Key Findings

- Last-in, First-out (LIFO) and First-in, First-out (FIFO) are two methods of inventory accounting used for both financial accounting and taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. purposes.

- Both LIFO and FIFO rely on the accounting principle of deducting costs from income when goods are sold.

- This principle often comes into conflict with the economic principle of deducting costs when incurred, as inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin does not reduce the value of the deduction in real terms.

- However, LIFO comes close to matching the economic ideal while still remaining true to the accounting principle.

- Repealing LIFO would disincentivize inventory investment, hampering efforts to make U.S. supply chains more resilient.

- Repealing LIFO would also reduce economic growth and penalize industries that typically keep more inventory on hand.

Introduction

The tax treatment of inventories may be an obscure policy, but it is still significant. Repealing Last-In, First-Out accounting appeared in many Obama administration budget proposals and was included in the Dave Camp tax reform package in 2014. Today, thanks to several factors such as rising inflation, high deficits, supply chain issues, and industry-specific concerns, LIFO has re-entered the policy discussion. While repealing LIFO might seem like an inconsequential way to raise revenue, it would penalize investment in inventory and move the tax system away from neutrality towards investment.

What Are LIFO and FIFO?

The LIFO inventory method allows companies to deduct the cost of inventory at the price of the most recently acquired items and assumes that the last inventory purchased is the first to be sold.[1] The FIFO inventory method, by contrast, allows companies to deduct the cost of inventory at the price of the oldest acquired items and assumes the first inventory purchased is the first to be sold.

These methods can affect companies differently. Consider companies in three loose categories: manufacturers, merchandising firms, and service firms. Manufacturers turn raw materials and labor into finished products and have several different types of inventories—raw materials, works in progress, and finished goods. Merchandising firms, meanwhile, purchase finished physical goods from a supplier and then sell them to customers; they only have finished goods inventories.[2] Importantly, there are usually several layers of merchandising firms in the supply chain. There are wholesalers and distributors, which purchase goods from manufacturers and sell them to retailers, who sell them to the final customer. There may be several distributors and wholesalers between the manufacturer and the retailer. Lastly, services firms sell services, not physical goods, and thus likely have no inventory.

