Modeling the Impact of President Trump’s Proposed Tariffs

The Trump administration’s proposed tariffs would lead to job losses and a reduction in economic growth, as the Tax Foundation’s updated Tax and Growth model shows.

4 min read

Kyle Pomerleau is a resident fellow at the American Enterprise Institute (AEI), where he studies federal tax policy.

Before joining AEI, Mr. Pomerleau was chief economist and vice president of economic analysis at the Tax Foundation, where he led the macroeconomic and tax modeling team and wrote on various tax policy topics, including corporate taxation, international tax policy, carbon taxation, and tax reform.

The author of many studies, Mr. Pomerleau has been published in trade publications and policy journals including Tax Notes and the National Tax Journal. He is frequently quoted in major media outlets such as The New York Times, The Wall Street Journal, and The Washington Post. He has also testified before Congress and state legislators.

Mr. Pomerleau has an MPP in economic and social policy from Georgetown University’s McCourt School of Public Policy and a BA in history and political science from the University of Southern Maine.

The Trump administration’s proposed tariffs would lead to job losses and a reduction in economic growth, as the Tax Foundation’s updated Tax and Growth model shows.

4 min read

The Tax Cuts and Jobs Act was meant to boost growth and deter corporate inversions. What does it mean that an Ohio company is still moving its HQ to the UK?

5 min read

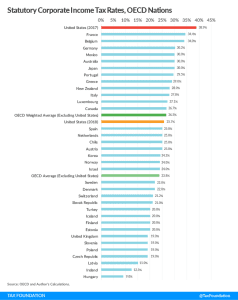

The Tax Cuts and Jobs Act significantly reduced the federal statutory corporate income tax rate. When combined with state and local taxes, it put the U.S.’s corporate tax rate in line with the average among OECD nations.

4 min read

The TCJA is projected to improve the United States’ current ranking from 30th among the 35 Organisation for Economic Co-operation and Development (OECD) countries to 25th, an improvement of five places.

4 min read

Hampered by high marginal tax rates and complex business tax rules, the United States again ranks towards the bottom of the pack on our 2017 International Tax Competitiveness Index, placing 30 out of 35 OECD countries.

11 min read

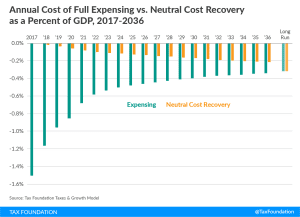

Instead of making expensing temporary, lawmakers could pursue other ways to speed up cost recovery with permanent economic gains and without drastically reducing revenue. One way to do that is by enacting “depreciation indexing.”

12 min read

These four Tax Foundation tax plans demonstrate ways in which lawmakers could achieve permanent, pro-growth tax reform while keeping the level of federal revenue and the distribution of the tax burden roughly the same as current law.

25 min read

The last time the U.S. reduced its federal corporate income tax rate was in 1986. Since then, countries throughout the world have significantly reduced their rates, leaving the U.S. with the fourth highest statutory corporate tax rate in the world and an overall uncompetitive tax system.

11 min read

A well-designed territorial tax system would reduce the incentive for companies to invert, encourage businesses to invest in and expand operations throughout the world, and allow capital to flow more freely back to the U.S., but would also come with some new challenges.

28 min read

Some federal lawmakers want a longer budget window to keep temporary tax cuts in place longer. However, temporary tax cuts would still have drawbacks and won’t provide the benefits of permanent tax reform.

5 min read

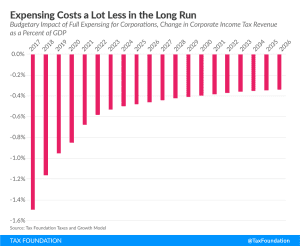

Full expensing could grow the long-run size of the U.S. economy by 4.2 percent, which would lead to 3.6 percent higher wages and 808,000 full-time jobs. What’s more, it wouldn’t cost as much revenue as some think.

12 min read