During last year’s legislature’s special session in Maine, two bills, H.P. 1039 and H.P. 1258, would have doubled the excise tax on cigarettes to $4.00 a pack. Neither bill passed, but both have carried over to this year’s session and H.P 1258 will be heard by the Health and Human Services Committee in February.

These proposals will not just impact cigarettes: by virtue of Maine law, all other tobacco products would also be subject to a 100 percent rate increase. The proposals share at least four major issues: flawed revenue allocation, risk of increased smuggling, regressivity, and violation of the harm reduction principle.

The impetus for the increase is a desire to limit tobacco use and increase funding for Maine’s Department of Health and Human Services and the Maine Center for Disease Control and Prevention. H.P. 1039 allocates $17 million to these agencies and H.P 1258 allocates 50 percent of collections to the Fund for a Healthy Maine. Given the excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections.’s purpose of recovering societal costs associated with tobacco use, this allocation is defensible. However, an increase in the rate is not necessary to achieve these funding targets.

H.P. 1039 states that all revenue collected from tobacco sales will be dedicated to these tobacco control funds, but it also stipulates that if funding recommendations by the U.S. Centers for Disease Control and Prevention (CDC) for state tobacco control programs are lower, the lower of the figures will prevail. The CDC currently recommends that 12 percent of taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. revenue be dedicated to tobacco control, and 12 percent of $143 million is roughly $17 million. Any additional revenue beyond the $17 million would likely be dedicated to the general fund.

If Maine estimates societal cost, called negative externalities, to be around $17 million above current allocations, there is no reason to double the excise tax rates. The current levy raises well above that figure already. A doubling of the rates looks more like arbitrary taxation meant to bolster general fund collections, and excise taxes are poor vehicles for stable revenue due to their narrow design.

Reallocating existing funds would be a much better policy, because doubling the rates introduces a risk for unintended consequences. The Mackinac Center, which publishes an annual analysis of cigarette smuggling, estimates that a 100 percent increase of cigarette taxes in Maine would more than triple inbound smuggling rates (from 8 percent in 2018 to 25 percent).

