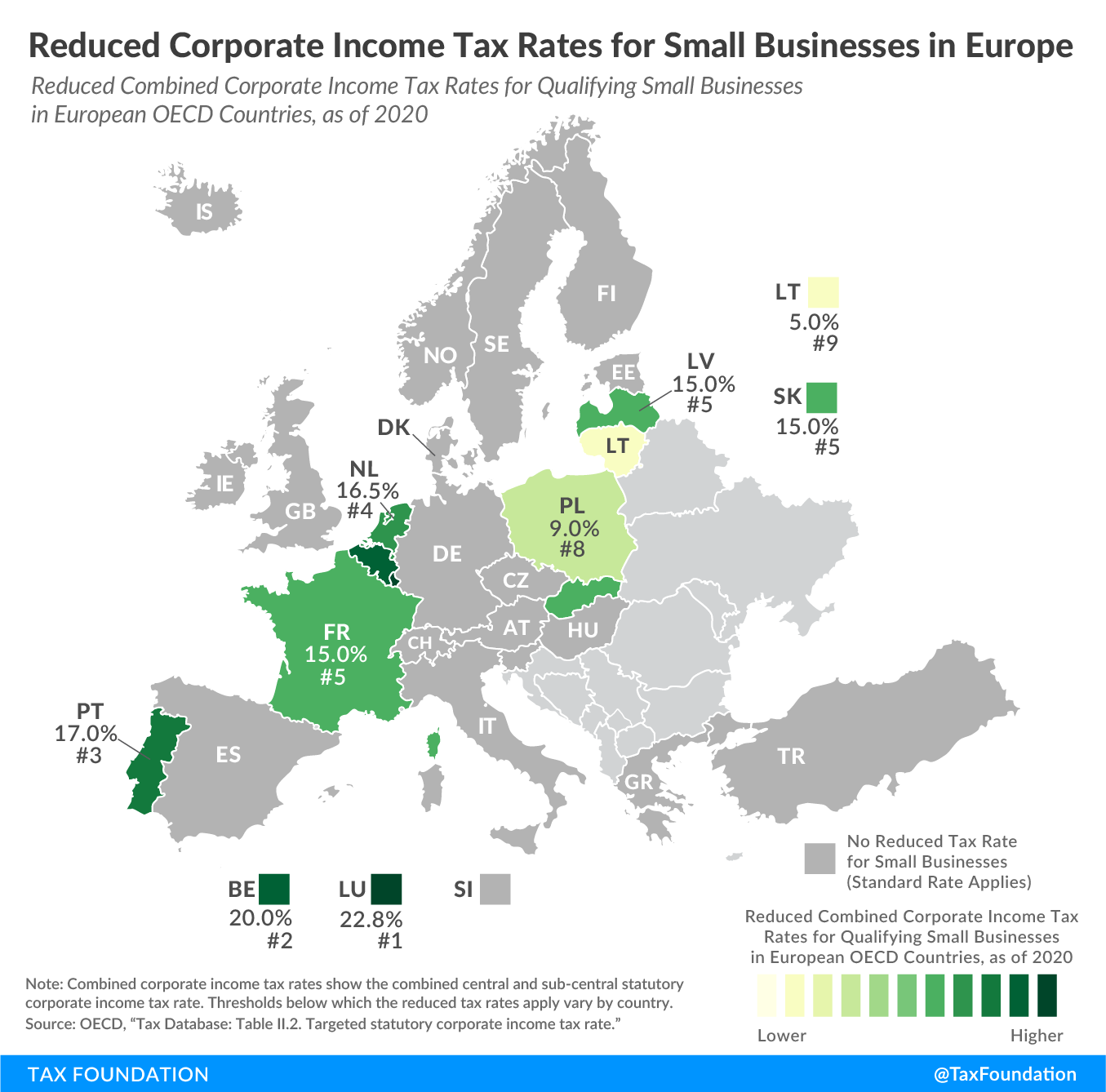

Reduced Corporate Income Tax Rates for Small Businesses in Europe

2 min readBy:Corporate income taxes are commonly levied as a flat rate on business profits. However, some countries provide reduced corporate income tax rates for small businesses. Out of 27 European OECD countries covered in today’s map, nine levy a reduced corporate taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rate on businesses that have revenues or profits below a certain threshold.

Belgium, France, Latvia, Lithuania, Luxembourg, the Netherlands, Poland, Portugal, and Slovakia levy reduced corporate tax rates on businesses below a certain size. In 2020, the reduced rates range from 5 percent in Lithuania to 22.8 percent in Luxembourg.

The largest difference between the reduced and the standard top corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate is in France, at 17.02 percentage points. Large businesses pay a standard top rate of 32.02 percent, while small businesses pay a reduced rate of 15 percent on profits up to €38,120. Luxembourg’s difference in rates is smallest, at 2.14 percentage points (standard rate of 24.94 percent and reduced rate of 22.8 percent).

| Country | Reduced Combined Corporate Income Tax | Standard Combined Top Corporate Income Tax Rate | |

|---|---|---|---|

| Reduced Rate | Threshold for Reduced Rate | ||

| Austria (AT) | – | – | 25.0% |

| Belgium (BE) | 20.0% | Applicable on the first €100,000 of taxable income of qualifying companies. | 25.0% |

| Czech Republic (CZ) | – | – | 19.0% |

| Denmark (DK) | – | – | 22.0% |

| Estonia (EE) | – | – | 20.0% |

| Finland (FI) | – | – | 20.0% |

| France (FR) | 15.0% | Applicable where turnover does not exceed €7.63 million, and on the part of the profit that does not exceed €38,120. | 32.0% |

| Germany (DE) | – | – | 29.9% |

| Greece (GR) | – | – | 24.0% |

| Hungary (HU) | – | – | 9.0% |

| Iceland (IS) | – | – | 20.0% |

| Ireland (IE) | – | – | 12.5% |

| Italy (IT) | – | – | 27.8% |

| Latvia (LV) | 15.0% | Applicable where revenue does not exceed €40,000. | 20.0% |

| Lithuania (LT) | 5.0% | Applicable for companies whose average number of employees does not exceed 10 and whose income during the tax period does not exceed €300,000. A one-year corporate income “tax holiday” (0% tax rate) for small business (meeting the aforementioned criteria) start-ups is applied. | 15.0% |

| Luxembourg (LU) | 22.8% | Applicable where taxable income does not exceed €175,000. | 24.9% |

| Netherlands (NL) | 16.5% | Applicable to taxable income up to €200,000. | 25.0% |

| Norway (NO) | – | – | 22.0% |

| Poland (PL) | 9.0% | Applicable where revenues do not exceed €2 million. | 19.0% |

| Portugal (PT) | 17.0% | Applicable on the first €25,000 of taxable income of qualifying companies. | 31.5% |

| Slovak Republic (SK) | 15.0% | Applicable where revenues do not exceed €100,000. | 21.0% |

| Slovenia (SI) | – | – | 19.0% |

| Spain (ES) | – | – | 25.0% |

| Sweden (SE) | – | – | 21.4% |

| Switzerland (CH) | – | – | 21.1% |

| Turkey (TR) | – | – | 22.0% |

| United Kingdom (GB) | – | – | 19.0% |

|

Notes: Combined corporate income tax rates show the combined central and sub-central statutory corporate income tax rate given by the central government rate (less deductions for sub-national taxes) plus the sub-central rate. Source: OECD, “Tax Database: Table II.2. Targeted statutory corporate income tax rate,” last updated April 2020, https://stats.oecd.org/Index.aspx?DataSetCode=TABLE_II2. |

|||

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe