Scott Eastman

Federal Research Manager

Scott Eastman is federal research manager at the Tax Foundation, where he coordinates research production for the Center for Federal Tax Policy. Prior to joining the Tax Foundation, Scott was program manager for the Mercatus Center at George Mason University’s Project for the Study of American Capitalism.

Scott has a master’s degree in economics from George Mason University, and a bachelor’s degree in political science from the University of Nebraska at Lincoln. Scott’s favorite season is fall and he is a fan of Cornhusker football.

Latest Work

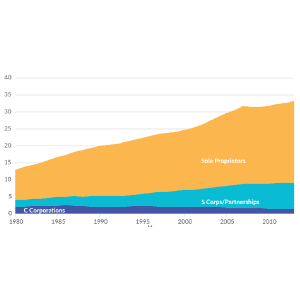

Increasing Individual Income Tax Rates Would Impact a Majority of US Businesses

Since most U.S. businesses are pass-through businesses, such as partnerships, S corporations, LLCs, and sole proprietorships, changes to the individual income tax, especially to top marginal rates, can affect a business’s incentives to invest, hire, and produce.

4 min read

Sanders’ Estate Tax Plan Won’t Likely Raise the Revenue Intended

While progressivity may look appealing—particularly at a time when policymakers in Congress seem to be competing on how best to extract revenue from the wealthiest in the country—it may not raise the revenue intended.

2 min read

Opportunity Zones: What We Know and What We Don’t

Research suggests place-based incentive programs redistribute rather than generate new economic activity, subsidize investments that would have occurred anyway, and displace low-income residents.

20 min read

New IRS Data Reiterates Shortcomings of the Estate Tax

The estate tax’s narrow base and high rate limit its ability to generate revenue. The estate tax discourages economic growth by discouraging investment.

3 min read