New Proposal Would Double France’s Harmful Digital Services Tax

5 min readBy:Key Points

- France is proposing to double the tax rate of its digital services tax (DST) to 6 percent.

- Because DSTs tax revenues, not profits, a company with a 10 percent profit margin would face a 60 percent effective tax rate on digital services provided in France.

- The proposal also raises the global revenue threshold for companies subject to the tax, making the DST even more discriminatory.

After France’s Constitutional Council upheld the legality of the country’s digital services taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. (DST), the National Assembly proposed an amendment to raise the DST rate from 3 percent to as high as 15 percent as part of ongoing budget negotiations. This week, a separate amendment, which would legally substitute the previous one, proposed to double the current DST rate to 6 percent. This would be a major policy shift with potentially harmful consequences for all stakeholders.

DSTs Tax Revenues Rather Than Profits

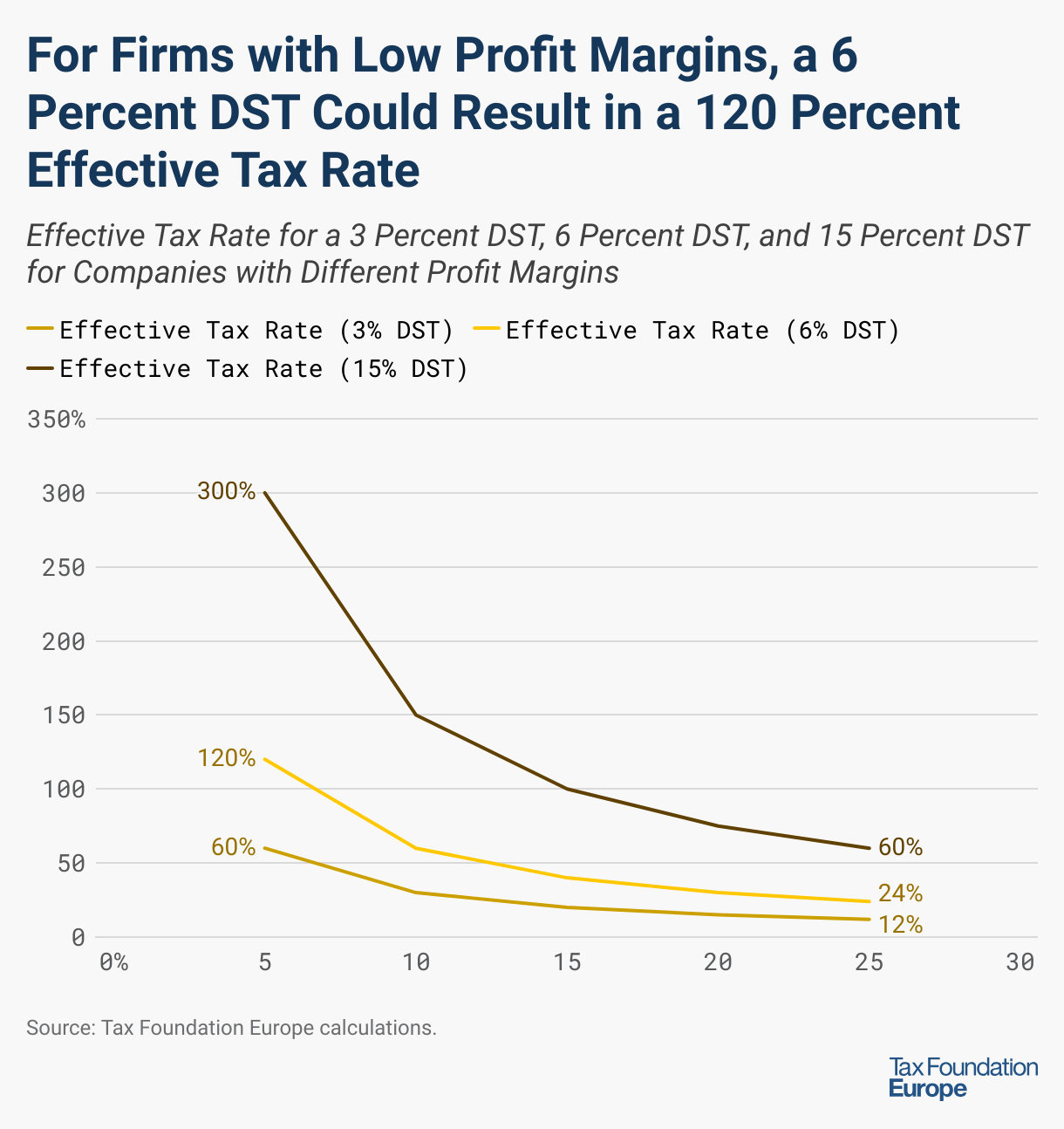

Unlike corporate income taxes, DSTs are levied on revenues rather than profits. Historically, European countries have turned away from these types of taxes because even low tax rates can translate into high effective tax burdens. For example, if a company has €100 in revenue and €90 in costs, it will earn €10 in profit. Under the current law, if a 3 percent DST is applied to that revenue, the company would owe €3 in tax (3 percent of €100 in revenue). For this company, a 3 percent tax on revenue equals a 30 percent tax on profits (a €3 tax on a €10 profit).

