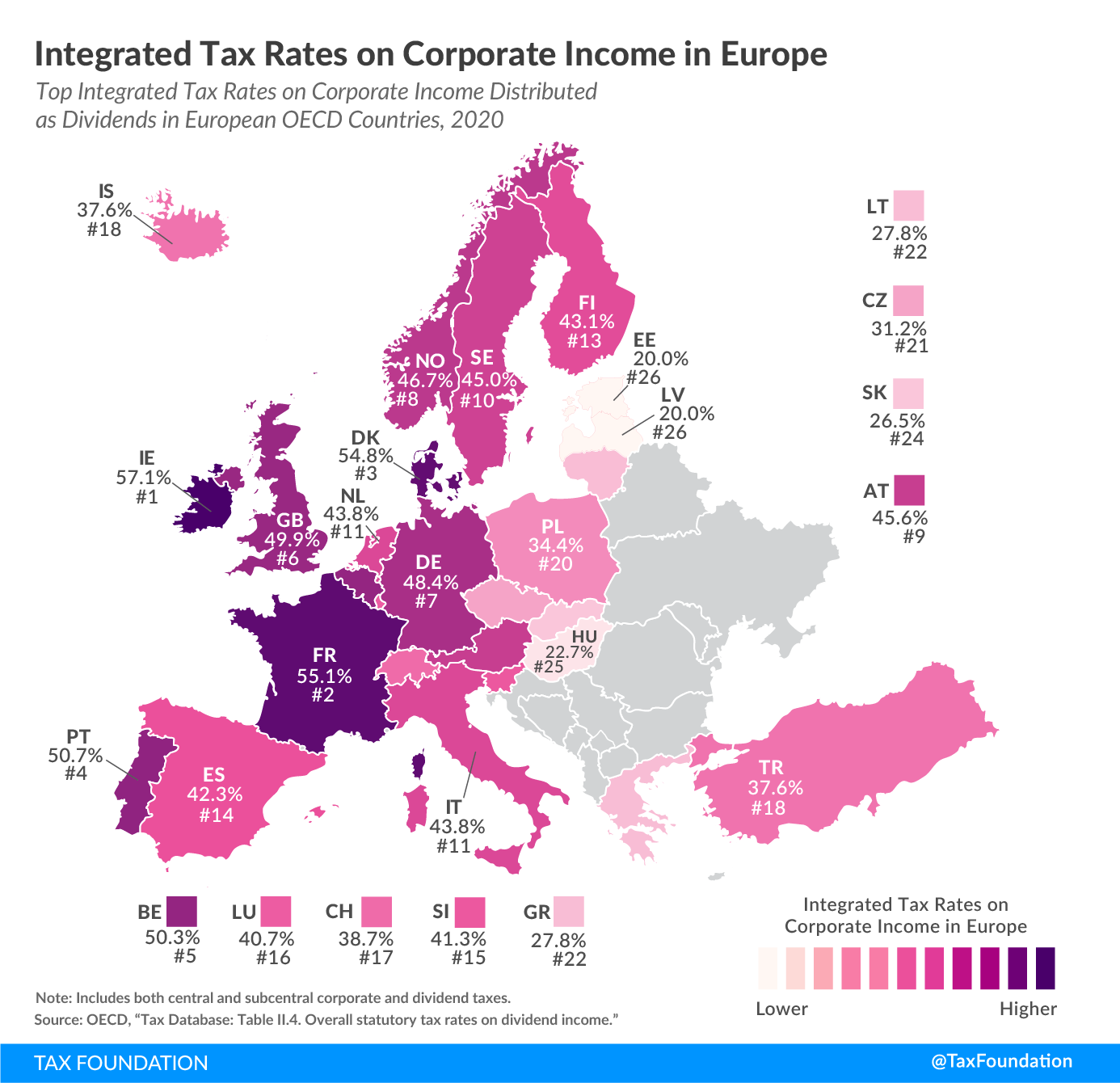

Integrated Tax Rates on Corporate Income in Europe, 2021

4 min readBy:In most European OECD countries, corporate income is taxed twice, once at the entity level and once at the shareholder level. Before shareholders pay taxes, the business first faces the corporate income tax. A business pays corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. on its profits; thus, when the shareholder pays their layer of taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. they are doing so on dividends or capital gains distributed from after-tax profits. The integrated tax rate on corporate income reflects both the corporate income tax and the dividends or capital gains tax—the total tax levied on corporate income.

As an example, suppose that an Italian corporation earns $100 of profit in 2020. It must pay corporate income tax of $24, which leaves the corporation with $76 in after-tax profits. If the corporation distributes those earnings as a dividend, the income is taxed again at the individual level at a top dividend rate of 26 percent, resulting in $19.76 in dividend taxes. Thus, final after-tax income is $56.24, implying that the $100 in original corporate profits faces an integrated tax rate on corporate income of 43.76 percent. (The same calculation can be done for corporate income realized as capital gains.)