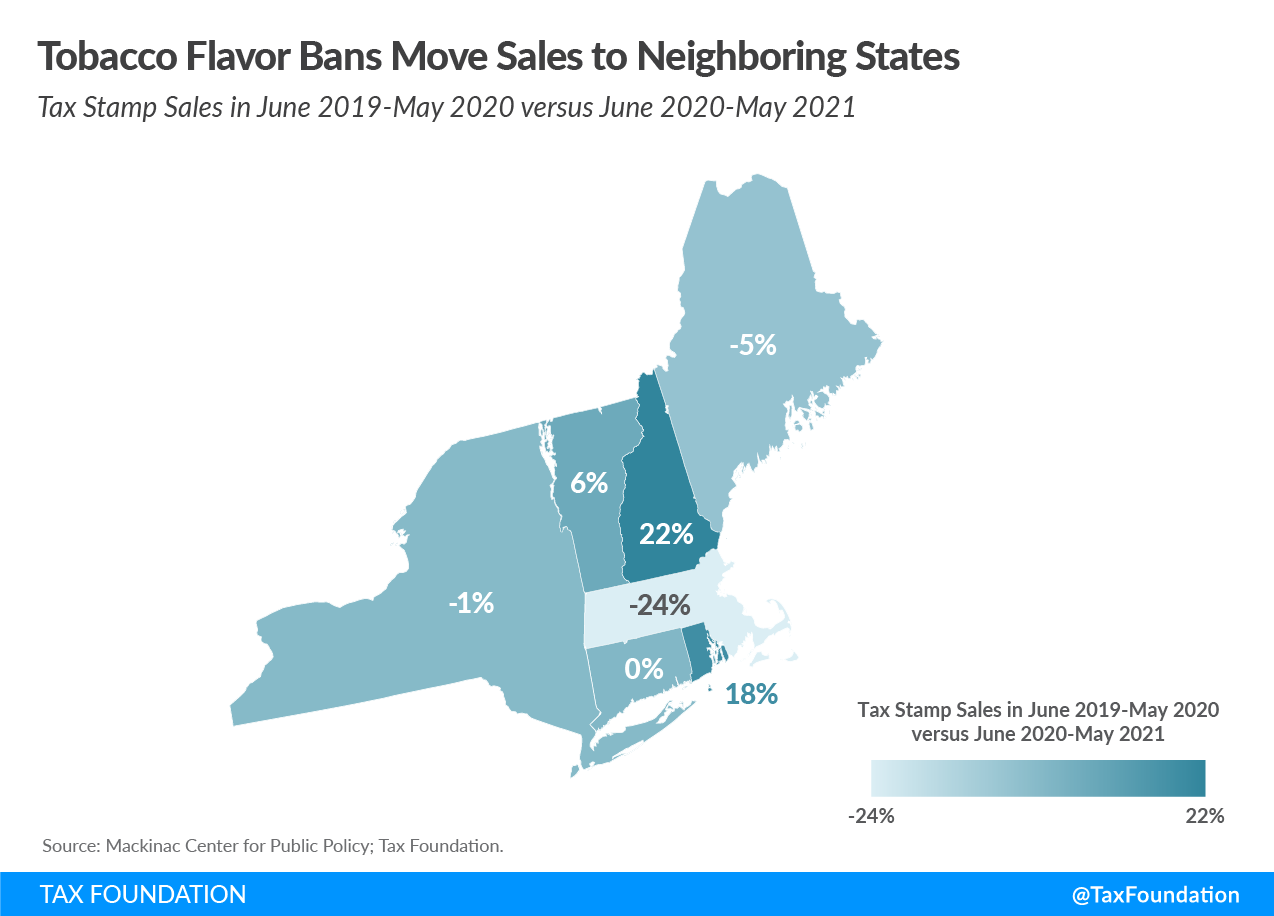

Mackinac’s estimate only considers the impact of a tax increase, but H.P. 1258 also contains a flavor ban. Tobacco flavor bans are likely to severely increase cross-border trade. Nearby Massachusetts is the only state to have implemented a tobacco flavor ban, and it has experienced significant declines in tobacco tax revenue while New Hampshire and Rhode Island have seen double-digit growth. These numbers indicate that consumption has not changed to a significant degree—smokers have simply changed where they purchase the products.

Were Maine to follow in Massachusetts’ footsteps, New Hampshire would likely experience even larger increases in tobacco sales and excise tax revenue.

In addition to the smuggling risk, excise taxes tend to be regressive, and some more so than others. Tobacco is especially regressive because consumption usually increases as income decreases—contrary to regular consumption. This results in higher consumption among young people, low-income earners, racial and ethnic minorities, and those without a college education. In Maine, a college graduate is eight times less likely to smoke compared to a resident without a high school degree. In other words, the brunt of this tax increase would fall on those least able to afford it.

Outside of the risk associated with increasing cigarette taxes, the bill also doubles taxation of vapor products. Today, these products are taxed at 43 percent of value at wholesale level, and this rate would increase to 86 percent. The rate on vapor products is designed to be equal to the rate on cigarettes, but taxing vapor products at the same rate as cigarettes violates the harm reduction principle. Cigarettes and vapor products are economic substitutes, and—even if vapor products are unhealthy in their right—they represent an attractive alternative to combustible cigarettes.

Vapor products can deliver nicotine, the addictive component of cigarettes, without the combustion and inhalation of tar that is a part of smoking cigarettes. While more research relating to the potential harm-reduction qualities of vapor products is needed, for now, the consensus is that vapor products are less harmful than traditional combustible tobacco products. Public Health England, an agency of the English Ministry for Health, concludes that vapor products are 95 percent less harmful than cigarettes.

Tax policy should encourage the switch to limit harm and to limit smoking—not the other way around, and if Maine’s excise taxes are supposed to account for negative externalities, vapor taxes should be lower relative to combustible products. Even though the increases are proportional, this bill would place a very high rate on vapor products and maintain a ratio that does nothing to encourage people to switch to less harmful products. Furthermore, revenue from taxes on cigarettes should be allocated to offset costs associated with consumption, since raising general fund revenue by increasing narrow-based and regressive taxes is not advisable.

Share this article