Key Findings

- The House Republican taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. reform plan would reform the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. and would move towards destination-based cash flow taxation of businesses.

- According to the Tax Foundation’s Taxes and Growth Model, the plan would significantly reduce marginal tax rates and the cost of capital, which would lead to 9.1 percent higher GDP over the long term, 7.7 percent higher wages, and an additional 1.7 million full-time equivalent jobs.

- The plan would reduce federal revenue by $2.4 trillion over the first decade on a static basis. However, due to the larger economy and the broader tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. , the plan would reduce revenue by $191 billion over the first decade.

- Although the plan would reduce federal revenue by $2.4 trillion on a static basis in the first decade, much of the revenue loss is one-time. As a result, the plan will cost much less in subsequent decades.

- On a static basis, the plan would lead to 0.7 percent higher after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings. for all taxpayers and 5.3 percent higher after-tax income for the top 1 percent. When accounting for the increased GDP, after-tax incomes of all taxpayers would increase by at least 8.4 percent.

Introduction

In June, the House Republicans released a tax reform plan.[1] The plan would reform the individual income tax code by lowering marginal tax rates on wage, investment, and business income; broaden the tax base; and simplify the tax code. The plan would also lower the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rate to 20 percent and convert it into a destination-based cash-flow tax. Finally, the plan would eliminate federal estate and gift taxA gift tax is a tax on the transfer of property by a living individual, without payment or a valuable exchange in return. The donor, not the recipient of the gift, is typically liable for the tax. es.

Our analysis finds that the House Republican tax plan would reduce federal tax revenue by $2.4 trillion over the next decade. The plan would reduce marginal tax rates on labor and substantially reduce marginal tax rates on investment. As a result, we estimate that the plan would boost long-run GDP by 9.1 percent. The larger economy would translate into 7.7 percent higher wages and result in 1.7 million more full-time equivalent jobs. Due to the larger economy and the broader tax base, the plan would reduce revenue on a dynamic basis by $191 billion over the next decade.

Changes to the Individual Income Tax

- Consolidates the current seven tax brackets into three, with rates of 12 percent, 25 percent, and 33 percent (Table 1).

| Current Law | Proposal | Single Filers | Married Joint Filers | Head of Household Filers |

|---|---|---|---|---|

| 10% | 12% | $0 to $9,275 | $0 to $18,550 | $0 to $13,250 |

| 15% | 12% | $9,275 to $37,650 | $18,550 to $75,300 | $13,250 to $50,400 |

| 25% | 25% | $37,650 to $91,150 | $75,300 to $151,900 | $50,400 to $130,150 |

| 28% | 25% | $91,150 to $190,150 | $151,900 to $231,450 | $130,150 to $210,800 |

| 33% | 33% | $190,150 to $413,350 | $231,450 to $413,350 | $210,800 to $413,350 |

| 35% | 33% | $413,350 to $415,050 | $413,350 to $466,950 | $413,350 to $441,000 |

| 39.6% | 33% | $415,050+ | $466,950+ | $441,000+ |

- Taxes capital gains and dividends as ordinary income and provides a 50 percent exclusion of capital gains, dividends, and interest income. This is equivalent to taxing capital gains, dividends, and interest income at half the rate of ordinary income, with three brackets of 6 percent, 12.5 percent, and 16.5 percent (Table 2).

| Current Law | Proposal | Single Filers | Married Joint Filers | Head of Household Filers |

|---|---|---|---|---|

| 0% | 6% | $0 to $9,275 | $0 to $18,550 | $0 to $13,250 |

| 0% | 6% | $9,275 to $37,650 | $18,550 to $75,300 | $13,250 to $50,400 |

| 15% | 12.5% | $37,650 to $91,150 | $75,300 to $151,900 | $50,400 to $130,150 |

| 15% | 12.5% | $91,150 to $190,150 | $151,900 to $231,450 | $130,150 to $210,800 |

| 15% | 16.5% | $190,150 to $413,350 | $231,450 to $413,350 | $210,800 to $413,350 |

| 15% | 16.5% | $413,350 to $415,050 | $413,350 to $466,950 | $413,350 to $441,000 |

| 20% | 16.5% | $415,050+ | $466,950+ | $441,000+ |

- Increases the standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. It was nearly doubled for all classes of filers by the 2017 Tax Cuts and Jobs Act (TCJA) as an incentive for taxpayers not to itemize deductions when filing their federal income taxes. from $6,300 to $12,000 for singles, from $12,600 to $24,000 for married couples filing jointly, and from $9,300 to $18,000 for heads of household.

- Eliminates the personal exemption and creates a $500 non-refundable credit for dependents who are not children.