However, under this new proposal, if a 6 percent DST is applied to that same company, the company would owe €6 in tax (6 percent of €100 in revenue)—a 60 percent tax on profits.

The following figure shows how different profit margins for that same company earning €100 in revenue relate to different effective tax rates, under the current (3 percent) and proposed (15 percent) DST rates. With a 15 percent DST, if that company only earned a 5 percent profit margin, the effective tax rate would be 300 percent. With a 25 percent profit margin, the effective tax rate would be 60 percent.

Even before this proposal, the DST led to a disproportionate tax burden being placed on companies with lower profit margins—the less profitable a company was, the higher its effective tax rate became. This is regressive. However, a 15 percent DST would disproportionately impact all companies, regardless of profitability, and would become confiscatory for companies with profit margins below 15 percent.

A New Threshold

The amendment also raises the global revenue threshold for companies subject to the tax from €750 million to €2 billion. However, this increase will make the DST even more discriminatory in terms of company size. The revenue threshold results in the tax only being applied to large multinationals. While this can avoid burdening smaller companies, it also provides a relative advantage for businesses below the threshold and creates an incentive for businesses operating near the threshold to alter their behavior.

The French DST, which functions like a tariffTariffs are taxes imposed by one country on goods imported from another country. Tariffs are trade barriers that raise prices, reduce available quantities of goods and services for US businesses and consumers, and create an economic burden on foreign exporters. on certain services, is designed to be discriminatory; it targets industries largely dominated by US companies, and the discrimination would be even greater if the revenue threshold is increased. The US government has voiced opposition to DSTs over the last decade, with President Trump using Section 301 investigations in his first term, and, more recently, the US Congress threatening the Section 899 retaliatory tax. Should the proposed measure become law, the US is expected to respond with retaliatory trade measures.

Economic Incidence

The amendment summary claims that the DST will “support digital sovereignty and public finances without burdening households or domestic firms.” However, this overlooks the economic reality of tax incidenceTax incidence is a measure of who bears the legal or economic burden of a tax. Legal incidence identifies who is responsible for paying a tax while economic incidence identifies who bears the cost of tax—in the form of higher prices for consumers, lower wages for workers, or lower returns for shareholders.. A recent research paper by economists Dominika Langenmayr and Rohit Reddy Muddasani shows that the attempt to target big digital platforms misses the mark as the cost mostly falls on consumers.

A Higher DST Will Not Solve France’s Deficit Problem

Part of the justification is to increase the revenue collected by the DST. Nevertheless, DST revenue in Austria, France, Italy, Spain, Turkey, and the UK ranged from €103 million (Austria) to €1.03 billion (the UK) in the most recent year revenue was reported. These various DSTs across Europe do not work well together. They work on different tax bases, and double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. on the same services is common.

Turkey’s DST, with a tax rate of 7.5 percent, brings in the most at 0.14 percent of total revenues, while France’s current DST brings in less than 0.06 percent of total revenues.

Even if France were able to quintuple its DST’s tax collection (an unlikely outcome), the amount raised would still be less than one percent of the country’s general revenue.

Recent Revenue Raised from Selected Digital Services Taxes

| Country | Most Recent Year for Official DST Revenue Reported | DST Revenue (Local Currency) in Millions | DST Revenue (in EUR) in Millions |

|---|---|---|---|

| Austria | 2023 | € 103 | |

| France | 2024 | € 756 | |

| Italy | 2024 | € 455 | |

| Spain | 2024 | € 375 | |

| Turkey | 2024 | ₺ 15,561 | € 322 |

| United Kingdom | 2025 | £900 | € 1,032 |

Source: Tax Foundation analysis of national budget documents and announcements.

If France is worried about raising more money from digital services, then it should continue reforming its value-added tax (VAT) to effectively tax these services at the point of consumption. Additionally, broadening the VAT tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. by eliminating reduced rates and exemptions would increase France’s VAT revenue by 44.5 percent while causing fewer distortions in the economy. Finally, the VAT is trade-neutral and does not discriminate between firms.

Since a new DST would neither resolve France’s revenue shortfall nor avoid shifting the burden to consumers—and could trigger renewed trade tensions—it’s time for policymakers to reconsider their approach. Rather than expanding the DST, they should eliminate it altogether. The core purpose of tax policy is to raise revenue efficiently, and there are far more effective tools than a DST to achieve that goal.

Subscribe to our free newsletter to get the latest tax data, news and analysis.Stay informed on the tax policies impacting you.

About the Author

Cristina Enache writes on the economics of tax policy and is the author of the Spanish Regional Tax Competitiveness Index. She was formerly the Director of Research at Civismo, an economic research organization based in Spain. She also served as head of research at Institución Futuro, a regional think tank based in Navarra in northern Spain. She is also currently Secretary-General at the World Taxpayers Associations and General Manager of the Spanish Taxpayers Union, which she joined in 2016.