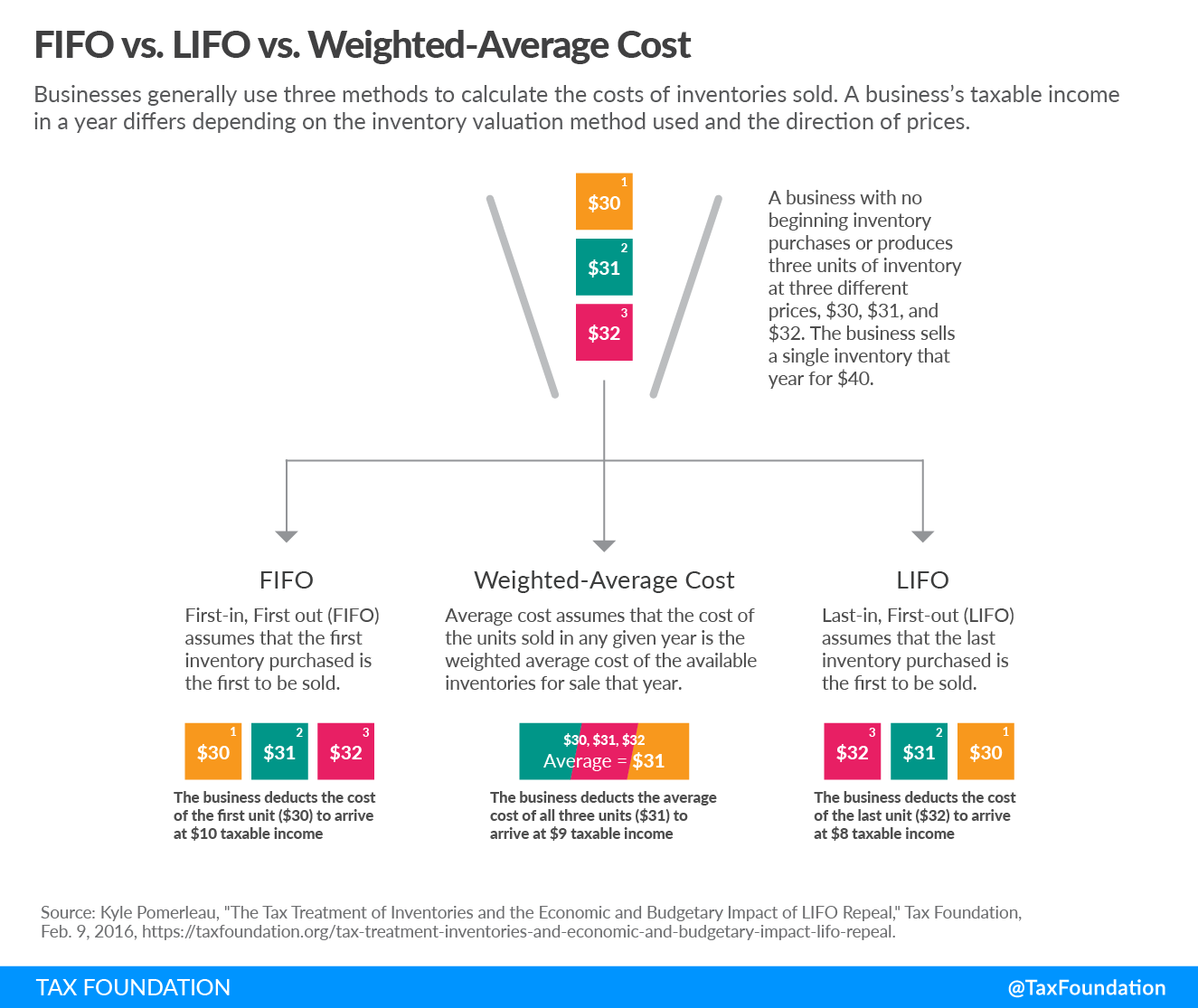

To demonstrate the differing effects of LIFO and FIFO, consider a company with no beginning inventory that purchases three units of inventory over the course of the year: one for $30 in January, one for $31 in June, and one for $32 in November. The firm then sells one unit for $40 in December. In this simplified example, assume inventory is the company’s only cost.

If the company uses the FIFO inventory accounting method, it would deduct the cost of the first unit of inventory purchased, namely the unit purchased for $30 in January. Subtract $30 in costs from the $40 in revenue, and the company has $10 in income. Meanwhile, under the LIFO inventory accounting method, it would deduct the cost of the last unit of inventory purchased, namely the unit purchased for $32 in November. Subtract $32 in costs from $40 in revenue, and the company has $8 in income.[3]

There are several other methods of inventory accounting, the most common being weighted-average cost. When a unit of inventory is sold, companies can deduct the weighted-average cost of every unit of inventory held. In the example case here, that would mean the company would deduct $31 in inventory costs when they sell a unit in December, leading to $9 in income.

The Two Philosophies of Taxes and Income

To understand the policy conversation about LIFO and FIFO, one must understand two main philosophies of calculating income: the pure income approach and the cash flow approach.

The income approach focuses on matching deductions for costs with the revenues they generate. For example, if a farm invests in a new tractor that it will use for 10 years, it should spread the deductions for that tractor out over the next 10 years. When applying this principle to inventories, companies should deduct the cost of a unit of inventory when it is sold.

The cash flow approach suggests companies should deduct their costs right when those costs are incurred. In the case of the farm investing in a new combine, it should deduct the full cost of the combine immediately. When applying this principle to inventories, companies should deduct the cost of a unit of inventory when it is acquired.