- Increases the Child Tax CreditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly. to $1,500 per child, limits the refundability of the credit to $1,000, and raises the phaseout threshold for the Child Tax Credit for married households from $110,000 to $150,000.

- Eliminates all itemized deductions besides the mortgage interest deductionThe mortgage interest deduction is an itemized deduction for interest paid on home mortgages. It reduces households’ taxable incomes and, consequently, their total taxes paid. The Tax Cuts and Jobs Act (TCJA) reduced the amount of principal and limited the types of loans that qualify for the deduction. and the charitable contribution deduction.

- Eliminates the individual alternative minimum tax.

Changes to Business Income Taxes

- Reduces the corporate income tax rate from 35 percent to 20 percent.

- Eliminates the corporate alternative minimum tax.

- Taxes income derived from pass-through businesses at a maximum rate of 25 percent.

- Allows the cost of capital investment to be fully and immediately deductible.

- Eliminates the deductibility of net interest expenses on future loans.

- Restricts the deduction for net operating losses to 90 percent of net taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. For both individuals and corporations, taxable income differs from—and is less than—gross income. and allows net operating losses to be carried forward indefinitely, and increased by a factor reflecting inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. and the real return to capital. Does not allow net operating losses to be carried back.

- Eliminates the domestic production activities deduction (section 199) and all other business credits, except for the research and development credit.

- Creates a fully territorial tax systemA territorial tax system for corporations, as opposed to a worldwide tax system, excludes profits multinational companies earn in foreign countries from their domestic tax base. As part of the 2017 Tax Cuts and Jobs Act (TCJA), the United States shifted from worldwide taxation towards territorial taxation. , exempting from U.S. tax 100 percent of dividends from foreign subsidiaries.

- Enacts a deemed repatriationTax repatriation is the process by which multinational companies bring overseas earnings back to the home country. Prior to the 2017 Tax Cuts and Jobs Act (TCJA), the U.S. tax code created major disincentives for U.S. companies to repatriate their earnings. Changes from the TCJA eliminate these disincentives. of currently deferred foreign profits, at a tax rate of 8.75 percent for cash and cash-equivalent profits and 3.5 percent on other profits.

- Modifies all business income taxes to be border-adjustable, disallowing the deduction for purchases from nonresidents and exempting export profits and foreign-derived profits from taxation.

Other Changes

- Eliminates federal estate and gift taxes.

Impact on the Economy

According to the Tax Foundation’s Taxes and Growth Model, the House Republican tax plan would increase the long-run size of the economy by 9.1 percent (Table 3). The larger economy would result in 7.7 percent higher wages and a 28.3 percent larger capital stock. The plan would also result in 1.7 million more full-time equivalent jobs.

The larger economy and higher wages are due chiefly to the significantly lower cost of capital under the proposal, which is due to the lower corporate income tax rate and the full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. of capital investment.

| Source: Tax Foundation Taxes and Growth Model, March 2016 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GDP | 9.10% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capital Investment | 28.30% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wage Rate | 7.70% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Full-time Equivalent Jobs (in thousands) | 1,687 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Impact on Revenue

If fully enacted, the proposal would reduce federal revenue by $2.4 trillion over the next decade on a static basis (Table 4). The plan would reduce individual income tax revenue by $981 billion over the next decade. Corporate tax revenue would fall by $1.2 trillion. The remainder of the revenue loss would be due to the repeal of estate and gift taxes.

On a dynamic basis, the plan would reduce federal revenue by $191 billion over the next decade. The larger economy would boost wages and thus broaden both the income and payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. base. As a result, the federal government would see $566 billion in additional individual income tax revenue and $683 billion in additional payroll tax revenue. On the other hand, corporate income tax revenue would actually decline even more on a dynamic basis. This is because the plan would encourage more investment and result in businesses deducting more capital investments, which would reduce corporate taxable income.

| Tax | Static Revenue Impact (2016-2025) | Dynamic Revenue Impact (2016-2025) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Source: Tax Foundation Taxes and Growth Model, March 2016. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Note: Individual items may not sum to total due to rounding. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Individual Income Taxes | -$981 | $566 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Payroll Taxes | $0 | $683 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Corporate Income Taxes | -$1,197 | -$1,324 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Excise taxes | $0 | $57 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Estate and gift taxes | -$240 | -$240 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other Revenue | $0 | $68 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | -$2,418 | -$191 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The House Republican tax plan contains a number of significant base broadeners. Eliminating all itemized deductions except for the mortgage interest deduction and the charitable deduction would significantly broaden the income tax base and raise about $2.3 trillion over the next decade.[2] In addition, the plan would eliminate most individual credits, except for the Child Tax Credit, the Earned Income Tax Credit, and the American Opportunity Tax Credit. This would raise an additional $104 billion over the next decade.

