Earlier this week, the Environmental Protection Agency outlined a new plan to reduce carbon emissions. This “Clean Power Plan” is based on what is, for the EPA’s CO2-related initiatives if not for other pollutants, a new strategy: outlining broad state-level goals for reducing emissions-per-megawatt hour of electricity, instead of regulating power plants directly. This “climate federalism” has attracted a lot of attention because it’s a new phenomenon in climate policy in the US, and thus its policy implications are unclear.

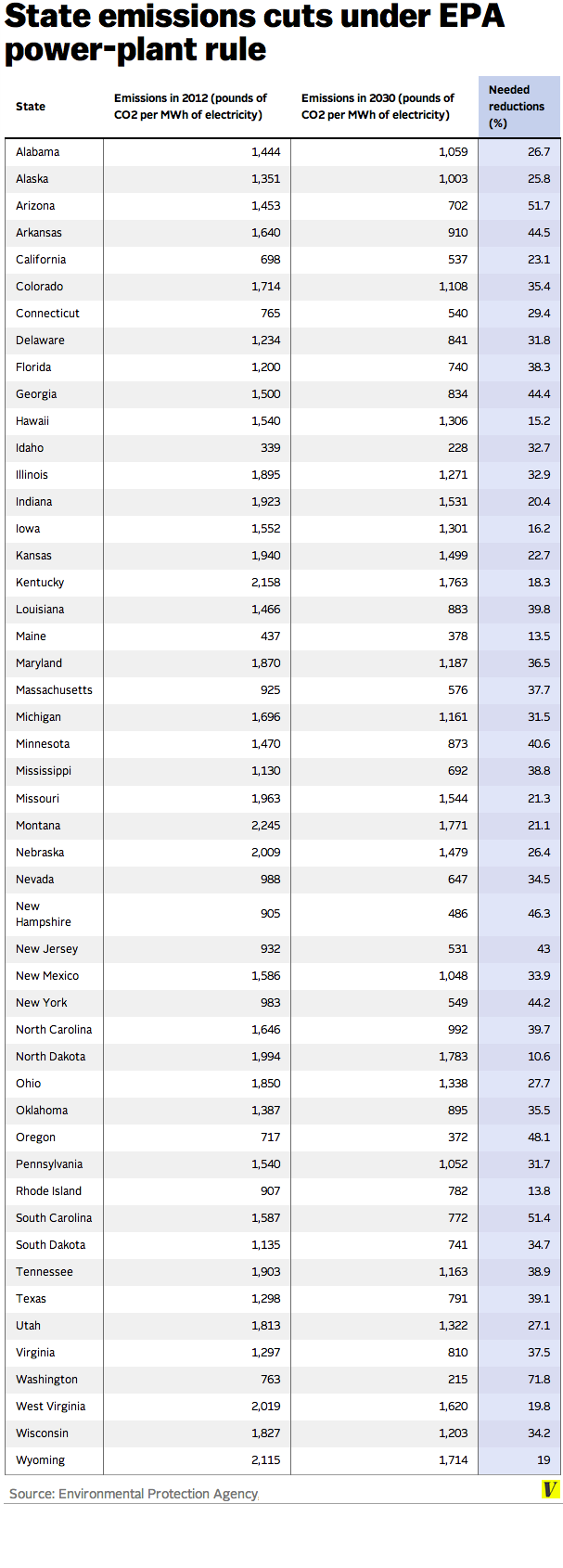

Not all states have been given the same targets. States that are more dependent on carbon-intensive fuels like coal have, in general, been assigned smaller reductions as a percent of emissions, while states that use very little coal have been assigned much bigger per-megawatt hour emissions cuts. But, as many commentators have noted, a small percent reduction in coal usage in states highly dependent on coal may be more difficult than a large percent reduction in states using little coal. Put more simply, Washington’s 70 percent reduction may be easier than Kentucky’s 18 percent reduction, because Washington has fewer major coal plants.

{kind=link}

Interestingly, these changes have taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. implications. As has been noted in many different news outlets, the new rules could serve to push states towards either state- or regional-cap-and-trade plans, or a carbon taxA carbon tax is levied on the carbon content of fossil fuels. The term can also refer to taxing other types of greenhouse gas emissions, such as methane. A carbon tax puts a price on those emissions to encourage consumers, businesses, and governments to produce less of them. . State-level carbon taxes have been proposed before, and states like California and much of New England participate in cap-and-trade schemes. Because a new carbon tax could not only help a state comply with the new EPA rules but also raise new revenue for policymakers to use, it’s possible some states may favor a carbon tax.

Unfortunately, state-level carbon taxes pose serious problems. From an environmental perspective, as noted, different states have different reduction targets: which means it is likely different states would have to impose different tax rates. Charging different taxes for the same product can create serious economic distortions. States with lower carbon costs could see relatively more new investment in carbon-intensive power generation (or energy-intensive industries), and export power and carbon-intensive goods to states with higher taxes, creating a phenomenon known as “carbon leakage.”

From a tax policy perspective, carbon taxes have other problems. Consumption taxes (which is what a carbon tax is) are only non-distortionary if they are evenly-applied, and, like most excise taxes, carbon taxes can be very uneven. Legal, healthcare, and other services, which already receive preferential taxation due to being exempt from the sales tax, have very low carbon footprints: and thus would be even more preferentially treated under a carbon tax. Meanwhile, manufacturers would suffer as the carbon tax shifted spending away from their more carbon-intensive products. Moreover, carbon taxes, due to driving up the price of utilities and many goods relative to services, have a tendency to be regressive, making lower-income people bear the burden of climate change.

Many proposals to implement carbon taxes call for a “grand bargain” or revenue-swap, where higher carbon taxes offset a reduction in income taxes. If previous carbon tax proposals in Massachusetts are any indication, this grand bargain may largely amount to the creation of new credits and deductions, complicating the tax code. But even if the tax reductions offered are well-structured, if carbon taxes actually work, then they will reduce the amount of carbon emissions, which will, in turn, reduce the amount of revenues raised from the tax. Policymakers will either have to renege on the earlier non-carbon tax decreases, or increase the carbon tax even more, creating a cycle of narrowing bases and rising rates.

If that trend sounds familiar, it’s because we’ve seen it all before. Just like using cigarette taxes to fund education, taxing carbon to finance other government priorities will drive revenue instability, distort consumer behavior, and create a perverse linkage where government priorities are rendered financially dependent on a practice the government itself officially regards as damaging.

It remains to be seen how states will respond to the new EPA rules, or even if those rules will hold up to potential legal challenges. Climate change policy is a major interest for many states, and there are many non-tax policy concerns involved in the debate. But when states do assess their response, they should keep in mind that carbon taxes are not substantially different, in tax policy terms, from other narrow, distortionary excise taxes, except that they are an excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. on a vital business input important to many of the most high-value-added industries: energy itself.

Follow Lyman on Twitter.

Read more on carbon taxes here.

Share this article