For accountants and financial analysts, the income (or book incomeBook income is the amount of income corporations publicly report on their financial statements to shareholders. It provides a picture of a firm’s financial performance and follows Generally Accepted Accounting Practices (GAAP). While it is a useful measure for assessing financial performance, it is not useful for assessing tax liability.) approach makes sense for determining the financial health of a company—this approach shows that, for instance, a decline in cash flow thanks to major investment decisions does not mean that the company is “losing money,” as those investment costs can get spread out. Meanwhile, the cash flow-based approach makes the most sense from a tax economics perspective because deducting investment costs when they are incurred means a company can deduct the full real cost, without inflation and the time value of money eating away at the deduction’s value (which occurs when deductions are spread over several years).[4]

For some issues, companies can use one set of rules to calculate financial income and another set of rules to calculate taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. —which also makes sense, as they measure different things.[5] But in the case of LIFO and FIFO, both systems are, at least on paper, based on the book income approach. Both systems have companies deduct the cost of a unit of inventory when it is sold, not when it is acquired. Additionally, companies must use the same system for both financial and taxable income.

Why LIFO Matters

Both LIFO and FIFO are grounded in the accounting principle of deducting costs when goods are sold rather than when they are acquired. However, LIFO comes closer in effect, although not in design, to deducting inventories when they are acquired, and thus reduces the tax penalty on inventory investment.

Consider the example company cited earlier that had three units of inventory, but now it sells one for $40 in December. Immediately after the sale, it buys a new unit of inventory (to keep inventory levels constant, as many companies do). However, prices have risen slightly, as its supplier now charges $33 per unit, as opposed to $32 in December (and $31 and $30 earlier in the year).

If the company was able to fully expense inventories, it would deduct $33 for the unit of inventory acquired in December. However, because it is using LIFO, it deducts the last-in unit of inventory when it recorded the sale, the $32 unit of inventory acquired in November. Under FIFO, the company would have to deduct its oldest unit of inventory—the one acquired for $30 in January. Ultimately, the deduction under LIFO comes closest to matching the cost of acquiring a replacement unit of inventory.

Generally, prices rise across the economy over time, so the last-in unit of inventory is usually more expensive than the first-in unit of inventory. Under those circumstances, LIFO allows companies to deduct a larger share of their inventory costs than FIFO. That translates to both a lower reported financial income and a lower taxable income, leading to a lower tax liability. The higher inflation is, the larger the penalty under FIFO.[6] And that penalty raises the cost of capital for inventory purchases, thus reducing investment.[7]

Consider another illustration showing the effects of LIFO under rising prices. A company makes a sale at the end of the year for $250. The oldest, or first-in, unit of inventory, bought at the beginning of January that year, cost $200. The last-in unit of inventory was purchased for $209 in November, a month earlier. And the day the company makes that sale in December, they purchase a new unit of inventory for $210. Under FIFO, the effective tax rate is 26.3%, compared to LIFO at 21.5% and expensing at 21% (Table 1).

The difference between the methods becomes wider with higher price increases. For example, if the last-in inventory increases to $218 and December’s new unit increases to $220, then the effective tax rates are 35% for FIFO, 22.4% for LIFO, and 21% for expensing (Table 2). Ultimately, LIFO gets close to expensing treatment economically, while still being consistent with the notion of matching deductions to goods sold.

| FIFO | LIFO | Expensing | |

|---|---|---|---|

| Revenue | $250 | $250 | $250 |

| Inventory Deduction | $200 | $209 | $210 |

| Taxable Income | $50 | $41 | $40 |

| Tax Owed | $10.5 | $8.61 | $8.4 |

| Effective Tax Rate | 26.3% | 21.5% | 21.0% |

|

Source: Author’s calculations. |

|||

| FIFO | LIFO | Expensing | |

|---|---|---|---|

| Revenue | $250 | $250 | $250 |

| Inventory Deduction | $200 | $218 | $220 |

| Taxable Income | $50 | $32 | $30 |

| Tax Owed | $10.5 | $6.72 | $6.3 |

| Effective Tax Rate | 35.0% | 22.4% | 21.0% |

| Source: Author’s calculations. | |||

LIFO Usage

One main factor that determines whether a company chooses LIFO or FIFO is inventory turnover.[8] Inventory turnover is the ratio of a business’s cost of goods sold (COGS) to its average inventory on hand over a particular period. In practice, this is usually expressed annually, indicating the number of times inventory fully turns over in a year. Financial analysts often use this metric to compare the efficiency of companies within the same industries, but inventory turnover varies wildly by industry.[9]

Companies with very fast inventory turnover use LIFO less than companies with slower inventory turnover. For example, a store that exclusively sells perishable fresh produce must replace its inventory frequently over the course of a year. There may only be days between when the oldest and most recent units of inventory are acquired—likely meaning a minimal difference in price. In those cases, the tax benefits of LIFO are relatively limited.

