Of the several tax increases that Vice President Kamala Harris has proposed, raising the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate from 21 percent to 28 percent is the largest. The Harris campaign has described this taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. hike as “a fiscally responsible way to put money back in the pockets of working people.” However, much of this tax increase would fall on workers in the form of lower wages. For example, analysis by the Alliance for Competitive Taxation (ACT) finds that the tax increase would reduce average wages by as much as $597 per US worker each year. In some states, the drop in wages would exceed $700 per worker.

Economists have known for decades that a portion of the corporate tax is borne by workers, as it causes corporations to reduce investment, resulting in lower productivity, lower wages, and fewer job opportunities. While there are a range of estimated impacts, most studies find substantial downsides for workers, with labor typically bearing around half or more of the corporate tax. The remainder of the corporate tax burden falls on shareholders, including pension account owners, many of whom are low-income households. Consumers are also harmed through higher prices according to some studies.

In one of the more recent and comprehensive studies, economists Li Liu and Rosanne Altshuler use variation in effective corporate tax rates across the US and industries over time to estimate that about 60 percent of the corporate tax is borne by workers in the form of lower wages. At the lower end of the range of estimates, the Joint Committee on Taxation and the Congressional Budget Office assume 25 percent of the corporate tax is borne by labor.

ACT uses this range of estimates to calculate the impact on workers’ wages of increasing the corporate tax rate to 28 percent (assuming no change in employment). First, taking the Treasury Department’s estimated revenue from raising the corporate tax rate ($1.3 trillion over a decade, or $135 billion per year on average) and multiplying it by the share borne by workers (25 percent to 60 percent) yields a total loss of wages ranging from $34 billion to $81 billion per year. Dividing by the number of workers in the US (136 million as of 2022 according to the Census Bureau) indicates the average wage loss per worker would range from $249 to $597 per year.

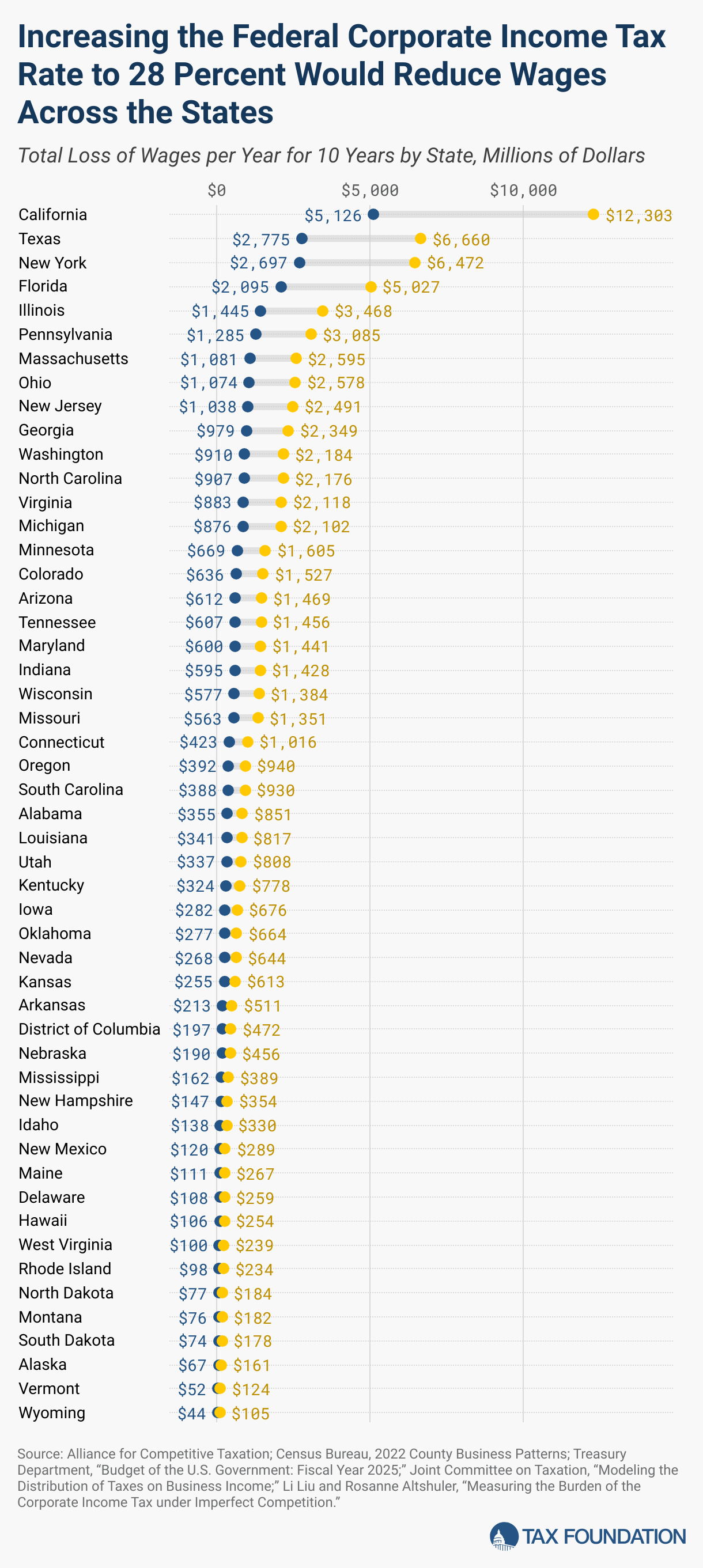

The calculation can be done for each state based on its share of total payroll (using Census data). As shown in the table below, at the high end of the range (using the 60 percent incidence assumption), workers in California, Massachusetts, New York, Washington, and the District of Columbia would see average wage losses that would top $700 annually. Even at the low end of the range (using the 25 percent incidence assumption), workers would face a reduction in average annual wages of nearly $200 in several low-income states, including Mississippi, West Virginia, New Mexico, Montana, and South Carolina.

