Emissions Trading System (ETS)

The Emissions Trading System (ETS) is a form of environmental taxation that seeks to use the dynamics of supply and demand to reduce the European Union’s (EU) overall carbon emissions in line with its broader climate change reduction goals.

The market price of carbon is set by cleaner firms trading allowances with more carbon-intensive firms while the overall cap on allowed emissions is reduced over time.

What Does the Emissions Trading System Do?

The Emissions Trading System (ETS) is a domestic carbon pricing mechanism in the EU that works on the “cap-and-trade” principle by setting a cap on the total amount of emissions allowed to be released into the environment by all operators. The ETS covers sectors such as power and heat generation, aviation within Europe, and energy-intensive industrial sectors that represent around 45 percent of the EU’s greenhouse gas emissions.

The ETS works by keeping carbon-intensive European industries competitive through “free” allocations of ETS allowances. Polluting companies that may not be able to afford a reduction in emissions can purchase allowances from companies that can afford to. In theory, this should neutralize emissions from polluting firms in the EU and incentivize the development of low-carbon emission technologies.

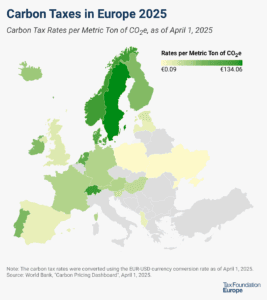

The ETS differs from a carbon tax because its price remains flexible depending on the supply and demand of permitted allowances rather than setting a fixed price on the emissions and letting operators decide their levels of emissions.

Current ETS revenue is used to tackle climate change through Member States investing in zero-emissions vehicles and mobility, improving energy efficiency and renovations, and addressing social aspects of the environmental transition. It will also be used to finance the EU’s COVID-19 recovery instrument, NextGenerationEU.

The EU agreed to revise the ETS in December 2022. The main changes are the inclusion of maritime shipping emissions in the current system, a reduced cap and more ambitious linear reduction of allowances, and the creation of a new separate emissions trading system to include the buildings, road transport, and fuel sectors starting in 2027.

What Is the Carbon Border Adjustment Mechanism (CBAM)?

The Carbon Border Adjustment Mechanism (CBAM) is designed to complement the Emissions Trading System by placing a carbon price on certain imports into the EU from other countries, such as Russia or the United States, that do not tax carbon at an “EU-approved” level. CBAM is also supposed to serve as a replacement mechanism for ETS’s free allowance system by 2034. The goal is to maintain the competitiveness of European producers relative to foreign producers and prevent carbon leakage—when climate policy in one jurisdiction leads to emissions-producing activity simply shifting to a different jurisdiction.

Following the provisional political agreement on CBAM in December 2022, the mechanism will be phased in gradually and will only apply to imports of certain goods most at risk of carbon leakage, such as cement, iron, steel, fertilizers, electricity, aluminum, and hydrogen.

CBAM does not include export rebates, limiting the competitiveness of EU products in markets around the world. More than a mechanism, CBAM has the economic effects of a border tariff rather than a true adjustment.

Stay updated on the latest educational resources.

Level-up your tax knowledge with free educational resources—primers, glossary terms, videos, and more—delivered monthly.

Subscribe