On the other hand, companies that deal in nonperishable and durable goods benefit more from LIFO provisions, and as such use the accounting method more.[10] This can lead to the perception that the provision is a subsidy for these industries.[11] However, the fact that some industries use LIFO more frequently merely reflects their different structure and greater reliance on inventories.

Consider an unobjectionable component of the corporate tax code: the deductibility of wages and salaries. Some companies are more labor-intensive than others and thus benefit more from the ability to deduct salary costs. That does not mean the deduction for wages and salaries is a subsidy for labor-intensive firms. It just reflects that labor costs are proportionately larger for some businesses than others. The same dynamic exists in the context of inventories—some industries and firms are more inventory-intensive and thus benefit more from the ability to deduct inventory costs.

There is some evidence that LIFO usage has declined in recent years.[12] The relatively low and stable inflation of the 2010s also meant LIFO provided a smaller advantage. With inflation high again, LIFO may become the preferred choice for more businesses.[13]

| Economic Effects of Repealing LIFO | |

|---|---|

| GNP | -0.02% |

| Capital Stock | -0.04% |

| Wage Rate | -0.02% |

| 10-Year Conventional Revenue | +$42.4 Billion |

| 10-Year Dynamic Revenue | +$37.9 Billion |

| Full-Time Equivalent Jobs | -6,000 |

| Source: Tax Foundation Taxes and Growth Model, September 2022. | |

| 10-Year Revenue Effects of Repealing LIFO (in billions) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2023-2032 | |

| Static | $13.5 | $13.5 | $7.3 | $1.1 | $1.1 | $1.1 | $1.2 | $1.2 | $1.2 | $1.2 | $42.4 |

| Dynamic | $13.4 | $13.3 | $7.1 | $0.8 | $0.7 | $0.6 | $0.6 | $0.5 | $0.5 | $0.4 | $37.9 |

| Source: Tax Foundation Taxes and Growth Model, September 2022. | |||||||||||

By slightly raising taxes on investment in inventory, repealing LIFO would reduce economic growth, wages, and the capital stock, while costing about 6,000 full-time equivalent jobs. Though it would also raise revenue—around $42 billion over the next decade on a conventional basis, and just under $38 billion on a dynamic basis—it would not exceed the costs.

Notably, the vast majority of the revenue generated from eliminating LIFO is concentrated in the first few years of the budget window. This is because getting rid of LIFO involves taxing companies’ LIFO reserves: the accumulated benefit of LIFO deductions going back several years. After this point, the revenue impact is negligible, especially after considering the economic effects. The reduction in long-run GDP of 0.02 percent may sound small, but it translates to $4.35 billion in lost output—greater than the amount of revenue generated in later years, especially on a dynamic basis.

Retroactive Taxation on LIFO Reserves

Proponents of taxing LIFO reserves argue it is efficient because it is retroactive and ergo does not change future incentives to work or invest. But repealing LIFO does not just tax accumulated LIFO reserves—it will change incentives for future inventory investments.

Furthermore, not all retroactive taxation is sound policy. For example, if Congress enacted a one-time tax of 5 percent on everyone’s 2004 income, that would be a retroactive tax, and would not (hypothetically) change expected future returns to work or investment, but it is not tied to any ability to pay today. LIFO reserves are not a pile of cash somewhere; they reflect historical, small benefits of LIFO summed up over a long period of time. Taxing these “reserves” that only exist as an accounting identity would be a massive tax increase on a handful of industries and companies, particularly in energy and manufacturing.[14]

Inventory Investment and Supply Chain Resiliency

Supply chain disruptions during the pandemic challenged the popular business practice of just-in-time inventory management.[15] When conditions are normal, it makes sense for businesses to keep as little inventory on hand as possible—a unit of inventory sitting on a shelf means it is not being sold. That’s why inventory turnover is often used as a measure of managerial efficiency. However, when supply chains break down, the relatively sparse inventory stock runs out quickly, leading to a freeze in business activity and lost revenue.[16] As a recent Federal Reserve working paper found, just-in-time inventory practices raise firm value by 1.3 percent, while forcing a 15 percent larger reduction in output in response to a sudden supply shock.[17]

Early studies of the economic shock of the COVID-19 pandemic support this common-sense conclusion. A study of French firms reliant on Chinese-manufactured inputs found that firms with higher inventories were able to absorb the initial pandemic shock better.[18] Eliminating the option to use LIFO would make these problems worse and create a further tax penalty for holding additional inventory, thus making supply chains less resilient.[19]

To be fair, marginally improving the tax treatment of inventories would not suddenly make the U.S. economy invulnerable to major global supply shocks. There are other resilience policies to consider. Diversified supply chains, where firms have both domestic suppliers and a mix of foreign suppliers from several countries, have been more resilient than supply chains reliant on one major supplier (independent of whether that supplier is located domestically or abroad).[20] And some shocks are too big for marginally deeper inventories to prevent work stoppages. But maintaining LIFO would at least prevent further harm to supply chains.

Semiconductors are a useful example. These inputs for many major industries were pinched in two ways. The pandemic caused interruptions to chipmaker operations, reducing supply, while at the same time lockdowns and other measures to keep people at home spurred an increase in demand for consumer electronics.[21] These factors, combined with the duration of the production process for manufacturing a computer chip, helped contribute to the historically high inflation of the past year and a half.[22]

Some companies were better prepared than others. As Massachusetts Institute of Technology professor Yossi Sheffi wrote recently, Toyota was well-prepared. Toyota is famously the pioneer of lean, just-in-time inventory management, but after the 2011 tsunami disrupted the Japanese automaker’s production, management concluded that the firm should keep a deeper stockpile of semiconductors on hand.[23] Initially, the deeper stockpile served the firm well, as they were able to maintain production levels for longer than some of their competitors. But eventually, those supplies ran out, and Toyota too had to reduce production.[24]

For context, the U.S. Commerce Department released a report in January 2022 finding that companies that use semiconductors as an input kept a median of fewer than five days’ worth of semiconductors in inventory, down from around 40 days’ worth of semiconductor inventory in 2019.[25] Meanwhile, it can take from 18 to 26 weeks for a customer’s order for a new semiconductor to be fulfilled, depending on the complexity of the chip, and that does not take into account the time it takes to ramp up production (either through increasing utilization of existing production facilities or building new ones).[26]

LIFO treatment of inventories is not a solution to supply chain difficulties. However, repealing the provision would further penalize inventory investment and could make these problems worse. Full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. for inventories (in other words, moving to deducting inventories when they are acquired instead of when they are sold) would provide a further improvement to the status quo, though it would likely only have a marginal impact relative to other factors driving supply chain woes.

Conclusion

Repealing LIFO, as some policymakers have proposed, is not sound policy. LIFO helps firms avoid the penalty on inventory investment created by FIFO and is neither a targeted tax break nor a subsidy (as some opponents suggest).

Repealing LIFO treatment of inventory would generate relatively little revenue for its economic costs. And LIFO repeal would disproportionately burden companies within industries that maintain more inventories and further disincentivize investment that could prevent supply chain breakdowns. Though preserving LIFO will not fix supply chain issues on its own, eliminating it would make the problem worse.

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe[1] TaxEDU, “Last-In, First-Out (LIFO),” Tax Foundation, https://taxfoundation.org/tax-basics/last-in-first-out-lifo/.

[2] Kristin L. Ingram, “3 Types of Companies in Managerial Accounting,” Accounting in Focus, https://accountinginfocus.com/managerial-accounting-2/introduction-managerial-accounting-2/types-of-companies/.