At the congressional district level, the ACT analysis indicates a range of impacts. At the high end of the estimates (using the 60 percent incidence assumption), some congressional districts would see an average drop in average annual wages exceeding $1,700 per worker.

As mentioned, this approach assumes no change in total employment, but in reality, both employment and wages would be negatively affected by a corporate tax hike. Our modeling of Harris’s proposal to raise the corporate rate to 28 percent indicates it would reduce the number of full-time equivalent jobs by 125,000 and reduce wages by 0.5 percent (in the middle of the range of wage impacts shown in the table below), while reducing GDP by 0.6 percent over the long run. We find Harris’s broader tax plan would eliminate 786,000 jobs, reduce wages by 1.2 percent, and shrink GDP by 2 percent, with the most damaging tax increase being the proposed hike in the corporate tax rate.

Harris’s proposal to raise the corporate tax rate by 33 percent would be a costly mistake, with a large part of the cost falling on workers in the form of lower wages and fewer jobs. When considering options to pay for various initiatives, the Harris campaign should look for alternatives less harmful to workers.

Wage Impacts of Increasing the Federal Corporate Income Tax Rate to 28 Percent

| State | Total Loss of Wages per Year for 10 Years (Millions) | Average Wage Loss per Year per Employee for 10 Years | ||||

|---|---|---|---|---|---|---|

| United States | $33,749 | to | $80,996 | $249 | to | $597 |

| Alabama | $355 | to | $851 | $199 | to | $479 |

| Alaska | $67 | to | $161 | $261 | to | $625 |

| Arizona | $612 | to | $1,469 | $220 | to | $527 |

| Arkansas | $213 | to | $511 | $196 | to | $470 |

| California | $5,126 | to | $12,303 | $320 | to | $767 |

| Colorado | $636 | to | $1,527 | $256 | to | $616 |

| Connecticut | $423 | to | $1,016 | $281 | to | $674 |

| Delaware | $108 | to | $259 | $254 | to | $610 |

| District of Columbia | $197 | to | $472 | $373 | to | $895 |

| Florida | $2,095 | to | $5,027 | $218 | to | $522 |

| Georgia | $979 | to | $2,349 | $230 | to | $553 |

| Hawaii | $106 | to | $254 | $209 | to | $501 |

| Idaho | $138 | to | $330 | $200 | to | $479 |

| Illinois | $1,445 | to | $3,468 | $261 | to | $627 |

| Indiana | $595 | to | $1,428 | $207 | to | $496 |

| Iowa | $282 | to | $676 | $203 | to | $488 |

| Kansas | $255 | to | $613 | $208 | to | $500 |

| Kentucky | $324 | to | $778 | $194 | to | $467 |

| Louisiana | $341 | to | $817 | $207 | to | $497 |

| Maine | $111 | to | $267 | $209 | to | $502 |

| Maryland | $600 | to | $1,441 | $246 | to | $591 |

| Massachusetts | $1,081 | to | $2,595 | $318 | to | $764 |

| Michigan | $876 | to | $2,102 | $222 | to | $534 |

| Minnesota | $669 | to | $1,605 | $245 | to | $587 |

| Mississippi | $162 | to | $389 | $171 | to | $411 |

| Missouri | $563 | to | $1,351 | $220 | to | $527 |

| Montana | $76 | to | $182 | $190 | to | $455 |

| Nebraska | $190 | to | $456 | $213 | to | $512 |

| Nevada | $268 | to | $644 | $208 | to | $500 |

| New Hampshire | $147 | to | $354 | $240 | to | $575 |

| New Jersey | $1,038 | to | $2,491 | $272 | to | $653 |

| New Mexico | $120 | to | $289 | $188 | to | $452 |

| New York | $2,697 | to | $6,472 | $320 | to | $768 |

| North Carolina | $907 | to | $2,176 | $221 | to | $530 |

| North Dakota | $77 | to | $184 | $224 | to | $537 |

| Ohio | $1,074 | to | $2,578 | $216 | to | $519 |

| Oklahoma | $277 | to | $664 | $199 | to | $478 |

| Oregon | $392 | to | $940 | $235 | to | $564 |

| Pennsylvania | $1,285 | to | $3,085 | $230 | to | $552 |

| Rhode Island | $98 | to | $234 | $222 | to | $534 |

| South Carolina | $388 | to | $930 | $193 | to | $462 |

| South Dakota | $74 | to | $178 | $198 | to | $475 |

| Tennessee | $607 | to | $1,456 | $213 | to | $511 |

| Texas | $2,775 | to | $6,660 | $241 | to | $579 |

| Utah | $337 | to | $808 | $221 | to | $531 |

| Vermont | $52 | to | $124 | $203 | to | $487 |

| Virginia | $883 | to | $2,118 | $253 | to | $606 |

| Washington | $910 | to | $2,184 | $306 | to | $733 |

| West Virginia | $100 | to | $239 | $185 | to | $443 |

| Wisconsin | $577 | to | $1,384 | $222 | to | $532 |

| Wyoming | $44 | to | $105 | $210 | to | $503 |

Share this article