The Fiscal Consequences of Increased German Spending

5 min readBy:On 18 March 2025, the German Bundestag passed a historic spending bill. The €1 trillion package includes significant investments in defence and infrastructure with €500 billion allocated to a special fund for infrastructure development and €100 billion designated for climate-related investments.

Now, the question for policymakers is how to pay for this increase in funding and to what extent this shift in priorities will impact long-term economic growth across the EU. Without aligning fiscal discipline with pro-growth taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. policies, Germany and the EU risk high deficits, mounting debt, and sustained inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. .

The Debt Brake and Economic Growth

The additional spending required an exemption from Germany’s fiscal rules known as the debt brake. The economic impacts of these rules on growth and investment have longed been debated by economists. While the increased spending could stimulate short-term economic growth, its long-term impact on both Germany’s economy and the broader eurozone remains uncertain.

For example, rising government interest burdens and the potential for crowding out private investments could hinder long-term economic growth. Additionally, reshuffling and repurposing of the new public funds could lead to political abuse with critical spending areas potentially being manipulated.

But the impact is not confined to Germany. The broader European economy is likely to experience negative spillovers, with neighboring countries facing rising interest rates due to Germany’s fiscal shift. This could result in either inflationary pressures or fiscal crises, as the increased debt load limits the financial capacity of both Germany and its European neighbors to manage long-term challenges.

