Inequality is a hot topic these days. Everyone seems to want to write about it. The launch of TheUpshot, the new project from the New York Times, included a story on the wealth of the middle class, the Times Sunday Review had a column on inequality and economic mobility, and Matt Yglesias can tell you “everything you need to know” about it.

But in the discussion of the cause of all this inequality, it’s sometimes good to look beyond all the data and rely on economic intuition. From a Ball and Mankiw paper:

“The fall in the capital stock affects factor prices: wages fall, harming workers, and the returns to capital rise, benefiting capital owners.”

Mankiw and Ball are talking about the crowding out of capital caused by a deficit in this scenario, but the effects are the same. When the service price of capital goes up and investment goes down. When fewer people are willing to invest, two things happen. First, the capital stock (i.e. the amount of computers, factories, equipment) shrinks over time, which makes workers less productive and decreases future wages. Second, because there is less capital available the available capital is more valuable, which causes the return to capital to rise.

The effect of this over time is that wage earners make less and capital owners make more.

Our current tax code exacerbates this problem significantly through its non-neutral bias towards consumption over future consumption (i.e. saving).

The evidence is fairly clear that America is a nation that likes to consume: 72 percent of our GDP is consumption. We are second on this measure behind only Greece at 75 percent. Meanwhile, our ratio of investment to GDP is second to last, just behind the United Kingdom, at 16 percent.

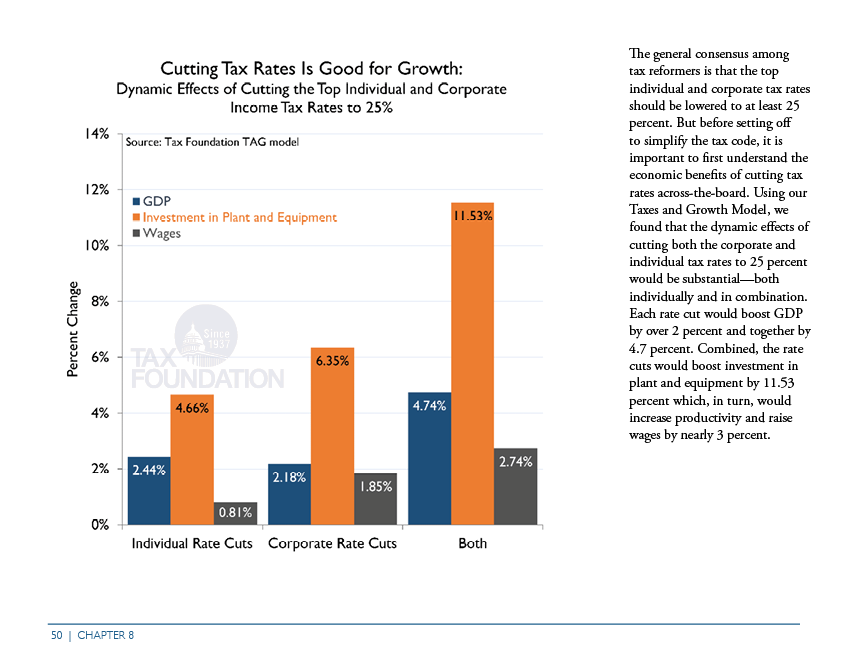

Low levels of investment can have a lasting impact. Saving and investment drive an economy forward.

There are many steps we can take to fix our predicament – improved K through 12 education, fewer barriers to starting businesses, etc. – but because taxes have a direct impact on the cost of capital and the amount of investment, taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. reform may be the best place to start.

In many respects, countries in the OECD have recognized the damage caused by taxes like the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. and have taken action to lower the tax burden on investment. Since 1980, the OECD average corporate tax rate has gone from around 50 percent to about 25 percent today.

Today, the U.S. has the highest corporate tax rate in the OECD, the sixth highest capital gains taxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment. rate, the ninth highest dividend tax rate, and the 25th worst cost recovery system. Additionally, the U.S. tax code double taxes investment, first at the corporate level and then the shareholder level, and has the most progressive tax code in the OECD.

All these factors contribute to a high tax burden on investment in the U.S. It’s important for that to change.

Reforms to improve the tax system and lower the cost of capital would mean good things for American workers. A cut in the corporate and top individual tax rate to 25 percent would grow the economy significantly and lead to large increases in wages and investment.

{kind=link}

If we takes steps to lower the cost of capital through full expensing or tax cuts, we will see two things happen. First, more people will decide to invest instead of spend, which will lead to a larger capital stock and higher wages. Second, because more capital is available, the existing capital will become less valuable than before, and returns to capital will shrink.

The effect overtime is that as the cost of capital declines, wage earners will earn more and capital owners will earn less. What would that do to inequality?

Share this article