VAT Bases in Europe

2 min readBy:Countries around the world have been introducing various fiscal measures to alleviate the economic distress caused by COVID-19. One measure—among many—has been to provide relief through temporary changes of Value-Added TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. es (VAT), such as delaying payments, speeding up refunds, or reducing rates.

However, the extent to which businesses and consumers will benefit from such relief measures will depend on the current structure of a country’s VAT, including VAT exemption thresholds, standard and reduced VAT rates, and the VAT base. Today’s post will take a closer look at European OECD countries’ VAT bases and how they impact recently proposed and implemented VAT changes.

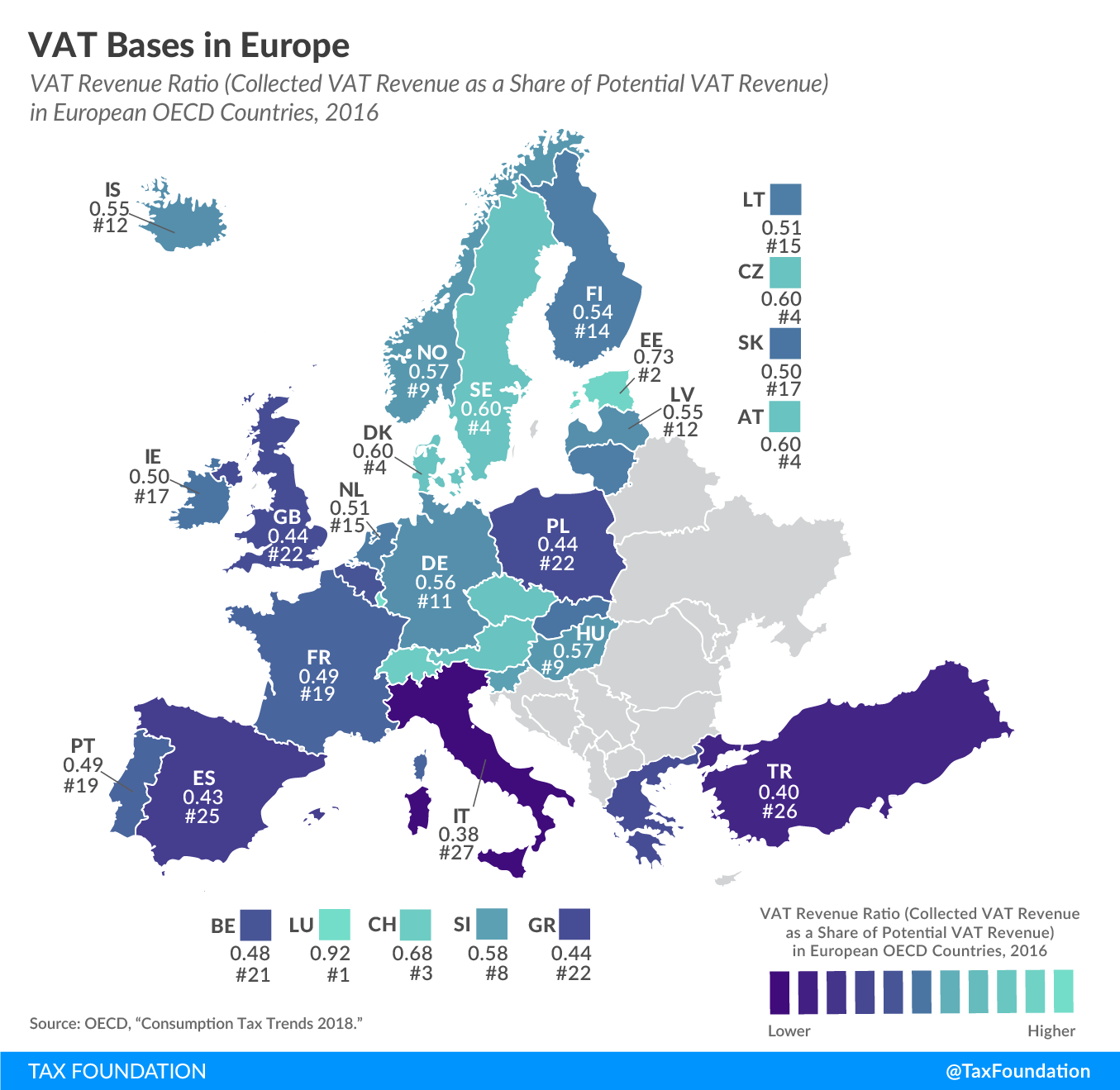

One way to measure a country’s VAT base is the VAT revenue ratio. This ratio looks at the difference between the VAT revenue actually collected and collectable VAT revenue under a VAT that was applied at the standard rate on all final consumption. The difference in actual and potential VAT revenues is due to 1) policy choices to exempt certain goods and services from VAT or tax them at a reduced rate, and 2) lacking VAT compliance.

For example, a VAT revenue ratio of 1 would mean that a country levies its standard VAT rate on all final consumption and there is no VAT evasion or avoidance. In other words, it would be an indicator that there is no revenue loss as a consequence of exemptions and reduced rates, fraud, evasion, and tax planning.

In 2016 (most recent data available), Luxembourg’s VAT revenue ratio was the highest among European OECD countries, at 0.92. Estonia and Switzerland were second and third, at 0.73 and 0.68, respectively. Italy (0.38), Turkey (0.40), and Spain (0.43) had the lowest ratios.

The design of the VAT base plays a deciding factor in who will benefit from VAT relief. Businesses selling goods and services that are exempt from VAT will not benefit from relief such as delayed VAT payments, faster VAT refunds, or reduced VAT rates. For example, many countries exempt food and cultural and sporting services from VAT, sectors that have been hit particularly hard during this crisis. Small businesses that are below the VAT exemption threshold face a similar situation.

In addition, a broad VAT base and thus relatively heavy reliance on VAT revenue can help stabilize total tax revenues during an economic crisis. During the Great RecessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years. , consumption taxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or an income tax where all savings is tax-deductible. revenue—VAT revenue accounts on average for two-thirds of consumption tax revenues in European OECD countries—remained relatively stable while revenue from other types of taxes—such as corporate and individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. es—decreased significantly. This crisis is different as the imposed economic shutdown will likely cause sharp declines in consumption and thus in VAT revenues. However, more reliance on VAT could help revenues recover more quickly once the economy reopens.

An overview of VAT relief and other fiscal measures that countries around the world have implemented during the coronavirus outbreak can be found here.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe