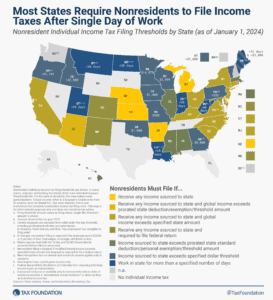

Nonresident Income Tax Filing and Withholding Laws by State, 2026

One area of the tax code in which extreme complexity and low compliance go hand-in-hand—and where reform is desperately needed—is in states’ nonresident individual income tax filing and withholding laws.

9 min read