In pursuit of revenue neutrality, the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. reform debate has taken the shape of broad bases and lower rates. The Senate has mentioned their intention to approach tax reform from a “blank slate” perspective.

Congress is right that the tax system needs to change. The current system “is a serious drag on economic growth. Its anti-growth effects, which are inadvertent but powerful, hurt Americans' productivity and incomes, reduce their ability to compete in an increasingly global marketplace, and diminish their future opportunities.”

But this week my colleague Michael Schuyler released a report that found that the “blank slate” approach to tax reform could have damaging consequences for growth.

This is because the current tax code poorly defines the income tax base.

While there is junk in the tax code, about 60 percent (or over $700 billion) of tax expenditures help make the tax code more neutral (i.e. less biased against savings and investment). The tax expenditures that help mitigate the double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. on savings and investment include the exclusion for retirement savings, business depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and disco rules, and the different rate on capital gains.

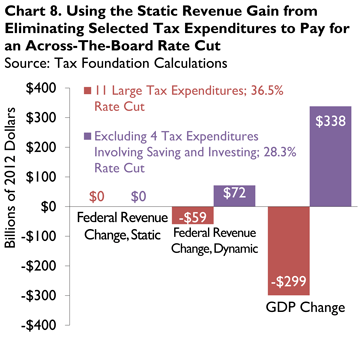

This means that if Congress were to eliminate 11 of the largest tax expenditures through tax reform and use the additional revenue to cut the top tax rate to 25.1 percent, we would still see a decrease in GDP by $299 billion because of the way the “blank slate” would damage savings and investment.

Instead, if we were to parse out the tax expenditures in the code that don’t prevent the double taxation of savings and investment (the state and local tax deduction, charitable deduction, etc.), then trade those for a cut in the tax rate, we could see some actual growth.

The elimination of the seven of the eleven provisions that don’t help define a neutral tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. would provide enough revenue to cut the tax rates by 28.3 percent across the board; dropping the 10 percent rate to 7.2 percent, the 25 percent rate to 17.9 percent, and the 39.6 percent rate to 28.4 percent. Trading those provisions for a rate cut would raise GDP by $338 billion.

In tax reform, it’s not just about the rate. The base has to be right, too.

To read the full report, click here. For our previous studies on the economic effect of the blank slate, click here.

Share this article

{kind=link}

{kind=link}