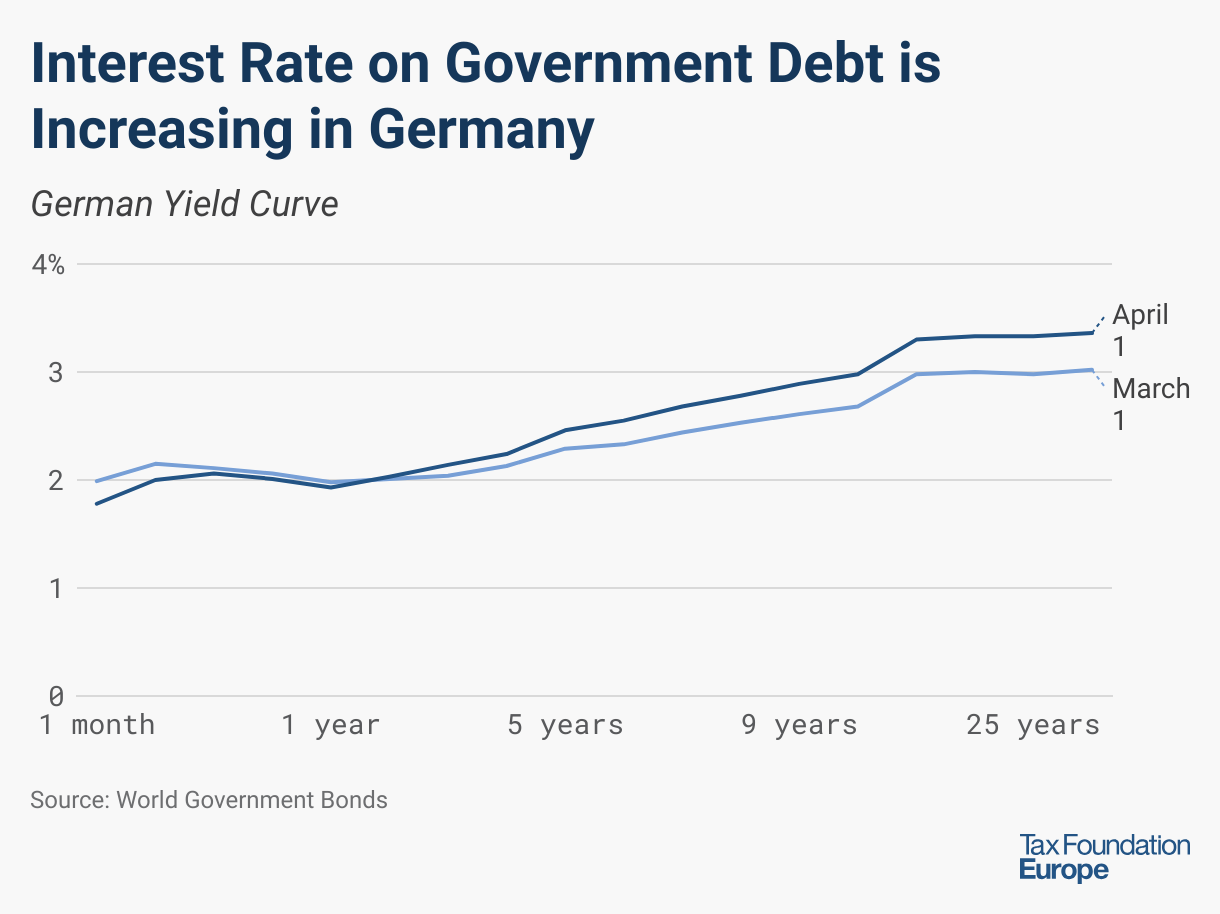

Consequences for Germany

The immediate impact of the new programme on the German yield curve was notable: German 10-year bonds suffered their worst weekly sell-off since the 1990s, with yields increasing by about 0.3 percentage points. While some researchers have mentioned that this change should not be seen as a fiscal threat for investors but rather as positive for growth expectations, there are serious doubts about this view.

First, the newly created fiscal space could allow for the reallocation of funds for other purposes. This would only further postpone important tax reforms related to Germany’s ageing society.

Second, the refinancing of public debt and likely debt-financed military spending could threaten the German purse in the future.

Thirdly, higher yields will directly hit those in need of financing as mortgage rates are typically directly linked to German Bund yields. Often, younger generations who want to buy or build their own homes are most affected.

Germany’s fiscal strategy raises questions not only about public debt and spending, but also about the role of taxation in maintaining fiscal stability. Germany’s tax system is already characterised by high income tax rates, significant social security contributions, and a solidarity surcharge that still applies to high earners. Germany’s tax wedgeBroadly speaking, a tax wedge is the difference between the pre-tax price or return and after-tax price or return. For labor income, it is the difference between the total labor costs to the employer and the corresponding net take-home pay of the employee. on labor is currently the second highest in the OECD.

However, the debate on tax reform is likely to intensify as fiscal pressures increase due to rising defence spending, infrastructure investment, and demographic challenges.

Most likely, the discussions will be about broadening the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. base and increasing VAT rates. While the previous German government supported more generous tax deductions for fixed assets to foster growth, the current coalition agreement, despite mentioning targeted incentives such as super-depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. for climate and digital investments and a step-wise reduction of the corporate tax rate beginning in 2028, suggests that broader tax reform of this kind is becoming increasingly unrealistic.

Given the poor economic performance of recent years —GDP per capita dropped in 2023 (-1.1 percent) as well as in 2024 (-0.5 percent)—such moves are likely to further decrease business and consumer sentiment, and therefore, the economic outlook.

Consequences for the EU

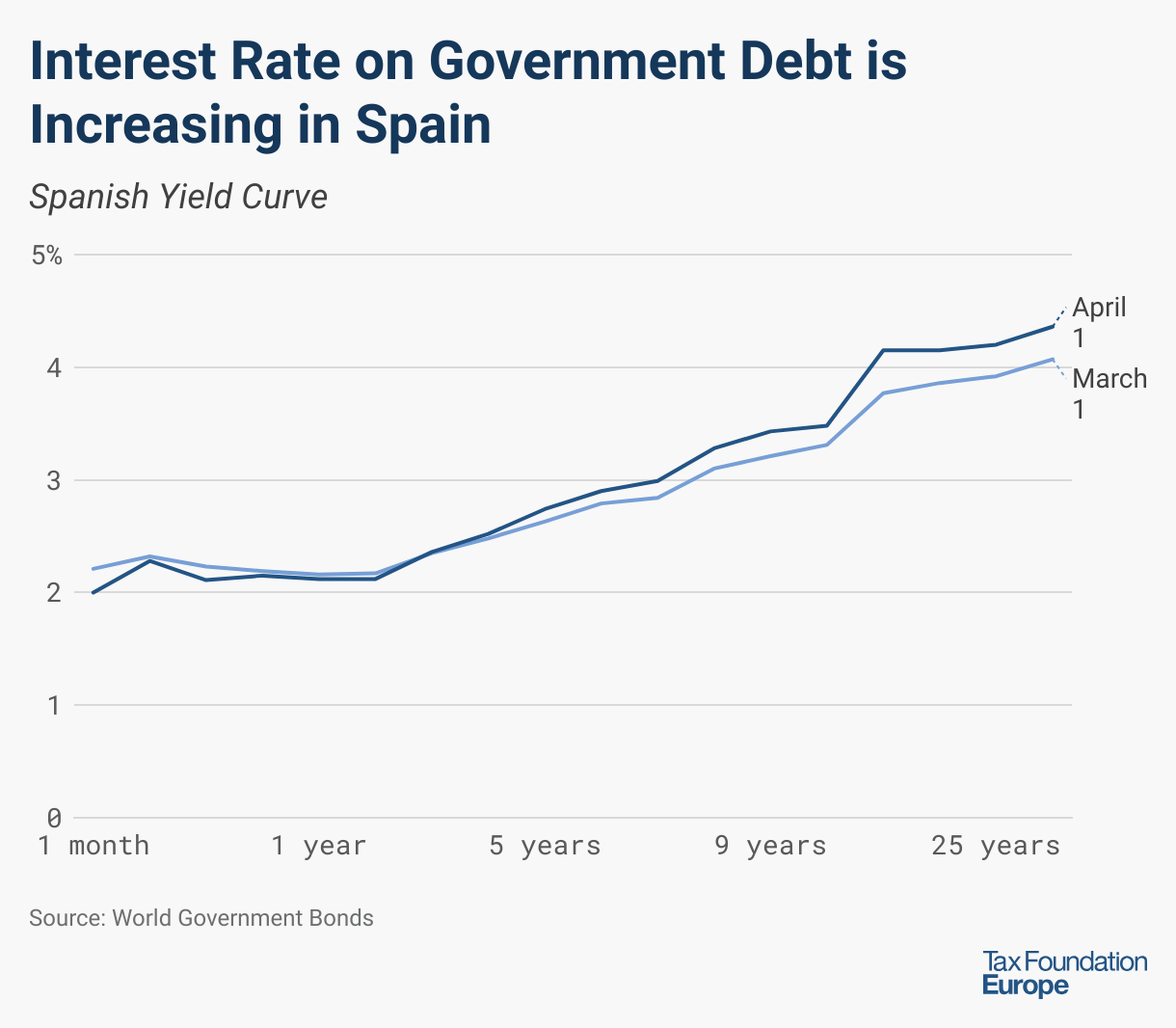

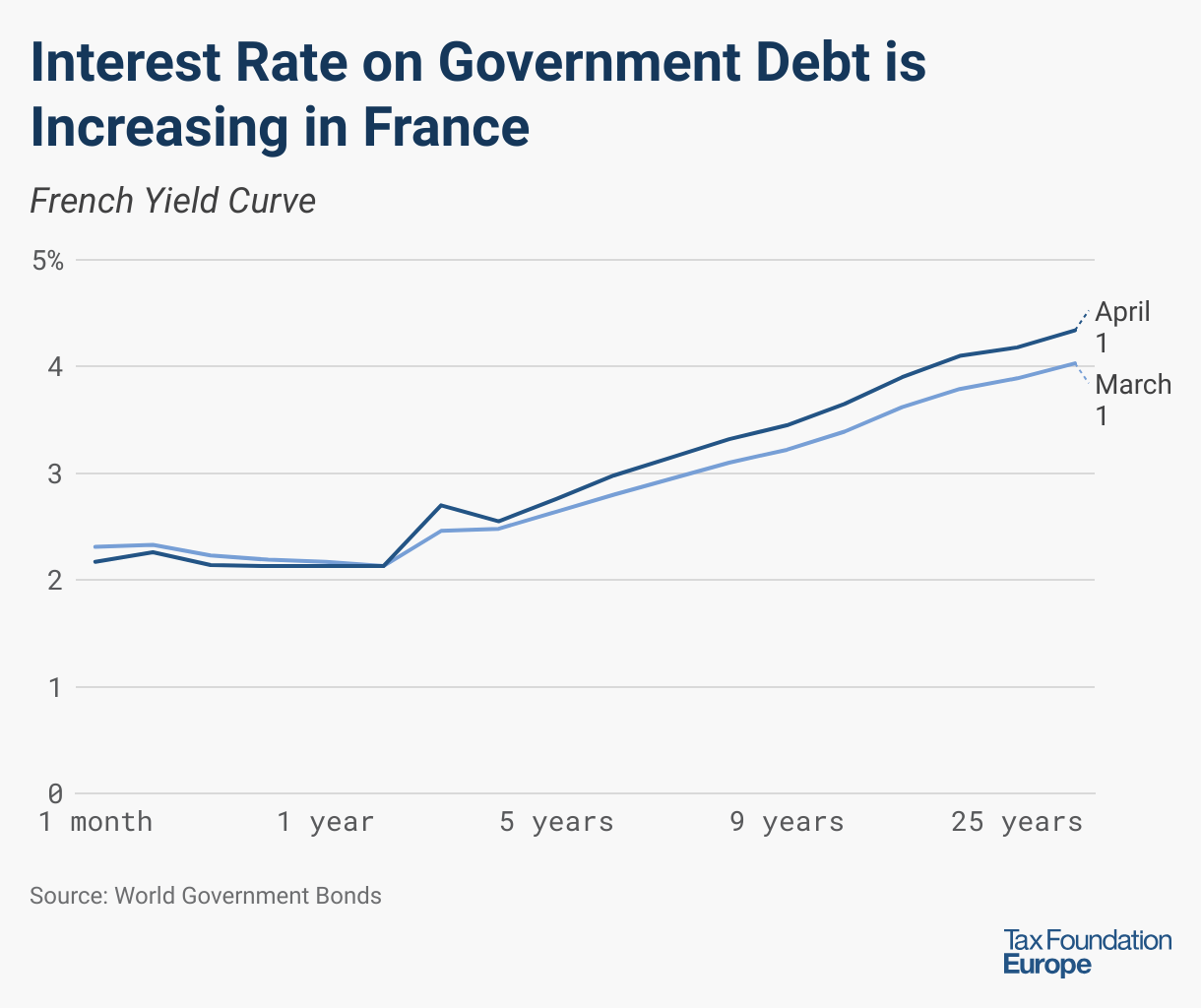

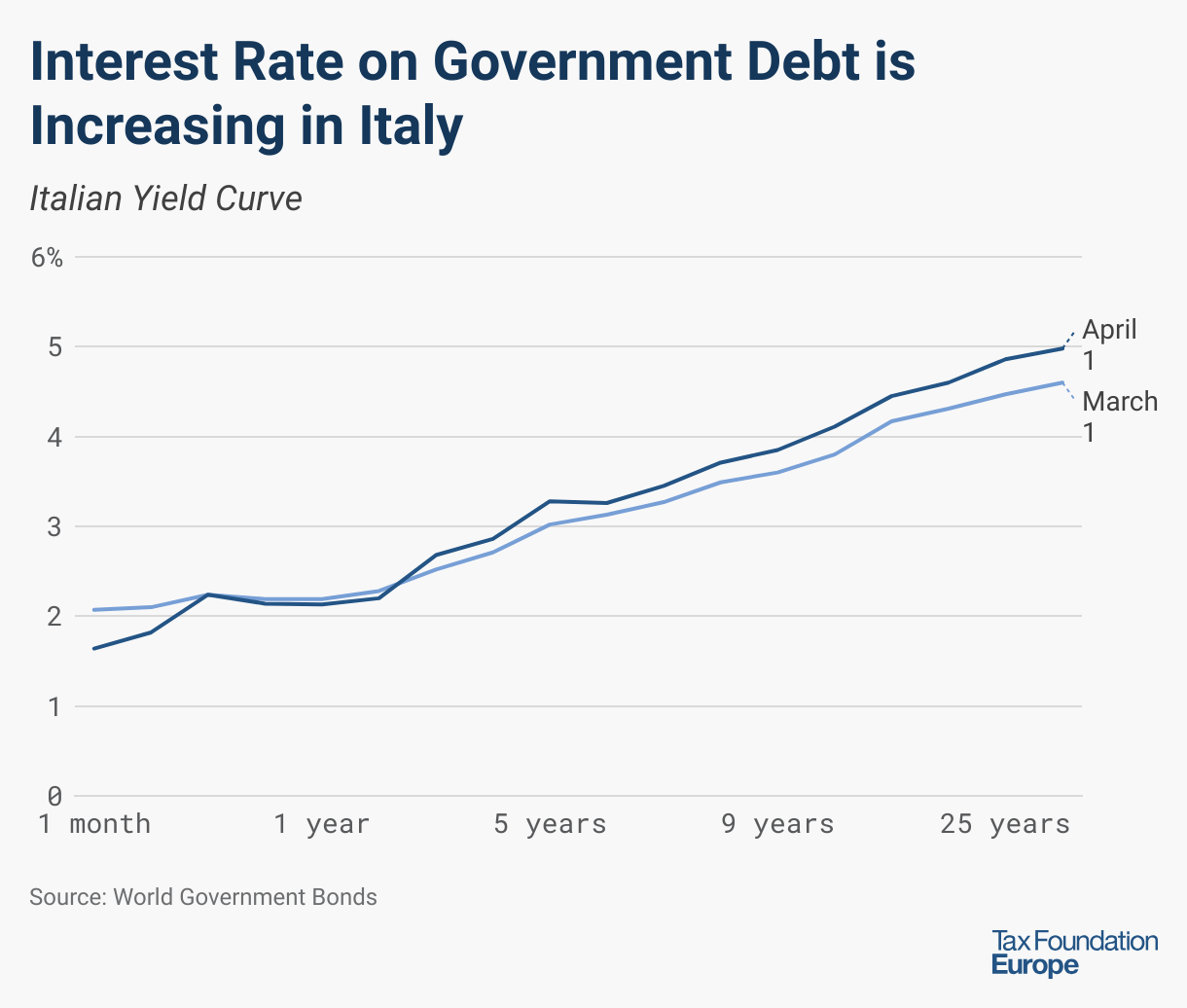

Similarly, at the EU level, the change in the European safe haven has direct consequences for all Member States. Following the announcement, German yields surged while yields across other European countries increased. This is because the German yield is recognised as the minimum interest rate at EU level.

Other European governments will likely feel more fiscal pressure from the German-induced rise in interest rates that will make domestic public spending more difficult. For example, military financing at the national level will become even more complicated for those countries that are highly indebted. This brings into question the possibility of a common EU-wide financing programme. Additionally, the European Commission has temporarily exempted defense spending from the EU’s fiscal rules.

Rather than pushing Member States to make structural reforms, including pro-growth reforms and tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. expansions, to accommodate increased spending, the exemption simply removes the Commission’s enforcement mechanism. It does not change the economic reality of indebtedness across Member States.

Worse, it allows policymakers to redefine other public spending objectives such as climate change initiatives as ”defense spending” to avoid penalties under the EU’s fiscal rules. As an example, Spain has advocated for a broader definition of defense spending, proposing that areas like cybersecurity, anti-terrorism, and even climate change initiatives be classified under defense to better reflect modern security challenges. This approach risks further weakening fiscal constraints, potentially encouraging deficit spending, and delaying much-needed structural reforms across Europe.

As a consequence, the European Central Bank (ECB) faces a credibility test in light of Germany’s new fiscal direction. While major European economies such as Germany, Austria, or Netherlands are grappling with sluggish growth expectations and rising inflation, Southern European economies appear more resilient, as Spain (2.3 percent) and Greece (2.3 percent) are expected to grow on a substantial higher level in 2025. The combination of increased government spending and rising yield curves across Europe will put the ECB in a difficult position: cutting interest rates could prevent a fiscal crisis but would contradict its price stability mandate.

What Is Really Needed?

Without a clear dedication to growth-oriented fiscal reforms, inflationary pressures in the EU will likely persist. In contrast to taxation, inflation can be imposed without legislation. If Germany and the EU fail to align fiscal discipline with sustainable, growth enhancing tax policies, they risk falling into a cycle of high deficits, rising debt costs, and prolonged inflation.

What was intended as a stabilizing measure may instead create enduring structural challenges. In trying to secure Germany’s future, a new risk was introduced that will shape Europe’s financial landscape for the foreseeable future.

Share this article