Expanding the standard deduction, replacing the personal exemption with a dependent credit, and expanding the Child Tax Credit would reduce revenue slightly ($127 billion over the next decade).

On the business side, there are two significant base broadeners. The elimination of the interest deduction would raise $1.2 trillion over the next decade. In addition, making business taxes border-adjustable would raise another $1.1 trillion over the next decade. The elimination of business credits and deductions and the limit on net operating losses would bring in an additional $701 billion over the next decade.

The largest sources of revenue loss in the first decade would be the individual and corporate rate cuts and the move to full expensing of capital investments. Reducing individual income tax brackets to 12, 25, and 33 percent would reduce revenue by about $2 trillion over the next decade, while cutting the corporate income tax to 20 percent would reduce revenue by $1.8 trillion over the next decade.[3] Capping the tax rate on pass-through businessA pass-through business is a sole proprietorship, partnership, or S corporation that is not subject to the corporate income tax; instead, this business reports its income on the individual income tax returns of the owners and is taxed at individual income tax rates. es would reduce revenue by $515 billion (after accounting for the new, lower tax brackets). Full expensing of capital investment would reduce revenue by $2.2 trillion over the next decade.

| Provision | Billions of Dollars, 2016-2025 | ||

|---|---|---|---|

| Static | GDP | Dynamic | |

| Eliminate the alternative minimum tax | -$354 | -0.3% | -$428 |

| Eliminate all itemized deductions except for the mortgage interest and charitable contributions deduction | $2,331 | -0.4% | $2,218 |

| Eliminate most personal credits | $104 | 0.0% | $104 |

| Tax capital gains and dividends as ordinary income, allow a 50% deduction for capital gains, dividends, and interest | -$609 | 0.3% | -$531 |

| Allow full expensing of capital investments | -$2,236 | 5.4% | -$883 |

| Disallow interest deduction on new loans | $1,194 | -0.1% | $1,176 |

| Border adjust business taxes | $1,069 | -0.4% | $936 |

| Eliminate section 199 and all business credits, and limit net operating loss deductions | $701 | -0.1% | $677 |

| Repeal the estate and gift taxes | -$241 | 0.9% | -$20 |

| Expand and consolidate the standard deduction, replace the personal exemption with a dependent credit, and expand the Child Tax Credit | -$127 | 0.0% | -$112 |

| Consolidate individual income tax brackets into three of 12 percent, 25 percent, and 33 percent | -$1,954 | 1.5% | -$1,641 |

| Tax income derived from pass-through business at a maximum rate of 25% | -$515 | 0.6% | -$388 |

| Lower the corporate income tax rate to 20% | -$1,807 | 1.7% | -$1,325 |

| Enact a deemed repatriation of deferred foreign-source income | $185 | 0.0% | $185 |

| Move to a territorial tax system | -$160 | 0.0% | -$160 |

Revenue Impact Beyond the First Decade

Although the plan will reduce federal revenues by $2.4 trillion over the next 10 years, much of the cost is due to transitional, or one-time, revenue losses that disappear eventually. There are two provisions that contribute significantly to these transitional costs: full expensing of capital investments and the elimination of the interest deduction.

As stated above, moving to the full expensing of capital investments would reduce federal revenue by $2.2 trillion over the next decade. There are two revenue impacts from moving to expensing. First, businesses will be allowed to fully write off investment costs the first year. This speedup of cost recoveryCost recovery is the ability of businesses to recover (deduct) the costs of their investments. It plays an important role in defining a business’ tax base and can impact investment decisions. When businesses cannot fully deduct capital expenditures, they spend less on capital, which reduces worker’s productivity and wages. increases the present value of cost recovery and reduces federal revenue each year. Second, after full expensing is enacted, businesses will continue to write off investments they made under the old depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. regime. When businesses fully write off new investments and continue to write off old investments, corporate taxable income falls significantly in those years, greatly reducing corporate revenue. However, once old depreciation has expired, the annual cost of expensing drops.

The plan also eliminates the deduction for net interest payments by businesses. We assumed that this provision would be prospective, or it would only apply to interest on loans made after the proposal went into effect. As a result, businesses would continue to deduct interest from loans acquired before enactment of the plan, reducing the amount of revenue this provision would raise in the first decade. In later decades, as old debt is retired, more interest would no longer be deductible, resulting in more revenue.

The plan also has one transitional revenue raiser: deemed repatriation. This proposal would tax corporations on their current deferred offshore profits. We assume that this provision would only raise revenue in the first 10 years.

