Proposal for Reporting Requirements for Financial Institutions Misses the Mark

Reducing the tax gap is a good idea, but the reporting requirements for financial institutions could be better-targeted at the problem at hand.

4 min read

Alex Muresianu was a Senior Policy Analyst at the Tax Foundation, focused on federal tax policy. Previously, Alex worked on the federal team as an intern in the summer of 2018 and as a research assistant in summer 2020.

He attended Tufts University, graduating with a degree in economics and minors in finance and political science in February 2021. He also worked for the Pioneer Institute in 2019, spent a summer as a journalism intern at Reason magazine, and written op-eds for various print and online publications.

Alex originally hails from outside Boston, and enjoys Dungeons and Dragons, ’80s movies (Back to the Future, Indiana Jones, the Schwarzenegger filmography, Die Hard, etc.), and classic rock.

Reducing the tax gap is a good idea, but the reporting requirements for financial institutions could be better-targeted at the problem at hand.

4 min read

A carbon tax would be a less economically harmful pay-for than either personal or corporate income tax hikes and a more efficient way to reduce carbon emissions than green energy tax credits, but would come with other trade-offs.

4 min read

The latest version of the Biden Build Back Better agenda, released last week by the House Ways and Means committee, is dense, with too many provisions to flesh out completely. Here’s a rundown of the good, the bad, and the ugly of it.

7 min read

As Congress considers several tax proposals designed to raise taxes on high-income earners, it’s worth considering the distribution of the existing tax code.

3 min read

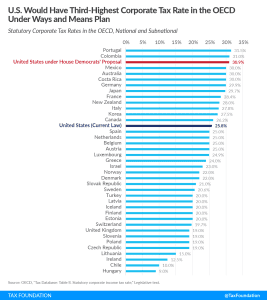

Under the Ways and Means text, the U.S. would have an average corporate tax rate of 30.9 percent, which would be the third-highest corporate tax rate in the OECD, behind only Colombia and Portugal.

1 min read

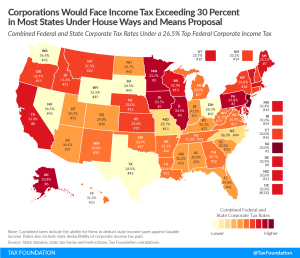

Under the House Democrats’ tax plan, companies in 21 states and D.C. would face a higher corporate tax rate than in any country in the OECD.

1 min read

The Biden administration does have a point about how some components of the infrastructure bill could put downward pressure on inflation in the long term. However, the taxes chosen to pay for those investments would counteract those effects, by reducing investment and productivity growth.

4 min read

Congressional lawmakers are putting together a reconciliation bill to enact much of President Biden’s Build Back Better agenda. Many lawmakers including Senate Finance Committee Chair Ron Wyden (D-OR), however, want to make their own mark on the legislation.

5 min read

Mark-to-market is not simple to implement, as it involves new administrative and compliance challenges for taxpayers. Mark-to-market levies tax on phantom income, requiring some taxpayers to engage in some degree of liquidation, ultimately suppressing incentives to save and invest. The limited tax revenues that could result from these proposals are not worth the risk.

5 min read

To tackle problems of homelessness and housing costs, Senator Ron Wyden (D-OR) has released a major tax proposal, the Decent Affordable Safe Housing (DASH) For All Act. Several of Wyden’s proposals are also components of the Biden administration’s infrastructure agenda, with a large focus on tax credits designed to either incentivize new housing or directly reduce rent burdens.

5 min read

Increasing tax compliance is a major part of the Biden administration proposal to raise revenue for physical and social infrastructure. Reducing the tax gap—the difference between taxes owed and taxes paid—is a good way to raise revenue, but it doesn’t come without trade-offs, and it’s important to go about it in the right way.

3 min read

Recent Biden administration proposals rely heavily on revenue from better IRS tax collections to fund spending initiatives. The American Families Plan uses several avenues to reduce the tax gap (or the difference between taxes paid and taxes owed), from increasing the IRS’s tax enforcement budget to improving information technology and expanding reporting requirements.

4 min read

Tackling climate change and shifting the economy towards renewable energy has been a key part of the Biden administration’s agenda. However, this effort must first confront an overly complicated and non-neutral tax code, particularly in how it treats nuclear energy, for the White House to reach its ambitious goals.

6 min read

The arguments for a new surtax on corporate book income misconstrues why there are differences between a corporation’s taxable income and book income.

5 min read

While it makes sense to ensure cryptocurrency transactions are treated similarly to other financial assets, the nature of these requirements as written are potentially unworkable.

3 min read

Return-free filing could reduce compliance costs for many taxpayers, but would only be as good as the system it is administrating.

4 min read

Reducing the tax gap is, on the margin, a good way to raise revenue, but is not without costs. Policymakers should consider compliance costs for law-abiding taxpayers as well as administrative costs for the IRS when evaluating measures to reduce the tax gap.

33 min read

While parts of the U.S. tax code can handle inflation, full expensing of capital investment would be a major improvement along these lines.

5 min readTaxes are once again at the forefront of the public policy debate as legislators grapple with how to fund new infrastructure spending, among other priorities. Our tax tracker helps you stay up-to-date as new tax plans emerge from the Biden administration and Congress.

1 min read