[3] Kyle Pomerleau, “The Tax Treatment of Inventories and the Economic and Budgetary Impact of LIFO Repeal,” Tax Foundation, Feb. 9, 2016, https://taxfoundation.org/tax-treatment-inventories-and-economic-and-budgetary-impact-lifo-repeal.

[4] Stephen J. Entin, “The Tax Treatment of Capital Assets and Its Effect on Growth: Expensing, DepreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and disco, and the Concept of Cost RecoveryCost recovery refers to how the tax system permits businesses to recover the cost of investments through depreciation or amortization. Depreciation and amortization deductions affect taxable income, effective tax rates, and investment decisions. in the Tax System,” Tax Foundation, Apr. 24, 2013, https://taxfoundation.org/tax-treatment-capital-assets-and-its-effect-growth-expensing-depreciation-and-concept-cost-recovery/.

[5] Karl Smith, “Elizabeth Warren’s Corporate Tax Plan Sounds Reasonable. It Isn’t,” Bloomberg, Apr. 17, 2019, https://www.bloomberg.com/opinion/articles/2019-04-17/elizabeth-warren-s-corporate-tax-plan-sounds-reasonable-it-isn-t; see also Erica York, “Explaining the GAAP Between Book and Taxable Income,” Tax Foundation, Jun. 3, 2021, https://taxfoundation.org/corporations-zero-corporate-tax/.

[6] James Tobin, “Inventories, Investment, Inflation, and Taxes,” Cowles Foundation Discussion Papers 849, Cowles Foundation for Research in Economics (September 1987), https://elischolar.library.yale.edu/cgi/viewcontent.cgi?article=2091&context=cowles-discussion-paper-series.

[7] F. Owen Irvine, “Retail Inventory Investment and the Cost of Capital,” The American Economic Review 71:4 (September 1981), https://www.jstor.org/stable/1806186; see also F. Owen Irvine, “Merchant Wholesaler Inventory Investment and the Cost of Capital,” The American Economic Review 71:2 (May 1981), https://www.jstor.org/stable/1815687.

[8] Katherine Arline, “LIFO vs. FIFO: What Is the Difference,” Business News Daily, Aug. 3, 2022. https://www.businessnewsdaily.com/5514-fifo-lifo-differences.html.

[9] CSIMarket, “Inventory Turnover Ratio Screening as of Q2 of 2022,” https://csimarket.com/screening/index.php?s=it.

[10] Katherine Arline, “LIFO vs. FIFO: What Is the Difference,” Business News Daily, Aug. 3, 2022. https://www.businessnewsdaily.com/5514-fifo-lifo-differences.html.

[11] Thornton T. Matheson and Thomas Brosy, “Inflation and Oil Price Spikes Revive the Case for LIFO Repeal,” Tax Policy Center, May 12, 2022, https://www.taxpolicycenter.org/taxvox/inflation-and-oil-price-spikes-revive-case-lifo-repeal.

[12] Daniel Tinkelman and Christine E. L. Tan, “Estimating the Potential Revenue Impact of Taxing LIFO Reserves in the Current Low Commodity Price Environment,” The Journal of the American Taxation Association 40:2 (Fall 2018), https://www.researchgate.net/publication/322055031_Estimating_the_Potential_Revenue_Impact_of_Taxing_LIFO_Reserves_in_the_Current_Low_Commodity_Price_Environment. However, according to Tinkelman, these estimates are likely an underestimate of LIFO usage.

[13] April Estes, Christine Turgeon, and Jim Martin, “Taxpayers Should Consider Immediate Action to Adopt the LIFO Inventory Method to Expense High Inflation,” PricewaterhouseCoopers, Feb. 1, 2022, https://www.pwc.com/us/en/tax-services/publications/insights/assets/pwc-consider-immediate-action-to-adopt-lifo-to-expense-high-inflation.pdf.

