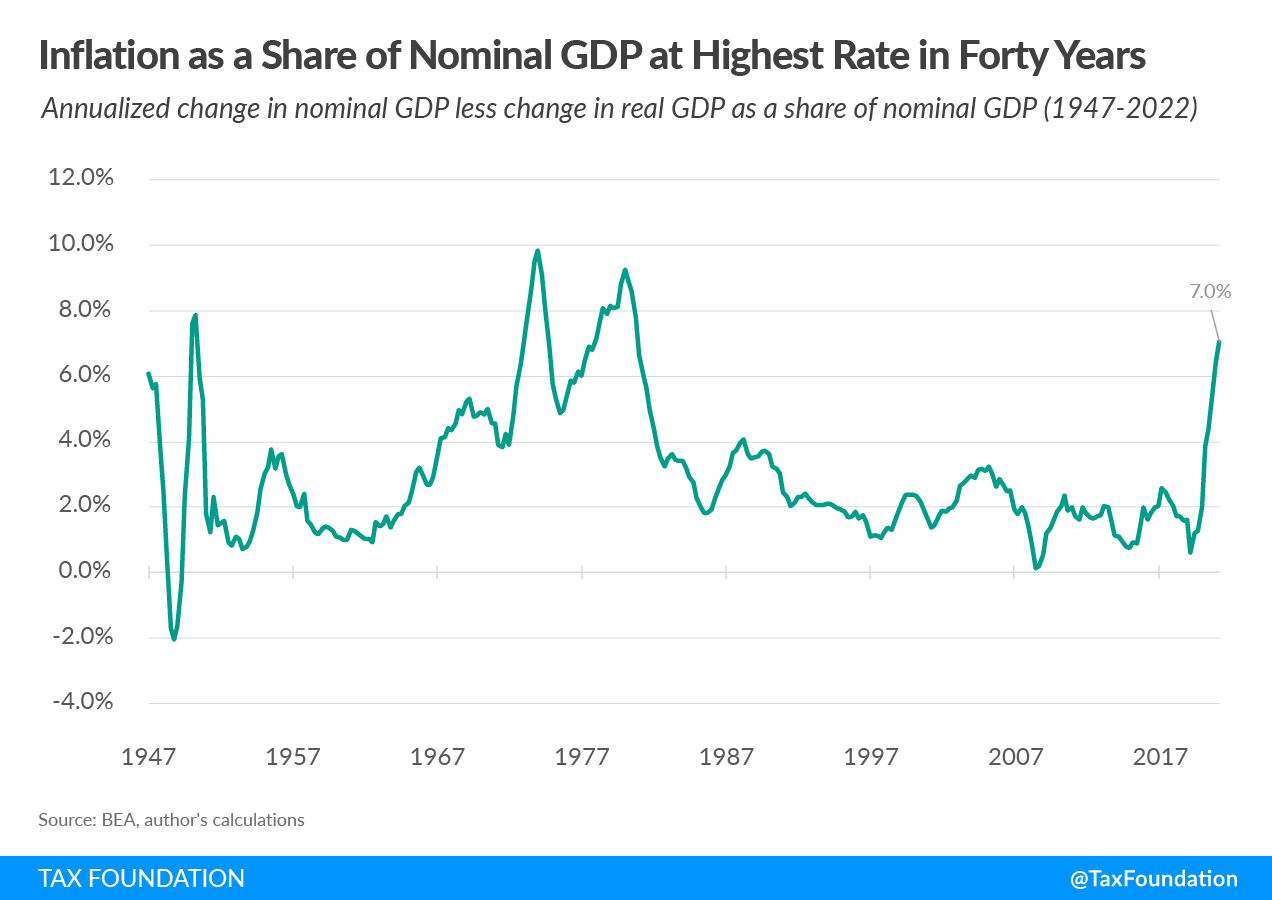

One way to monitor the size of the inflation taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. is to track changes in nominal GDP, that is, GDP unadjusted for inflation. According to the latest data from the Bureau of Economic Analysis, nominal GDP as of the second quarter of this year was $24.9 trillion, up $2.1 trillion from a year ago. However, most of that growth—$1.8 trillion—is due to inflation.

To put that in context, the federal government will collect about $5 trillion in tax from all sources this year. As a share of nominal GDP, inflation amounted to 7.0 percent as of the second quarter, up from about 1.6 percent at the end of 2019, prior to COVID-19, and the highest since 1981.

New analysis from the CBO underscores how low- and middle-income households have been impacted by the current inflation wave. The paper shows that prices for goods consumed by the lowest income quintile have risen faster than those for goods consumed by households in the highest income quintile—4.6 percent versus 4.3, respectively—on an annualized basis from 2019 to 2022.

The differences are mainly driven by higher prices for food and energy, which comprise a larger share of the consumption for low-income households compared to higher-income households. Additionally, services other than rent account for a larger share of consumption for high-income households—32 percent compared to 23 percent—and have experienced less price growth than goods over this period.

Distributional concerns typically dominate in debates about the fairness of various public financing sources, but there are other things to consider, such as procedural fairness. How procedurally fair is it that inflation appears now to be the primary means of financing pandemic relief spending, more than a year and a half after the $1.9 trillion American Rescue Plan was enacted and more than two and a half years after the first relief package was enacted?

Very few people (voters or elected officials) anticipated this inflationary outcome, but many did voice concerns about the impacts on the deficit and the national debt. It seems clear now in retrospect that one of the major downsides to deficit spending is the unknown liabilities it creates for future taxpayers and consumers and the potential destabilizing macroeconomic forces it unleashes. It is incumbent upon our elected officials to take that into account, even during the emergency of a pandemic.

Now that the emergency has passed, our elected officials should spare people further harm from the inflation tax by committing to sustainable, balanced budgets.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe