Kentucky Legislature Sends Pro-Growth Tax Changes to Governor

Kentucky is making commendable progress toward a more modern and competitive tax code, but more work on comprehensive tax reform should be prioritized next session.

7 min read

Katherine Loughead is a Senior Policy Analyst & Research Manager with the Center for State Tax Policy at the Tax Foundation, where she serves as a resource to policymakers in their efforts to modernize and improve the structure of their state tax codes.

Katherine has testified before legislators in seven states and has authored or coauthored tax reform options guides on Kansas, Kentucky, Nebraska, and Wisconsin. Her work has been cited in The New York Times, The Economist, USA TODAY, Forbes, the Associated Press, and numerous state media outlets across the country.

Prior to joining the Tax Foundation in 2018, Katherine worked for a US senator and a member of the US House of Representatives, where she advised on tax policy during the consideration of the historic Tax Cuts and Jobs Act. A graduate of the John Wesley Honors College at Indiana Wesleyan University, Katherine holds a degree in English and Business Administration, as well as a paralegal certificate from Georgetown University.

Originally from Belvidere, Illinois, Katherine now lives in Nashville, Tennessee, where in her spare time she enjoys rock climbing and taking flying trapeze classes.

Kentucky is making commendable progress toward a more modern and competitive tax code, but more work on comprehensive tax reform should be prioritized next session.

7 min read

After a whirlwind of cuts and reforms in 2021, it looks like 2022 might be an even bigger year for state tax codes. Republican and Democratic governors alike used their annual State of the State addresses to call for tax reform, and there is already serious momentum from state lawmakers nationwide to get the job done.

3 min read

As Kentucky policymakers make final decisions on tax relief this year, they should make the most of this opportunity to return excess tax collections in a manner that would also enhance the Bluegrass State’s prospects for long-term economic growth.

5 min read

If Nebraska is to create a competitive environment and attract in-state investment, comprehensive tax modernization must be a priority.

9 min read

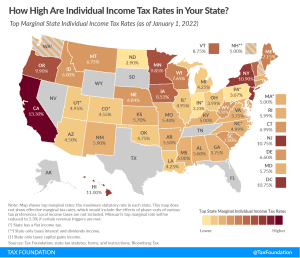

Individual income taxes are a major source of state government revenue, accounting for more than a third of state tax collections:

28 min read

With the adoption of its new budget in mid-November, North Carolina has reinforced its position as a leader in pro-growth tax reform, becoming the 12th state to enact income tax rate reductions in 2021 alone.

7 min read

Through 10 ballot measures across four states—Colorado, Louisiana, Texas, and Washington—voters will decide significant questions of state tax policy.

7 min read

Taken together, the proposed reforms would further solidify North Carolina’s position as a leader in sound tax policy and as a state whose tax code is among the most conducive to generating long-term economic growth.

7 min read

In most states, tax incentives abound, usually offered as a way of promoting new investment or attracting certain industries by shielding them from the full impact of otherwise high tax rates.

6 min read

As states close their books for fiscal year 2021, many have much more revenue on hand than they anticipated last year. Eleven states have responded by reducing income tax rates and making related structural reforms as they strive to solidify a competitive advantage in an increasingly competitive national landscape.

29 min read

As policymakers consider ways to improve their tax structure to encourage business investment and promote economic growth, corporate income tax rate reductions are a crucial part of that conversation, but they shouldn’t be the only consideration.

6 min read

After weeks of deliberations, Arizona Gov. Doug Ducey signed into law a budget for fiscal year (FY) 2022 that reduces the state’s individual income tax rates and consolidates brackets, a plan that will help restore Arizona’s reputation as a low-tax alternative to California.

7 min read

Reducing the second-highest individual income tax rate, repealing the TPP tax, and freezing UI tax rates are three valuable reforms that would help promote a smooth economic recovery in Wisconsin while setting the state up for robust economic growth for years to come.

6 min read

Thirteen states have notable tax changes taking effect on July 1, 2021, which is the first day of fiscal year (FY) 2022 for every state except Alabama, Michigan, New York, and Texas. Individual and corporate income tax changes usually take effect at the beginning of the calendar year for the sake of maintaining policy consistency throughout the tax year, but sales and excise tax changes often correspond with the beginning of a fiscal year.

11 min read

As Wisconsin emerges from the pandemic, state policymakers have a rare opportunity to reinvest excess revenues in a structurally sound manner that will make the state more attractive to individuals and businesses, promote a quicker and more robust economic recovery, and put the state on the path to increased in-state investment and growth for many years to come.

7 min read

The income tax changes in HB 2900 as introduced would improve Arizona’s individual income tax structure and economic competitiveness, making the state more attractive to individuals and pass-through businesses .

8 min read

State taxation of GILTI is unconventional and economically uncompetitive and will become even more so if the federal government adopts a more aggressive approach to taxing GILTI, as outlined in the American Jobs Plan Act.

29 min read

A landmark comparison of corporate tax costs in all 50 states, Location Matters provides a comprehensive calculation of real-world tax burdens, going beyond headline rates to demonstrate how tax codes impact businesses and offering policymakers a road map to improvement.

8 min read