[14] Kyle Pomerleau, “The Tax Treatment of Inventories and the Economic and Budgetary Impact of LIFO Repeal,” Tax Foundation, Feb. 9, 2016, https://taxfoundation.org/tax-treatment-inventories-and-economic-and-budgetary-impact-lifo-repeal; see also Committee for a Responsible Federal Budget, “The Tax Break-Down: LIFO Accounting,” Aug. 22, 2013, https://www.crfb.org/blogs/tax-break-down-lifo-accounting.

[15] Alistair MacDonald and Georgi Kantchev, “Companies Grapple with Post-Pandemic Inventory Dilemma,” The Wall Street Journal, Nov. 7, 2021, https://www.wsj.com/articles/companies-grapple-with-post-pandemic-inventories-dilemma-11636290000.

[16] Willy C. Shih, “Global Supply Chains in a Post-Pandemic World,” Harvard Business Review (September-October 2020), https://hbr.org/2020/09/global-supply-chains-in-a-post-pandemic-world.

[17] Julio L. Ortiz, “Spread Too Thin: The Impact of Lean Inventories,” International Finance Discussion Papers 1342, Federal Reserve, https://www.federalreserve.gov/econres/ifdp/files/ifdp1342.pdf.

[18] Raphaek Lafrogne-Joussier, Julien Martin, and Isabelle Mejean, “Supply Shocks in Supply Chains: Evidence from the Early Lockdown in China,” IMF Economic Review (2022), https://link.springer.com/content/pdf/10.1057/s41308-022-00166-8.pdf.

[19] Martin Sullivan, “Inventories, Inflation, and Supply Chain Disruption,” Tax Notes, Jun. 21, 2022, https://www.taxnotes.com/featured-analysis/inventories-inflation-and-supply-chain-disruption/2022/06/17/7dl0q.

[20] Barthélémy Bonadio, Zhen Huo, Andrei A. Levchenko, and Nitya Pandalai-Nayar, “Global Supply Chains in the Pandemic,” Journal of International Economics 133 (November 2021), https://www.sciencedirect.com/science/article/pii/S0022199621001148.

[21] Yantoultra Ngui, Debby Wu, and Yoolim Lee, “Chip Supply Faces New Crunch as Malaysia Plants Shut Down for a Week,” Bloomberg, Sep. 8, 2021, https://www.bloomberg.com/news/articles/2021-09-08/new-blow-to-chip-supplies-as-malaysia-plants-shut-for-a-week; see also Ian King, Debby Wu, and Demetrios Pogkas, “How a Chip Shortage Snarled Everything From Phones to Cars,” Bloomberg, Mar. 29, 2021, https://www.bloomberg.com/graphics/2021-semiconductors-chips-shortage/.

[22] Fernando Leibovici and Jason Dunn, “Supply Chain Bottlenecks and Inflation: The Role of Semiconductors,” Economic Synopses, Dec. 16, 2021, https://files.stlouisfed.org/files/htdocs/publications/economic-synopses/2021/12/16/supply-chain-bottlenecks-and-inflation-the-role-of-semiconductors.pdf.

[23] Yossi Sheffi, “Pandemic Shortages Haven’t Shattered the Case for ‘Just-in-Time’ Supply Chains,” The Wall Street Journal, Jan. 30, 2022, https://www.wsj.com/articles/commentary-pandemic-shortages-havent-shattered-the-case-for-just-in-time-supply-chains-11643547604?mod=djemlogistics_h; see also Norihiko Shirouzu, “How Toyota Thrives When the Chips Are Down,” Reuters, Mar. 9, 2021, https://www.reuters.com/business/autos-transportation/how-toyota-thrives-when-chips-are-down-2021-03-09/.

[24] Ibid.

[25] “Results from Semiconductor Supply Chain Request for Information,” U.S. Department of Commerce, Jan. 25, 2022, https://www.commerce.gov/news/blog/2022/01/results-semiconductor-supply-chain-request-information.

[26] Semiconductor Industry Association, “Chipmakers Are Ramping Up Production to Address Semiconductor Shortage. Here’s Why that Takes Time,” Feb. 26, 2021, https://www.semiconductors.org/chipmakers-are-ramping-up-production-to-address-semiconductor-shortage-heres-why-that-takes-time/.

Share this article