As a result of these transitional issues, the plan would cost much less in subsequent decades. We estimate that the proposal would reduce federal revenue by 1.1 percent of GDP in the first decade, 0.5 percent of GDP in the second decade, and 0.4 percent of GDP after all transition costs have phased out.

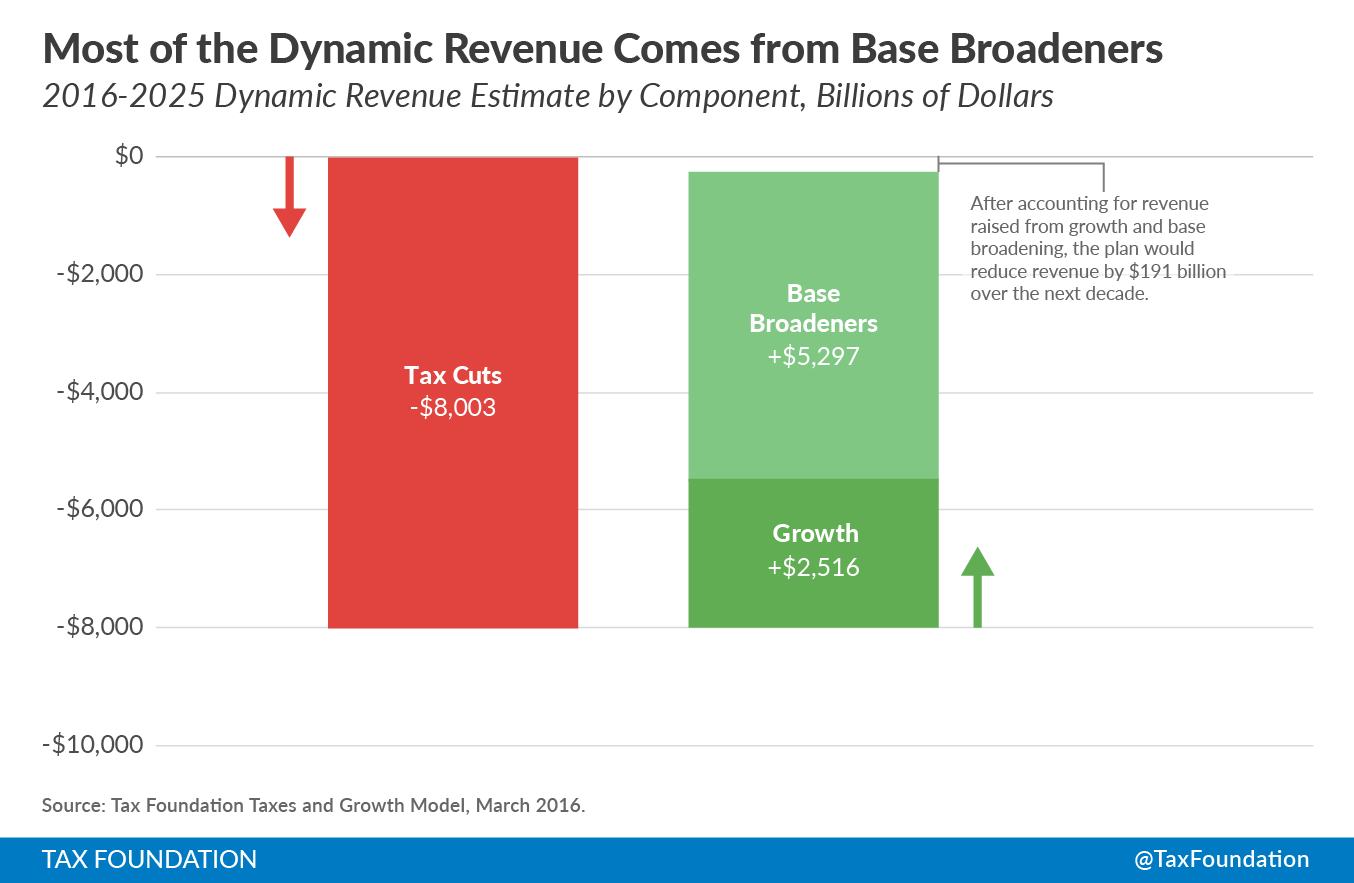

Components of the Dynamic Revenue Estimate

The dynamic revenue impact of -$191 billion over the next decade can be broken down into three pieces: the marginal tax cuts, growth, and the base broadeners.

The first piece is the marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax. reductions in the plan. These provisions include, but are not limited to, the cut in the corporate income tax rate to 20 percent, full expensing of capital investments, and the reduction in marginal tax rates for most individuals. Combined, these tax cuts would reduce federal revenue by $8 trillion over the next decade if enacted alone.

