Patent Box Regimes in Europe, 2020

4 min readBy: ,Patent box regimes (also referred to as intellectual property, or IP, regimes) provide lower effective tax rates on income derived from IP. Most commonly, eligible types of IP are patents and software copyrights. Depending on the patent boxA patent box—also referred to as intellectual property (IP) regime—taxes business income earned from IP at a rate below the statutory corporate income tax rate, aiming to encourage local research and development. Many patent boxes around the world have undergone substantial reforms due to profit shifting concerns. regime, income derived from IP can include royalties, licensing fees, gains on the sale of IP, sales of goods and services incorporating IP, and patent infringement damage awards.

The aim of patent boxes is generally to encourage and attract local research and development (R&D), incentivizing businesses to locate IP in the country. However, patent boxes can introduce another level of complexity to a taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. system, and some recent research questions whether patent boxes are actually effective in driving innovation.

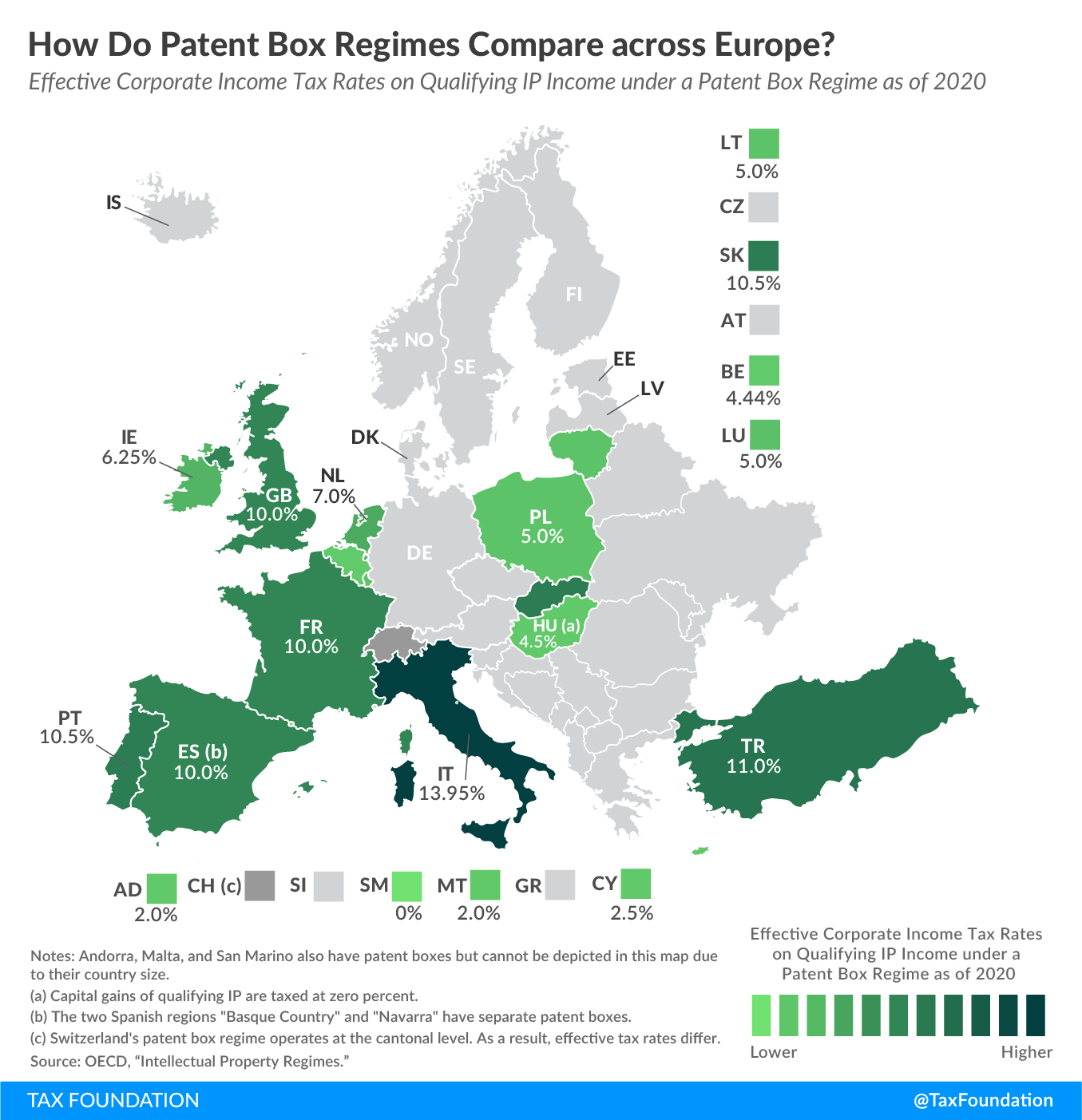

As today’s map shows, patent box regimes are relatively widespread in Europe. Most have been implemented within the last two decades.