For dividends, Ireland’s top integrated tax rate was highest among European OECD countries, at 57.1 percent, followed by France (55.1 percent) and Denmark (54.8 percent). Estonia (20 percent), Latvia (20 percent), and Hungary (22.7 percent) levy the lowest rates. Estonia and Latvia’s dividend exemption system means that the corporate income tax is the only layer of taxation on corporate income distributed as dividends.

For capital gains, Denmark (54.8 percent), France (52.4 percent), and Portugal (50.7 percent) have the highest integrated rates among European OECD countries, while the Czech Republic (19 percent), Slovenia (19 percent), and Slovakia (21 percent) levy the lowest rates. Several European OECD countries—namely Belgium, the Czech Republic, Luxembourg, Slovakia, Slovenia, Switzerland, and Turkey—do not levy capital gains taxes on long-term capital gains, making the corporate tax the only layer of tax on corporate income realized as long-term capital gains.

| OECD Country | Statutory Corporate Income Tax Rate | Dividends | Capital Gains (a) | ||

|---|---|---|---|---|---|

| Top Personal Dividend Tax Rate | Integrated Tax on Corporate Income (Dividends) | Top Personal Capital Gains Tax Rate | Integrated Tax on Corporate Income (Capital Gains) | ||

| Austria (AT) | 25.0% | 27.5% | 45.6% | 27.5% | 45.6% |

| Belgium (BE) | 29.0% | 30.0% | 50.3% | 0.0% | 29.0% |

| Czech Republic (CZ) | 19.0% | 15.0% | 31.2% | 0.0% | 19.0% |

| Denmark (DK) | 22.0% | 42.0% | 54.8% | 42.0% | 54.8% |

| Estonia (EE) | 20.0% | 0.0% | 20.0% | 20.0% | 36.0% |

| Finland (FI) | 20.0% | 28.9% | 43.1% | 34.0% | 47.2% |

| France (FR) | 32.0% | 34.0% | 55.1% | 30.0% | 52.4% |

| Germany (DE) | 29.9% | 26.4% | 48.4% | 26.4% | 48.4% |

| Greece (GR) | 24.0% | 5.0% | 27.8% | 15.0% | 35.4% |

| Hungary (HU) | 9.0% | 15.0% | 22.7% | 15.0% | 22.7% |

| Iceland (IS) | 20.0% | 22.0% | 37.6% | 22.0% | 37.6% |

| Ireland (IE) | 12.5% | 51.0% | 57.1% | 33.0% | 41.4% |

| Italy (IT) | 24.0% | 26.0% | 43.8% | 26.0% | 43.8% |

| Latvia (LV) | 20.0% | 0.0% | 20.0% | 20.0% | 36.0% |

| Lithuania (LT) | 15.0% | 15.0% | 27.8% | 20.0% | 32.0% |

| Luxembourg (LU) | 24.9% | 21.0% | 40.7% | 0.0% | 24.9% |

| Netherlands (NL) | 25.0% | 25.0% | 43.8% | 30.0% | 47.5% |

| Norway (NO) | 22.0% | 31.7% | 46.7% | 31.7% | 46.7% |

| Poland (PL) | 19.0% | 19.0% | 34.4% | 19.0% | 34.4% |

| Portugal (PT) | 31.5% | 28.0% | 50.7% | 28.0% | 50.7% |

| Slovak Republic (SK) | 21.0% | 7.0% | 26.5% | 0.0% | 21.0% |

| Slovenia (SI) | 19.0% | 27.5% | 41.3% | 0.0% | 19.0% |

| Spain (ES) | 25.0% | 23.0% | 42.3% | 23.0% | 42.3% |

| Sweden (SE) | 21.4% | 30.0% | 45.0% | 30.0% | 45.0% |

| Switzerland (CH) | 21.1% | 22.3% | 38.7% | 0.0% | 21.1% |

| Turkey (TR) | 22.0% | 20.0% | 37.6% | 0.0% | 22.0% |

| United Kingdom (GB) | 19.0% | 38.1% | 49.9% | 20.0% | 35.2% |

| Average | 21.9% | 23.3% | 40.1% | 19.0% | 36.7% |

|

Notes: Integrated tax rates are calculated as follows: (Corporate Income Tax) + [(Distributed Profit – Corporate Income Tax) * Dividends or Capital Gains Tax]. (a) In some countries, the capital gains tax rate varies by type of asset sold. The capital gains tax rate used in this report is the rate that applies to the sale of listed shares after an extended period of time. While the integrated tax rate on dividends captures subcentral taxes, this may not be the case for all integrated tax rates on capital gains due to data availability. (b) In the Netherlands, the net asset value is taxed at a flat rate on a deemed annual return. Source: OECD, “Tax Database: Table II.4. Overall statutory tax rates on dividend income,” last updated September 2020, https://stats.oecd.org/Index.aspx?QueryId=59615; PwC, “Quick Charts: Capital gains tax (CGT) rates,” https://taxsummaries.pwc.com/quick-charts/capital-gains-tax-cgt-rates; author’s calculations. |

|||||