Reliance on Corporate Income Tax Revenue in Europe

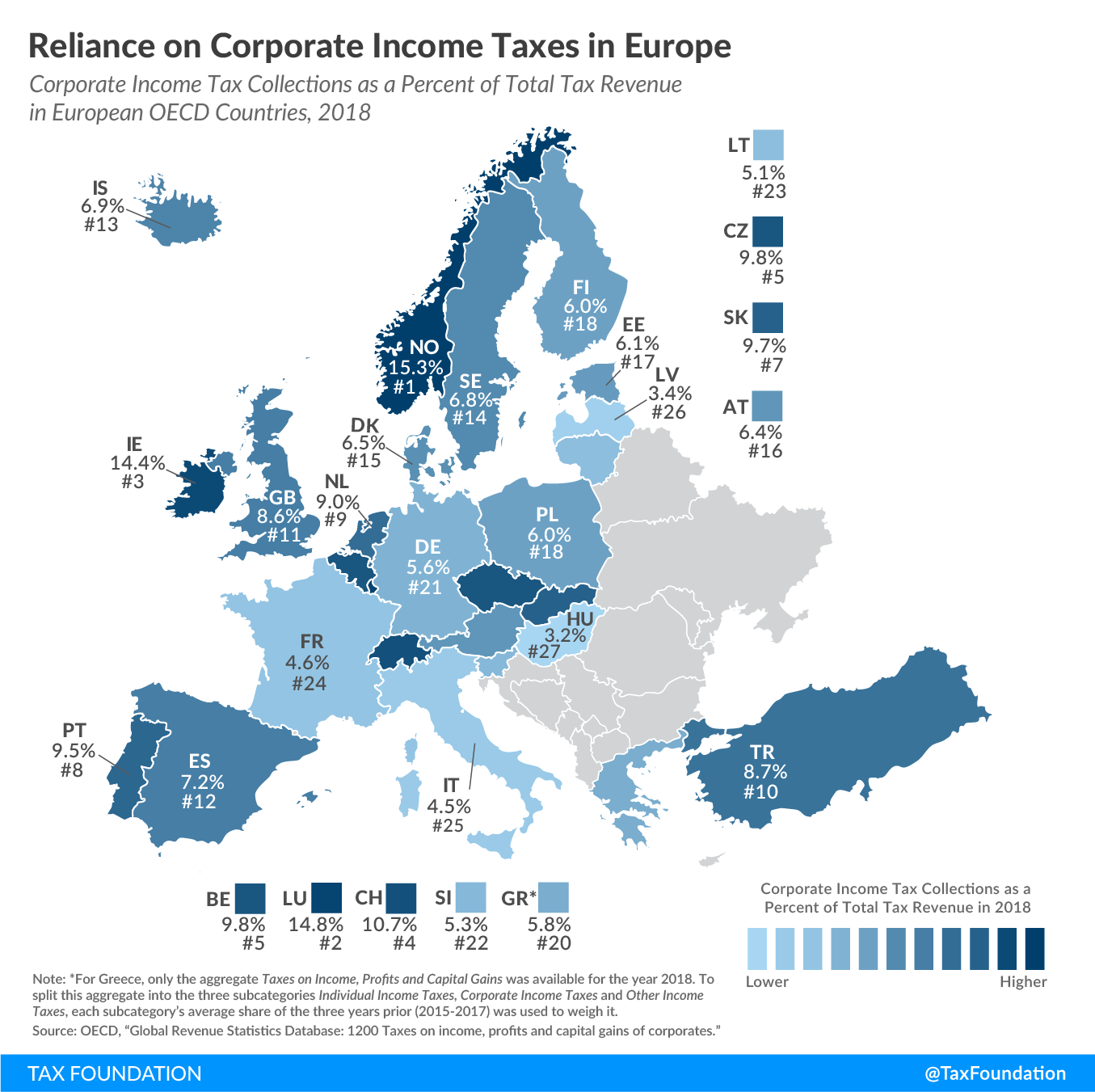

1 min readBy:A recent report on taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. revenue sources shows the extent to which OECD countries rely on different tax types. Today’s map looks at the corporate income tax, which, compared to individual taxes, social insurance taxes, and consumption taxes, generates a relatively small share of tax revenue in Europe. In 2018—the most recent year for which data is available—the European countries covered in today’s map raised on average 7.8 percent of total tax revenue from corporate income taxes.

In 2018, Norway relied the most on its corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax., at 15.3 percent of total tax revenue, followed by Luxembourg (14.8 percent) and Ireland (14.4 percent). Hungary (3.2 percent), Latvia (3.4 percent), and Italy (4.5 percent) relied the least on the corporate income tax.

Despite declining corporate income tax rates over the last 40 years in Europe (and other parts of the world), average revenue from corporate income taxes as a share of total tax revenue has not changed significantly compared to 1990. Many countries have been weakening their treatment of capital investment, which has led to broader tax bases and helped to offset the loss in corporate income tax revenue resulting from lower tax rates.

Corporate income taxes are a direct tax on corporate profits, and fluctuating business cycles can significantly impact these profits generated by businesses. This can make the corporate income tax a relatively volatile source of revenue.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

SubscribeAbout the Author

Elke Asen

Policy Analyst

Elke Asen was a Policy Analyst with the Tax Foundation’s Center for Global Tax Policy, focusing on international tax issues and tax policy in Europe. Prior to joining the Tax Foundation, Elke interned with the EU Delegation in Washington, D.C., the German Development Agency, and a social startup in Munich, Germany. She holds a BS in Economics from Ludwig Maximilian University of Munich.