The Honorable Peter Roskam

2246 Rayburn House Office Building

Washington, DC 20515

Dear Chairman Roskam,

I’m writing to give you a broader perspective on the debate over whether tax reform should prioritize full expensing or a corporate rate cut. One of the supposed demerits of full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. , claims a group in a letter sent to you recently, is that “it would benefit a very particular business operation, only new capital investments.”

It’s puzzling why any group would be against incentivizing new capital investment, especially given the competitive challenges faced by American manufacturing today. Setting aside for a minute the case that these two policies are complementary and should not be pitted against each other, the fact that expensing “only benefits new capital investment” is exactly why it should be the centerpiece of any taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. reform plan.

New investment is what drives economic growth and, just as importantly, boosts worker productivity which, in turn, raises real wages and living standards. The number one priority of tax reform should be to raise the living standards of American families, not cater to the needs of special interests.

To be sure, cutting the corporate tax rate should be a priority because the U.S. has the highest corporate tax rate in the industrialized world, a status which is undermining America’s competitive position in the global economy. However, allowing businesses the ability to immediately expense their capital investments—especially structures and buildings—is the most powerful tax policy lawmakers can use to boost investment, productivity, and wages.

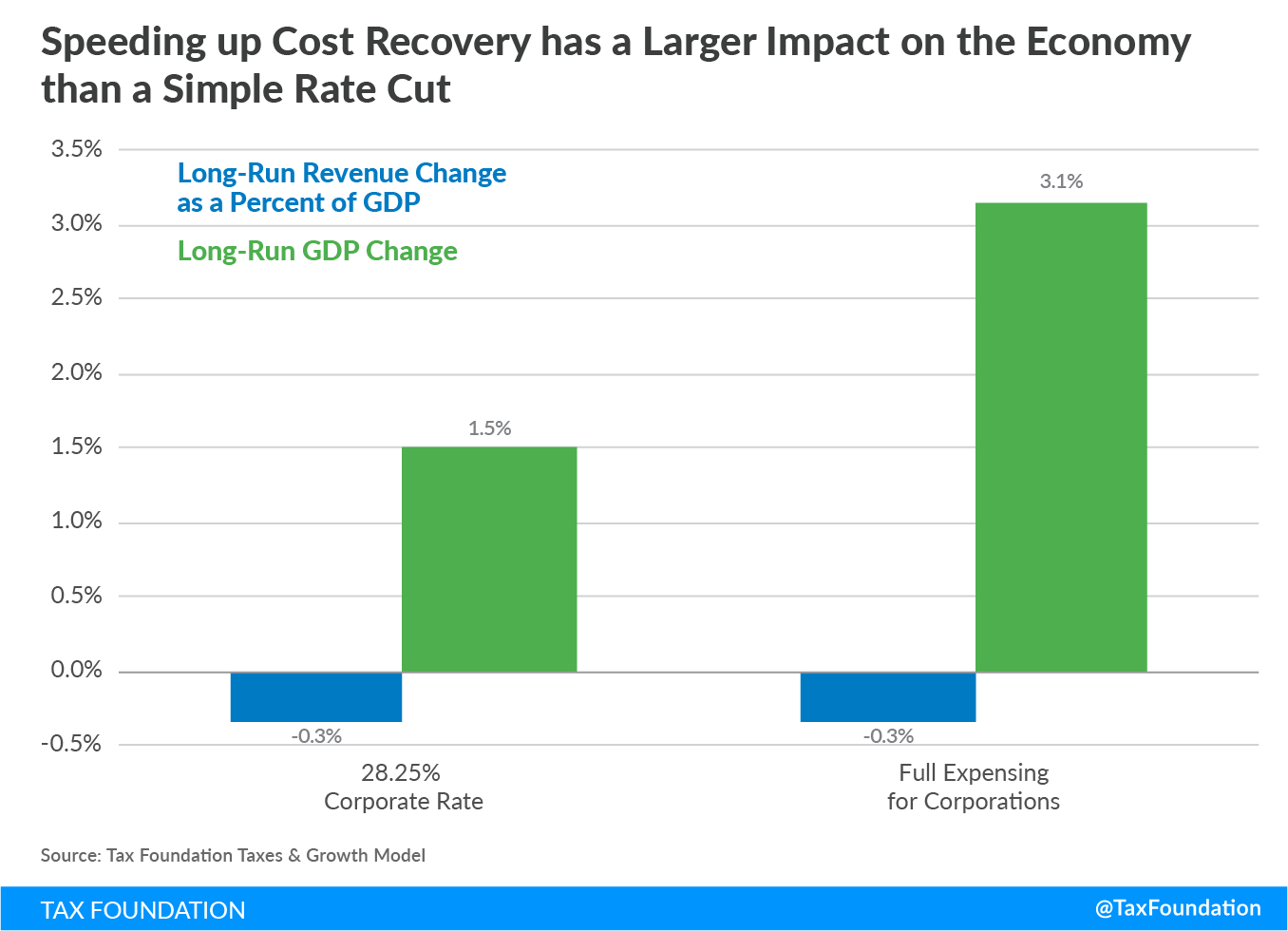

Expensing Has Biggest Bang for the Buck in Lifting GDP

As the chart below indicates, expensing has twice the impact on economic growth than cutting the corporate tax rate. Why is that? Because expensing benefits only those who invest in new capital while cutting the corporate tax rate benefits both new and old capital, thus splitting its impact across the economy.

For example, if I own a factory that makes appliances, a lower corporate will increase the amount of after-tax profit I earn on each toaster, but it will not necessarily incentivize me to produce more toasters. On the other hand, the only way that I can reap the benefits of full expensing is by adding an assembly line or building a factory. Thus, the corporate rate cut initially flows to my bottom line, whereas the new capital investment immediately benefits my workers and new employees.

