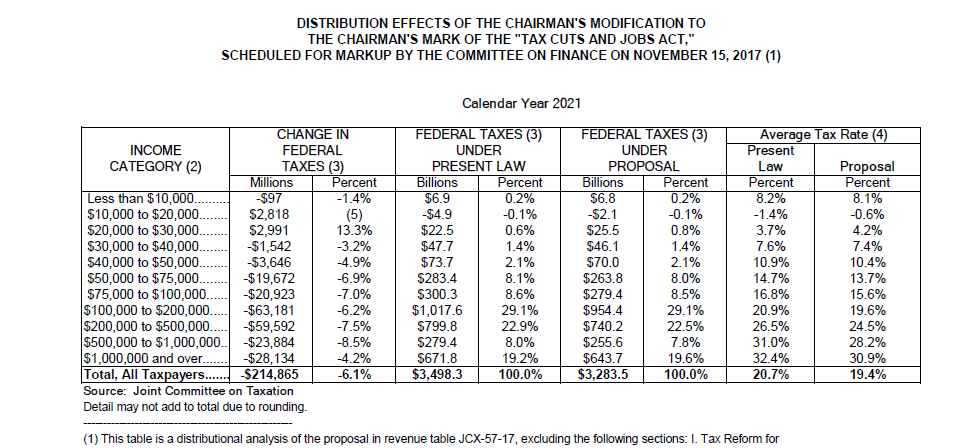

This morning, the Joint Committee on Taxation (JCT) released an updated distributional table reflecting the modifications made to the Senate’s Tax Cuts and Jobs Act. The table includes the impact of all the new provisions, including the functional repeal of the individual mandate penalty. The inclusion of this provision is reflected in a unique way on the distribution table.

The table for 2021 has drawn the most attention.

At first glance, the table shows that individuals with incomes from $10,000 to $30,000 would face a taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. increase under the new proposal, compared to current law. However, this appears to be due to the provisions eliminating the individual mandate.

How could repealing a mandate to buy insurance lead to a tax increase? Understanding how insurance premiums work under the Affordable Care Act is key to interpreting JCT’s result. Individuals without qualified health insurance, such as from an employer, are able to purchase insurance from exchanges based in every state. If the individual makes between 100 and 400 percent of the federal poverty level, the individual receives a premium tax credit to offset some or all of the cost of insurance. The premium tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income rather than the taxpayer’s tax bill directly. is paid monthly, directly to the insurance company.

However, the Congressional Budget Office assumes that many individuals purchase insurance only because the individual mandate requires them to do so. As a result, when fewer individuals purchase health insurance from an exchange, fewer individuals receive premium tax credits. Less of an advanceable refund from the Treasury results in the appearance of a tax increase under JCT’s distributional analysis.

Many can argue as to how many individuals would purchase insurance without the mandate penalty, but lowering the mandate to zero impacts the distributional analysis of the Senate’s current tax plan, according to the Joint Committee on Taxation.

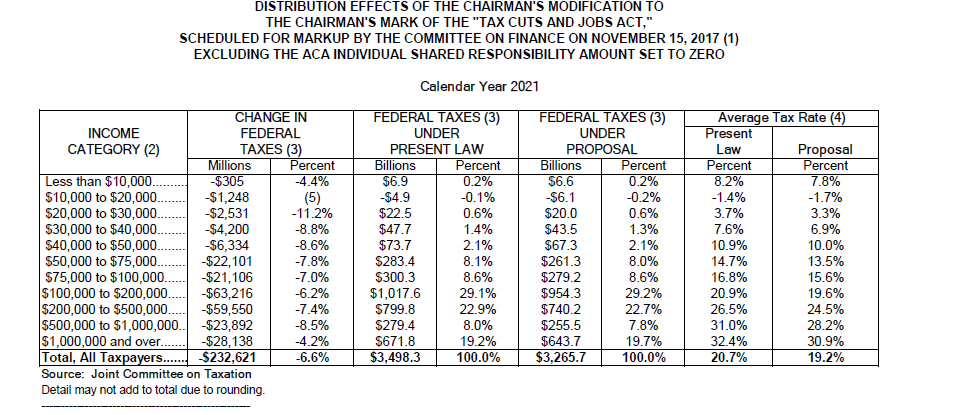

In fact, we now know that the JCT’s finding of a tax increase on households making between $10,000 and $30,000 is entirely due to the individual mandate penalty being lifted. JCT released a separate set of distributional tables reflecting the Senate bill, including the modifications from earlier in the week, but excluding the individual mandate being decreased to zero. In these tables, the tax increase disappears.

All incomes would see a decrease in their tax liability under this scenario.

Much attention is being paid to the new distributional tables being released by JCT this morning, but their results don’t quite seem to show what some are suggesting. While the results appears to show a tax increase for some lower-income filers, this is due to the unique nature of the individual mandate and the premium tax credits available under the Affordable Care Act.

Share this article