The second piece is the expected increase in revenue due to economic growth. As stated previously, this plan would reduce marginal tax rates on work, saving, and investment. Our model finds that these marginal tax rates would significantly increase the long-run size of the economy. The larger economy would boost wages and thus increase the tax base, especially for the individual income and payroll taxes. As a result, the growth from the plan would reduce the 10-year cost of the plan by roughly $2.5 trillion.

The third and final piece is the base broadeners in the plan. The House Republican tax plan contains a number of significant base-broadening provisions, such as the elimination of most itemized deductionItemized deductions allow individuals to subtract designated expenses from their taxable income and can be claimed in lieu of the standard deduction. Itemized deductions include those for state and local taxes, charitable contributions, and mortgage interest. An estimated 13.7 percent of filers itemized in 2019, most being high-income taxpayers. s, the elimination of the deduction for net interest expenses for businesses, and the border adjustment of businesses taxes. Combined, these provisions significantly broaden the tax base and reduce the revenue loss of the tax plan by $5.3 trillion over the next decade.

Distributional Impact of the Plan

On a static basis, the House Republican tax plan would increase the after-tax incomes of taxpayers in every income group. The bottom 80 percent of taxpayers (those in the bottom four quintiles) would see a small increase in after-tax income between 0.2 percent and 0.5 percent. Taxpayers in the top 10 percent would see a 1 percent increase in after-tax income. Taxpayers in the top 1 percent would see the largest increase in after-tax income on a static basis of 5.3 percent, driven by both the lower top marginal tax rate and the lower corporate income tax.

On a dynamic basis, all taxpayers would see an increase in after-tax income of at least 8.4 percent. The top 1 percent of taxpayers would see an increase in after-tax income of 13 percent on a dynamic basis.

| Changes in After-Tax Incomes | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Income Group | Static | Dynamic | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Source: Tax Foundation, Taxes and Growth Model (March 2016 version) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 0% to 20% | 0.3% | 8.4% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 20% to 40% | 0.5% | 8.6% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 40% to 60% | 0.2% | 9.1% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 60% to 80% | 0.2% | 8.5% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 80% to 100% | 1.0% | 8.8% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 90% to 100% | 1.5% | 9.3% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 99% to 100% | 5.3% | 13.0% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TOTAL | 0.7% | 8.7% | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Conclusion

The House Republican tax plan would reform both the individual income tax and convert the corporate income tax into a destination-based cash flow tax. This plan would significantly reduce the cost of capital and reduce the marginal tax rate on labor. These changes in the incentives to work and invest would greatly increase the U.S. economy’s size in the long run, boost wages, and result in more full-time equivalent jobs. On a static basis, the plan would reduce federal revenue by $2.4 trillion, most of the revenue loss being from one-time transitional costs. However, due to the larger economy and the significantly broader tax base, the plan would reduce revenue by $191 billion over the next decade.

Modeling Notes

The Taxes and Growth Model does not take into account the fiscal or economic effects of interest on debt. It also does not require budgets to balance over the long term, nor does it account for the potential macroeconomic or distributional effects of any changes to government spending that may accompany the tax plan.

We modeled all provisions outlined above and assumed that all provisions were enacted in the beginning of 2016. We accounted for potential transitional costs: most notably, the transition costs associated with moving to full expensing and the phase-in of the elimination of the interest deduction. Both the static and dynamic revenue impacts of the plan are relative to the CBO’s current law baseline.

We assumed that Treasury would design anti-abuse provisions that would be successful in preventing individuals from reclassifying a significant amount of wage compensation as business income in order to benefit from the special 25 percent tax rate of pass-through income.

In modeling the distributional impact of the plan we followed the convention that changes to the corporate income tax are passed to capital and labor. We assumed on a static basis that 30 percent of the corporate tax change is passed to labor and 70 percent is passed to capital. On a dynamic basis, changes to the corporate income tax falls on capital and labor in proportion to their share of factor income: roughly 70 percent labor and 30 percent capital.

We did not model the impact of changes to tax policy associated with the House Republican healthcare reform plan, which contains provisions that will impact tax revenue.

[1] “A Better Way, Our Vision for a Confident America: Tax,” June 24, 2016. http://abetterway.speaker.gov/_assets/pdf/ABetterWay-Tax-PolicyPaper.pdf

[2] The House Republican tax plan also mentions that it would reform the home mortgage interest deduction and the charitable deduction. However, without further details, we assumed that these provisions would be left alone.

[3] These revenue numbers are calculated assuming that the individual and corporate tax bases have already been broadened.