Expensing Boosts After-Tax Incomes More than Rate Cuts

The nearby table, based on Tax Foundation modeling, shows how expensing has much more of an impact on boosting after-tax incomes of families compared to the effects of a lower corporate tax rate or cutting individual tax rates. Expensing increases the after-tax incomes of households by an average of 5.3 percent, compared to an average increase of 4 percent from cutting the corporate tax rate, and an average increase of 3.6 percent from consolidating individual tax brackets. These gains represent the combination of wage growth, economic growth, and the dollar value of the tax cuts.

| Income Group | Consolidate Individual Brackets to 10%, 25%, 35% | Lower the Corporate Rate to 15% | Allow Full Expensing of Capital Investments |

|---|---|---|---|

| 0% to 20% | 1.2% | 3.9% | 4.9% |

| 20% to 40% | 1.2% | 3.9% | 4.9% |

| 40% to 60% | 2.4% | 4.3% | 5.3% |

| 60% to 80% | 3.5% | 4.1% | 5.1% |

| 80% to 100% | 4.4% | 4.0% | 5.4% |

| 90% to 100% | 4.8% | 4.0% | 5.6% |

| 99% to 100% | 6.2% | 4.1% | 6.3% |

| Total | 3.6% | 4.0% | 5.3% |

Expensing Saves More than $23 Billion in Compliance Costs

Lastly, a move to full expensing accomplishes something that no rate cut can: it eliminates pages from the tax code, thus saving taxpayers time and money. American businesses today spend more than 448 million hours each year complying with the Byzantine depreciation and amortization schedules, at an estimated cost of over $23 billion annually. Moving to full expensing eliminates the need for these complicated schedules, thus saving businesses the $23 billion in compliances costs, which is an added benefit to the impact the policy has on boosting wages and economic growth.

Chairman Roskam, it would be a tragic mistake to pit full expensing against a corporate rate cut. Each performs an important function in any pro-growth tax reform plan:

- Corporate rate cuts improve U.S. competitiveness and are pro-growth.

- Expensing adds twice the growth, increases productivity, boosts real family incomes, and simplifies the tax code.

- Combined, they are a powerful engine for improving U.S. competitiveness and raising living standards for all Americans.

If lawmakers’ aim is a tax reform plan that maximizes economic growth while boosting real incomes, they should pair expensing with a low corporate rate. If you have any questions about this, please don’t hesitate to contact me or my colleagues at the Tax Foundation.

Sincerely,

Scott A. Hodge

President

Cc: Members, House Ways and Means Committee

Share this article