Currently, 14 of the 27 EU member states have a patent box regime in place. These are Belgium, Cyprus, France, Hungary, Ireland, Italy, Lithuania, Luxembourg, Netherlands, Poland, Portugal, Slovakia, Spain (federal, Basque Country, and Navarra), and the United Kingdom. Non-EU countries Andorra, San Marino, Switzerland, and Turkey have also implemented patent box regimes.

The reduced tax rates provided under patent box regimes range from 0 percent in San Marino and Hungary to 13.95 percent in Italy.

| Qualifying IP Assets | Tax Rate Under Patent Box Regime | Statutory Corporate Income Tax Rate | |||

|---|---|---|---|---|---|

| Patents | Software | Other1 | |||

| Andorra | X | X | 2% | 10% | |

| Belgium | X | X | 4.44% | 29.58% | |

| Cyprus | X | X | X | 2.5% | 12.5% |

| France | X | X | 10% | 32.02% | |

| Hungary2 | X | X | 0% or 4.5% | 9% | |

| Ireland | X | X | X | 6.25% | 12.5% |

| Italy3 | X | X | 13.95% | 27.9% | |

| Lithuania | X | X | 5% | 15% | |

| Luxembourg | X | X | 4.99% | 24.94% | |

| Malta | X | X | 1.75% | 35% | |

| Netherlands | X | X | X | 7% | 16.5% to 25% |

| Poland | X | X | 5% | 19% | |

| Portugal | X | 10.5% | 21% | ||

| San Marino4 | X | X | 0% or 8.5% | 17% | |

| Slovakia | X | X | 10.5% | 21% | |

| Spain – federal5 | X | X | 10% | 25% | |

| Spain – Basque Country | X | X | 7.2% | 25% | |

| Spain – Navarra | X | X | 8.4% | 25% | |

| Switzerland6 | X | Varies from canton to canton, up to a 90% exemption from corporate tax | Varies from canton to canton; 11.9% to 21.6% | ||

| Turkey7 | X | 11% | 22% | ||

| United Kingdom | X | 10% | 19% | ||

|

Notes: 1. ”Other” refers to IP assets that are non-obvious, useful, and novel. These can only be applied to small and medium-size businesses. 2. Hungary’s patent box regime applies a zero percent rate in the case of capital gains of reported qualifying IP and 4.5 percent in the case of benefits related to royalty income. 3. Italy has a federal corporate income tax (IRES) of 24 percent and a regional production tax (IRAP) of 3.9 percent, thus a combined statutory rate of 27.9 percent. Italy’s patent box regime reduces both tax rates by 50 percent, leading to a tax rate of 13.95 percent on IP income. 4. San Marino has three IP regimes. The “New companies regime provided by art. 73, law no. 166/2013” grants a tax rate of 8.5 percent. The “Regime for high-tech start-up companies under law no. 71/2013 and delegated decree no. 116/2014” and the “IP regime” both grant tax rates of 0 percent. All three apply to patents and software. 5. The Spanish regions “Basque Country” and “Navarra” have separate IP regimes. 6. Switzerland introduced a patent box regime which went into effect in 2020 at the cantonal level covering all of Switzerland. The regime provides a maximum tax base reduction of 90 percent on income from patents and similar rights developed in Switzerland. Cantons can opt for a lower reduction. 7. Turkey has a second IP regime which allows for a full tax deduction (0 percent effective tax rate) of qualified IP income resulting from R&D activities that were undertaken in Turkish Technology Development Zones. Liechtenstein has abolished its patent box regime because it did not comply with the OECD’s Modified Nexus Approach. Sources: OECD Dataset Intellectual Property Regimes; Deloitte: The Cyprus IP regime; PwC: French Finance Act for 2019; Ireland’s Office of the Revenue Commissioners: Guidance Notes on the Knowledge Development Box. |

|||||

In 2015, OECD countries agreed on a so-called Modified Nexus Approach for IP regimes as part of Action 5 of the OECD’s Base Erosion and Profit Shifting (BEPS) Action Plan. This Modified Nexus Approach limits the scope of qualifying IP assets and requires a geographic link among R&D expenditures, IP assets, and IP income. To be in line with this approach, previously noncompliant countries have either abolished or amended their patent box regimes within the last few years.

Many European countries offer additional R&D incentives, such as direct government support, R&D tax credits, or accelerated depreciation on R&D assets. The effective tax rates on IP income can therefore be lower than the ones stated in the respective patent box regimes.

Share this article