New Jersey Considers Deeply Flawed Data Tax in Waning Days of Session

New Jersey’s proposed data tax on corporations is based on dubious premises and made worse by its poor design.

5 min read

Jared Walczak is a Senior Fellow at the Tax Foundation, where he spent five years as Vice President of State Projects, and president of Walczak Policy Consulting.

Jared has written or co-written tax reform guides for more than a dozen states and has served as the principal author of the Tax Foundation’s State Tax Competitiveness Index and Location Matters. He is also a regular on the conference circuit and has testified before legislatures in 35 states. His efforts have been instrumental in securing tax reform in many states, including sweeping reforms in Iowa and Louisiana, along with substantive reforms in Georgia, Idaho, Kentucky, Missouri, North Carolina, Oklahoma, Utah, West Virginia, and Wyoming, among others.

Jared also serves as a member of the faculty of the Institute for Professionals in Taxation, sits on the state tax advisory board of the Institute for State Policy Leaders, and contributes to Tax Notes State magazine. He is the author of the “SALT Road” Substack, a free newsletter on state and local tax policy.

New Jersey’s proposed data tax on corporations is based on dubious premises and made worse by its poor design.

5 min read

Some state lawmakers are considering decoupling from the pro-growth expensing provisions of the OBBBA due to revenue concerns, but it is valuable to recognize just how much the corporate tax base has expanded over the past decade.

6 min read

The State Tax Competitiveness Index enables policymakers, taxpayers, and business leaders to gauge how their states’ tax systems compare. While there are many ways to show how much state governments collect in taxes, the Index evaluates how well states structure their tax systems and provides a road map for improvement.

122 min read

Taxes are an important part of the mix, and modernizing a state’s tax structure helps position it for growth. States that rank better on the Index have better-structured tax codes, and states with better-structured tax codes get Wins Above Replacement.

5 min read

Illinois lawmakers are attempting to rush through a harmful mark-to-market capital gains tax proposal that captures unrealized gains.

7 min read

The past four years have brought significant focus on state income tax reform and relief, and with that, something of a flat tax revolution.

11 min read

With property tax bills on the rise, homeowners are searching for answers—and some even want to abolish the tax altogether. In this episode, we break down why property taxes are increasing, common but flawed solutions, and why the property tax remains an economically efficient revenue source.

Backfilling forgone local property tax revenue through new state taxes is difficult because it dramatically shifts overall tax burdens, undermines local accountability, and cannot easily adjust for changing population mixes.

20 min read

When the Kansas City and Los Angeles squads face off in São Paulo, the players will owe Brazil’s nonresident income tax on the share of income they earned there, while California will lose out on the nonresident income taxes that Chiefs players ordinarily would have remitted in what is nominally a Chargers home game.

5 min read

Congress may have passed the One Big Beautiful Bill Act (OBBBA), but state lawmakers now face big choices. Most states link their tax codes to the federal system, meaning OBBBA’s provisions—good and bad—are about to ripple across state budgets.

For Congress, work on the One Big Beautiful Bill Act is done. But in state capitols, the work has not yet begun. Many of the tax changes in the federal reconciliation act flow through to state tax codes—automatically in some states, and subject to an update in states’ Internal Revenue Code conformity date in others.

39 min read

However states choose to respond to other tax provisions of the One Big Beautiful Bill Act, they should conform to the pro-growth provisions, which represent a marked improvement in the corporate tax code.

12 min read

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

10 min read

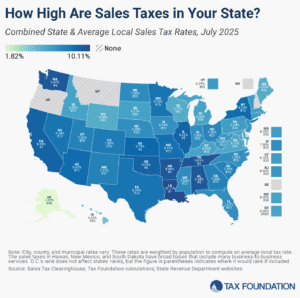

The five states with the highest average combined state and local sales tax rates are Louisiana (10.11 percent), Tennessee (9.61 percent), Arkansas (9.48 percent), Washington (9.47 percent), and Alabama (9.44 percent).

10 min read

The Senate’s version of the OBBB restores the benefit of avoiding the SALT deduction cap with PTETs for all pass-through businesses, while placing new limits on the extent of the workarounds.

6 min read

President’s Trump’s policies would throw high-tax states a life raft as they swim against the tide—before potentially hitting all states with a tariff-induced economic tsunami that could force lawmakers’ hands and reverse recent tax relief.

For owners of pass-through businesses, the reconciliation package (1) raises the state and local tax (SALT) deduction cap, (2) denies the benefit of pass-through entity-level taxes that had previously worked around the SALT cap for such pass-through businesses, and (3) increases the Section 199A deduction for qualifying pass-through entities.

4 min read

As the US House hashes out its “One, Big, Beautiful Bill,” statehouse lawmakers are watching closely, given the impact of both its tax and spending provisions on state budgets.

12 min read

As home values have spiked, Florida and other states are weighing elimination of property taxes.

In Washington, Gov. Ferguson (D) will soon have to act on legislation enacting a far more sweeping tax on Washington-based businesses than lawmakers imagined.

7 min read